Question: Can you please do Question 4, I'm having a hard time figuring out how to answer it Exercise I (20 marks) We suppose the following

Can you please do Question 4, I'm having a hard time figuring out how to answer it

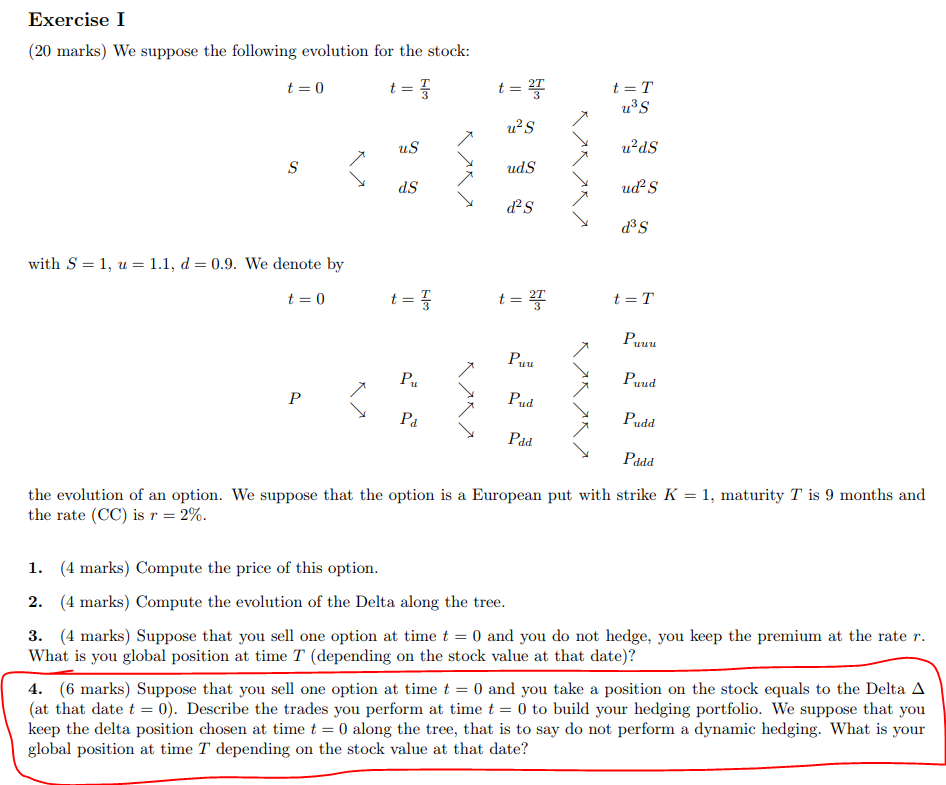

Exercise I (20 marks) We suppose the following evolution for the stock: 3 with S 1, u 1.1, d-0.9. We denote by t2T 3 Puu PuPuud the evolution of an option. We suppose that the option is a European put with strike K = 1, maturity T is 9 months and the rate (CC) is r-2% 1. (4 marks) Compute the price of this option 2. (4 marks) Compute the evolution of the Delta along the tree 3. (4 marks) Suppose that you sell one option at time t = 0 and you do not hedge, you keep the premium at the rate r What is you global position at time T (depending on the stock value at that date)? 4. (6 marks) Suppose that you sell one option at time t = 0 and you take a position on the stock equals to the Delta (at that date 0). Describe the trades you perform at time t 0 to build your hedging portfolio. We suppose that you keep the delta position chosen at time t 0 along the tree, that is to say do not perform a dynamic hedging. What is your global position at time T depending on the stock value at that date? Exercise I (20 marks) We suppose the following evolution for the stock: 3 with S 1, u 1.1, d-0.9. We denote by t2T 3 Puu PuPuud the evolution of an option. We suppose that the option is a European put with strike K = 1, maturity T is 9 months and the rate (CC) is r-2% 1. (4 marks) Compute the price of this option 2. (4 marks) Compute the evolution of the Delta along the tree 3. (4 marks) Suppose that you sell one option at time t = 0 and you do not hedge, you keep the premium at the rate r What is you global position at time T (depending on the stock value at that date)? 4. (6 marks) Suppose that you sell one option at time t = 0 and you take a position on the stock equals to the Delta (at that date 0). Describe the trades you perform at time t 0 to build your hedging portfolio. We suppose that you keep the delta position chosen at time t 0 along the tree, that is to say do not perform a dynamic hedging. What is your global position at time T depending on the stock value at that date

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts