Question: Can this be reviewed to determine whether I am explaining the concept asked in the assignment is correct or on target? How would you define

Can this be reviewed to determine whether I am explaining the concept asked in the assignment is correct or on target?

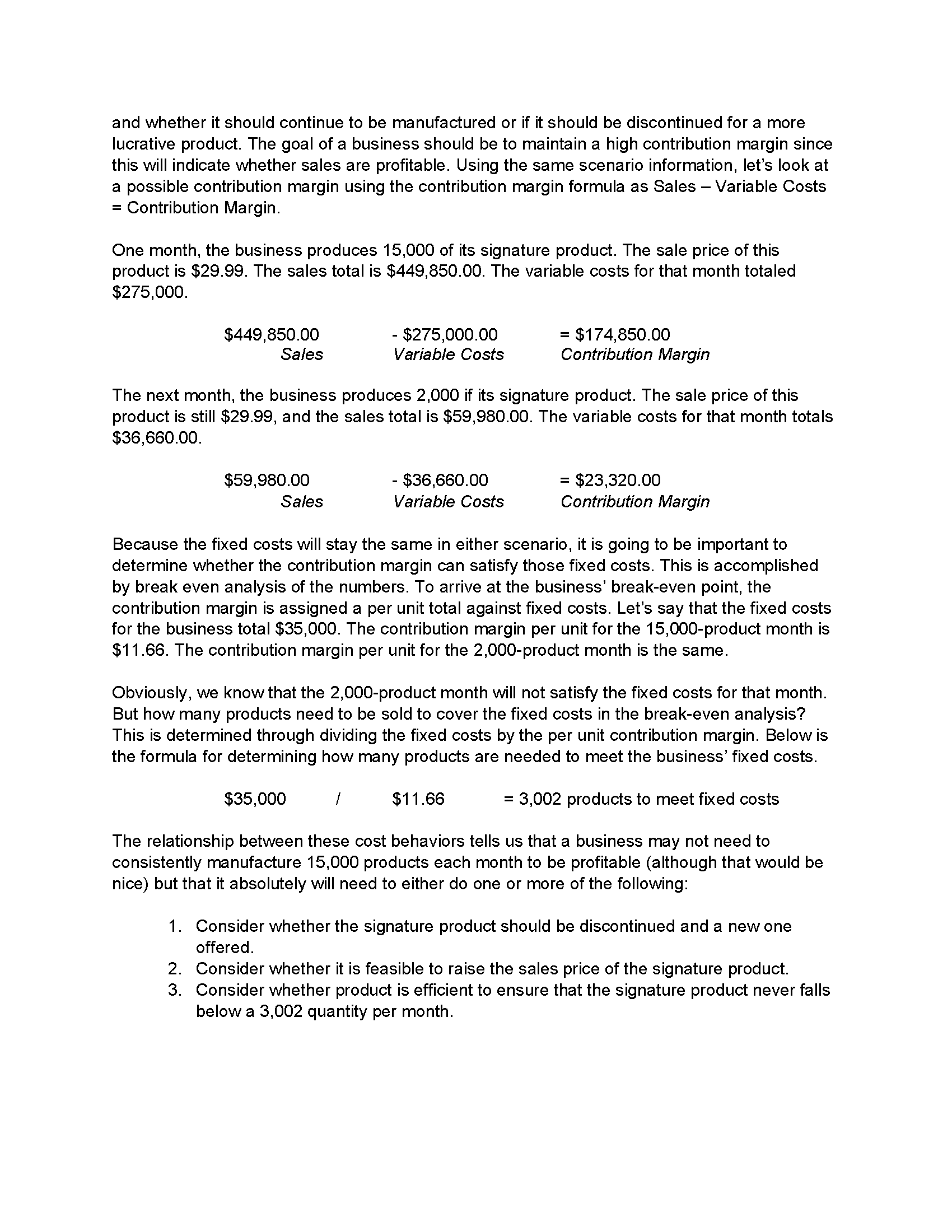

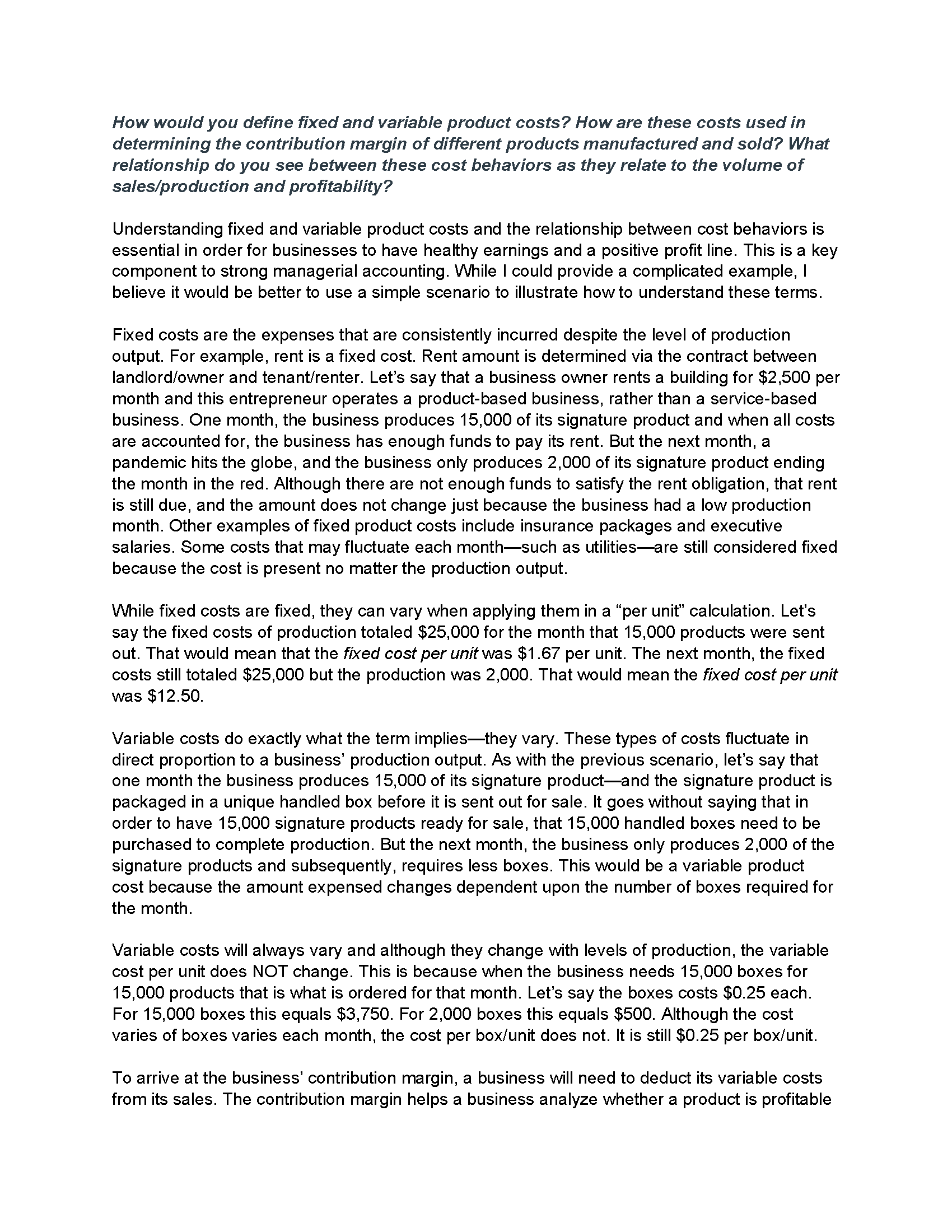

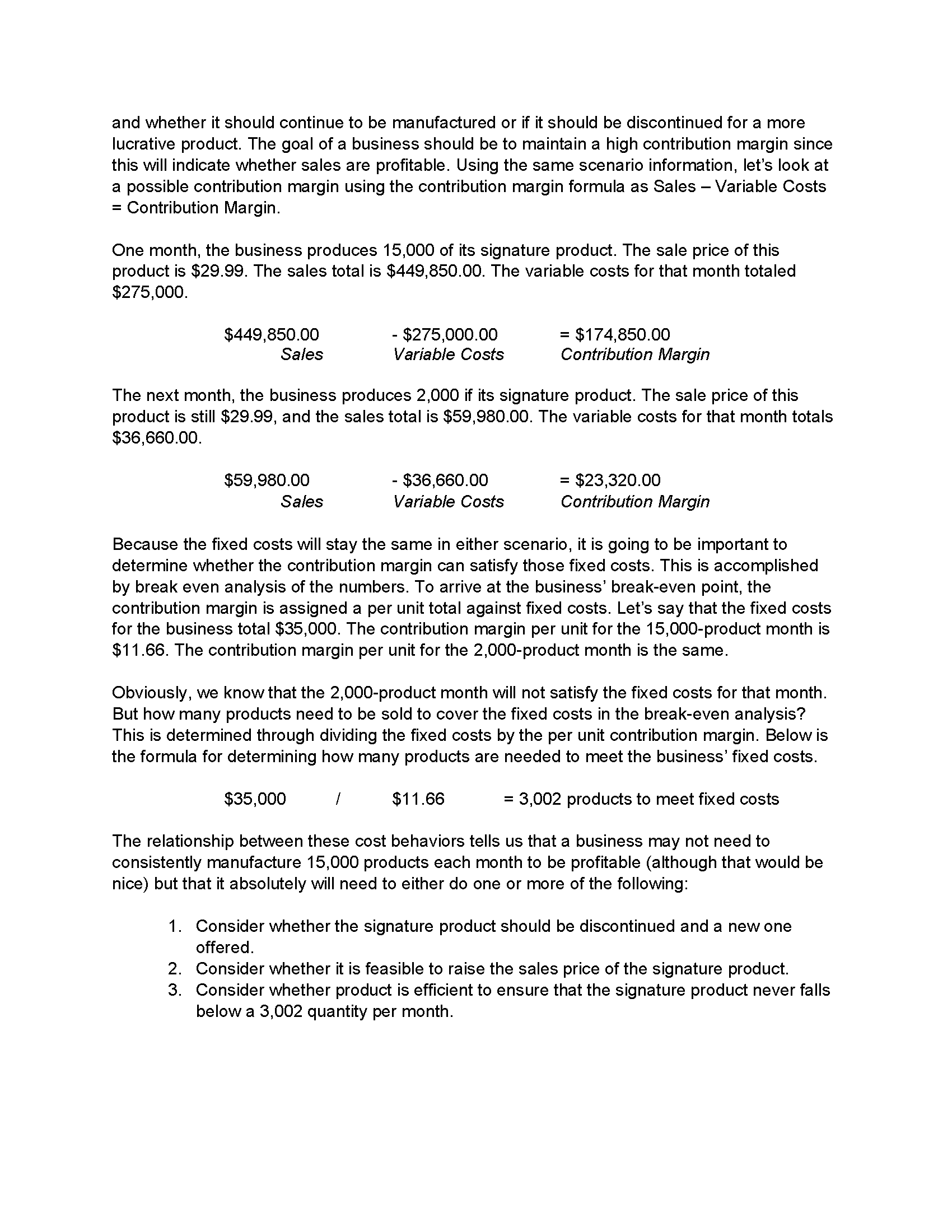

How would you define xed and variable product costs? How are these costs used in determining the contribution margin of different products manufactured and sold? What relationship do you see between these cost behaviors as they relate to the volume of sales/production and protability? Understanding fixed and variable product costs and the relationship between cost behaviors is essential in orderfor businesses to have healthy earnings and a positive profit line. This is a key component to strong managerial accounting. While I could provide a complicated example, I believe it would be better to use a simple scenario to illustrate how to understand these terms. Fixed costs are the expenses that are consistently incurred despite the level of production output. For example, rent is a fixed cost. Rent amount is determined via the contract between landlord/owner and tenant/renter. Let's say that a business owner rents a building for $2,500 per month and this entrepreneur operates a product-based business, rather than a service-based business. One month, the business produces 15,000 of its signature product and when all costs are accounted for, the business has enough funds to pay its rent. But the next month, a pandemic hits the globe, and the business only produces 2,000 of its signature product ending the month in the red. Although there are not enough funds to satisfy the rent obligation, that rent is still due, and the amount does not change just because the business had a low production month. Other examples of fixed product costs include insurance packages and executive salaries. Some costs that may fluctuate each monthsuch as utilitiesare still considered fixed because the cost is present no matter the production output. While fixed costs are fixed, they can vary when applying them in a "per unit\" calculation. Let's say the fixed costs of production totaled $25,000 for the month that 15,000 products were sent out. That would mean that the fixed cost per unit was $1.67 per unit. The next month, the fixed costs still totaled $25,000 but the production was 2,000. That would mean the xed cost per unit was $12.50. Variable costs do exactly what the term impliesthey vary. These types of costs fluctuate in direct proportion to a business' production output. As with the previous scenario, let's say that one month the business produces 15,000 of its signature productand the signature product is packaged in a unique handled box before it is sent out for sale. It goes without saying that in order to have 15,000 signature products ready for sale, that 15,000 handled boxes need to be purchased to complete production. But the next month, the business only produces 2,000 of the signature products and subsequently, requires less boxes. This would be a variable product cost because the amount expensed changes dependent upon the number of boxes required for the month. Variable costs will always vary and although they change with levels of production, the variable cost per unit does NOT change. This is because when the business needs 15,000 boxes for 15,000 products that is what is ordered for that month. Let's say the boxes costs $0.25 each. For 15,000 boxes this equals $3,750. For 2,000 boxes this equals $500. Although the cost varies of boxes varies each month, the cost per box/unit does not. It is still $0.25 per box/unit. To arrive at the business' contribution margin, a business will need to deduct its variable costs from its sales. The contribution margin helps a business analyze whether a product is profitable and whether it should continue to be manufactured or if it should be discontinued for a more lucrative product. The goal of a business should be to maintain a high contribution margin since this will indicate whether sales are profitable. Using the same scenario information, let's look at a possible contribution margin using the contribution margin formula as Sales Variable Costs = Contribution Margin. One month, the business produces 15,000 of its signature product. The sale price of this product is $29.99. The sales total is $449,850.00. The variable costs for that month totaled $275,000. $449,850.00 - $275,000.00 = $174,850.00 Sales Variable Costs Contribution Margin The next month, the business produces 2,000 if its signature product. The sale price of this product is still $29.99, and the sales total is $59,980.00. The variable costs for that month totals $36,660.00. $59,980.00 - $36,660.00 = $23,320.00 Sales Variable Costs Contribution Margin Because the fixed costs will stay the same in either scenario, it is going to be important to determine whether the contribution margin can satisfy those fixed costs. This is accomplished by break even analysis of the numbers. To arrive at the business' break-even point, the contribution margin is assigned a per unit total against fixed costs. Let's say that the fixed costs for the business total $35,000. The contribution margin per unit for the 15,000-product month is $11.66. The contribution margin per unit for the 2,000-product month is the same. Obviously, we know that the 2,000-product month will not satisfy the fixed costs for that month. But how many products need to be sold to cover the fixed costs in the break-even analysis? This is determined through dividing the fixed costs by the per unit contribution margin. Below is the formula for determining how many products are needed to meet the business' fixed costs. $35,000 / $11.66 = 3,002 products to meet fixed costs The relationship between these cost behaviors tells us that a business may not need to consistently manufacture 15,000 products each month to be profitable (although that would be nice) but that it absolutely will need to either do one or more of the following: 1. Consider whether the signature product should be discontinued and a new one offered. 2. Consider whether it is feasible to raise the sales price of the signature product. 3. Consider whether product is efficient to ensure that the signature product never falls below a 3,002 quantity per month

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts