Question: can you help ? be specific so I can learn when doing similar problems. Calculate 98% and 99% VaR at the 1 and 10 day

can you help ? be specific so I can learn when doing similar problems.

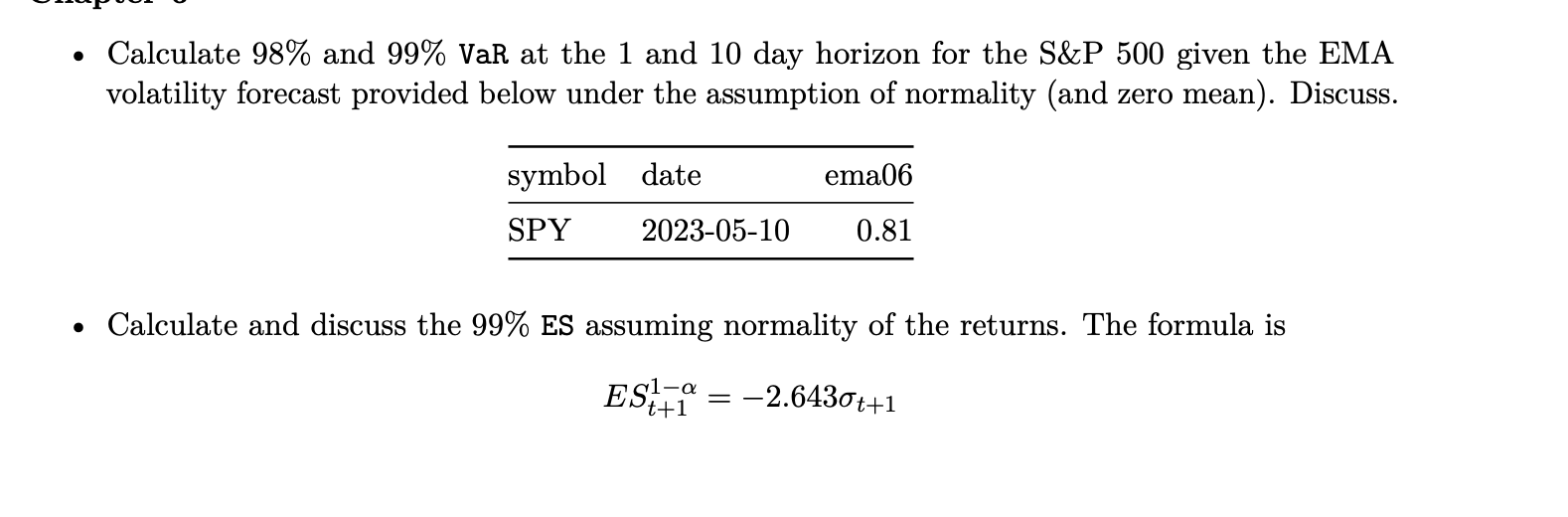

Calculate 98% and 99% VaR at the 1 and 10 day horizon for the S\&P 500 given the EMA volatility forecast provided below under the assumption of normality (and zero mean). Discuss. Calculate and discuss the 99% ES assuming normality of the returns. The formula is ESt+11=2.643t+1

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock