Question: Can you help me solve this problem? Chapter 06 - HW CDUUN 4. Problem 6-07 5. The following are monthly percentage price changes for four

Can you help me solve this problem?

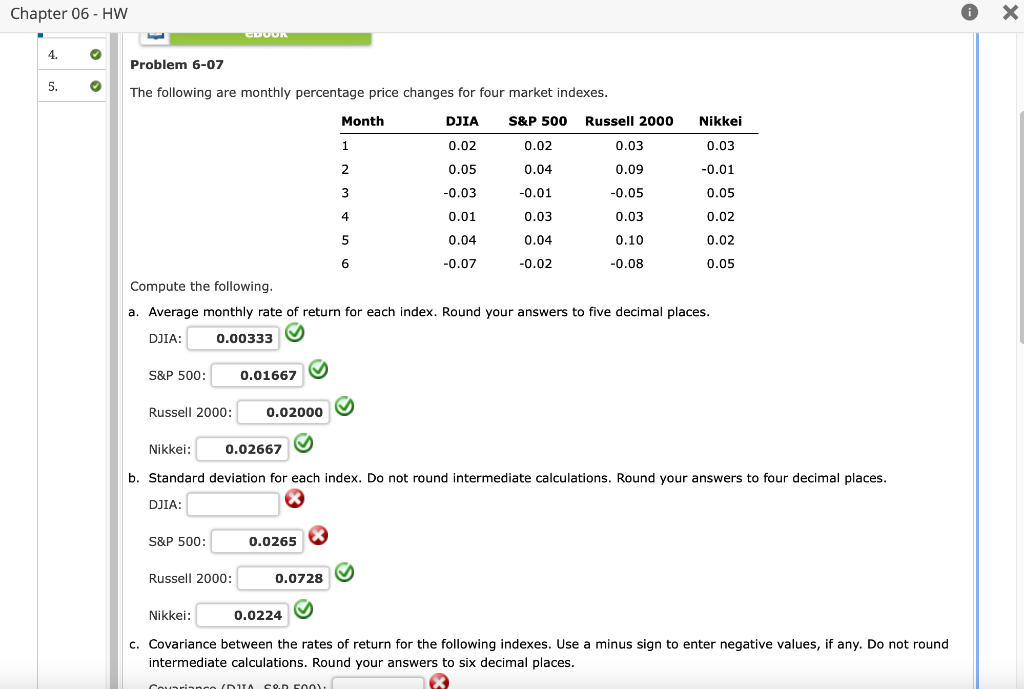

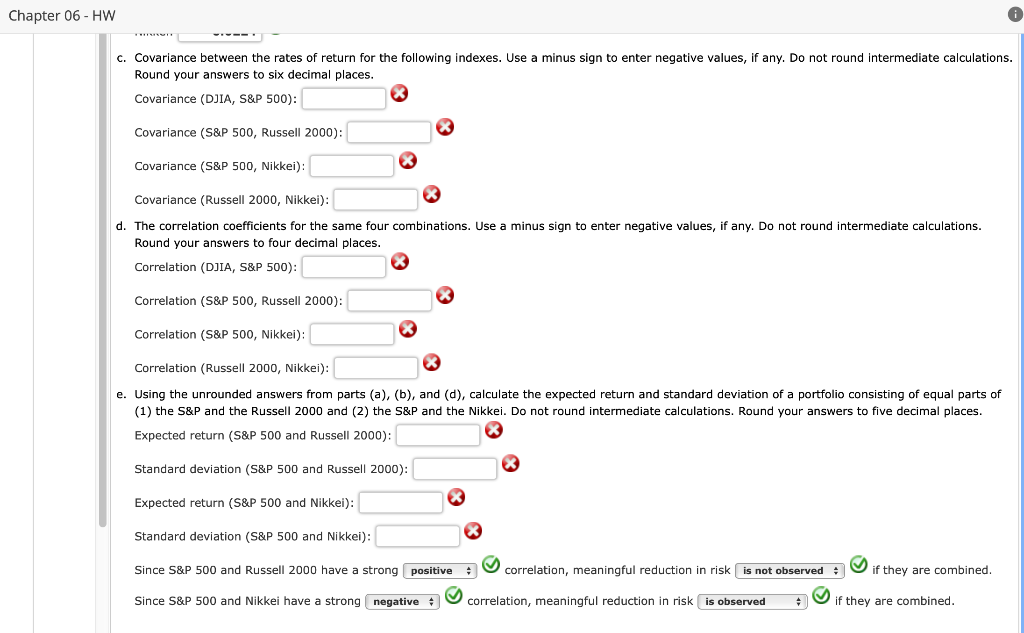

Chapter 06 - HW CDUUN 4. Problem 6-07 5. The following are monthly percentage price changes for four market indexes. Month DJIA S&P 500 Russell 2000 1 0.02 0.02 0.03 2 0.05 0.04 0.09 3 -0.01 Nikkei 0.03 -0.01 0.05 -0.03 -0.05 4 0.01 0.03 0.03 0.02 5 0.04 0.04 0.10 0.02 6 -0.07 -0.02 -0.08 0.05 Compute the following. a. Average monthly rate of return for each index. Round your answers to five decimal places. DJIA: 0.00333 S&P 500: 0.01667 Russell 2000: 0.02000 Nikkel: 0.02667 b. Standard deviation for each index. Do not round intermediate calculations. Round your answers to four decimal places. DJIA: S&P 500: 0.0265 Russell 2000: 0.0728 Nikkei: 0.0224 C. Covariance between the rates of return for the following indexes. Use a minus sign to enter negative values, if any. Do not round intermediate calculations. Round your answers to six decimal places. Cournon (DUTA S 5001 Son Chapter 06- HW C. Covariance between the rates of return for the following indexes. Use a minus sign to enter negative values, if any. Do not round intermediate calculations. Round your answers to six decimal places. Covariance (DJIA, S&P 500): Covariance (S&P 500, Russell 2000): Covariance (S&P 500, Nikkei): Covariance (Russell 2000, Nikkei): d. The correlation coefficients for the same four combinations. Use a minus sign to enter negative values, if any. Do not round intermediate calculations. Round your answers to four decimal places. Correlation (DJIA, S&P 500): Correlation (S&P 500, Russell 2000): Correlation (S&P 500, Nikkei) Correlation (Russell 2000, Nikkei): e. Using the unrounded answers from parts (a), (b), and (d), calculate the expected return and standard deviation of a portfolio consisting of equal parts of (1) the S&P and the Russell 2000 and (2) the S&P and the Nikkei. Do not round intermediate calculations. Round your answers to five decimal places. Expected return (S&P 500 and Russell 2000): Standard deviation (S&P 500 and Russell 2000): Expected return (S&P 500 and Nikkei): Standard deviation (S&P 500 and Nikkei): Since S&P 500 and Russell 2000 have a strong positive correlation, meaningful reduction in risk is not observed - if they are combined Since S&P 500 and Nikkei have a strong negative correlation, meaningful reduction in risk is observed if they are combined

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts