Question: Can you please fix the red boxes Culver Corp. purchased depreciable assets costing $25,200 on January 2, 2020. For tax purposes, the company uses CCA

Can you please fix the red boxes

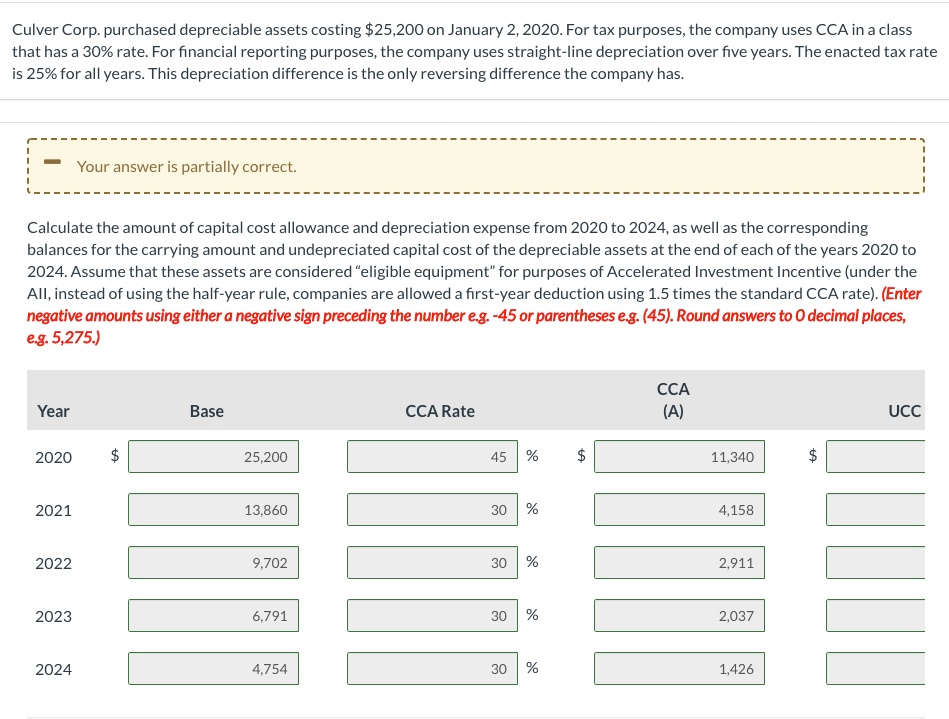

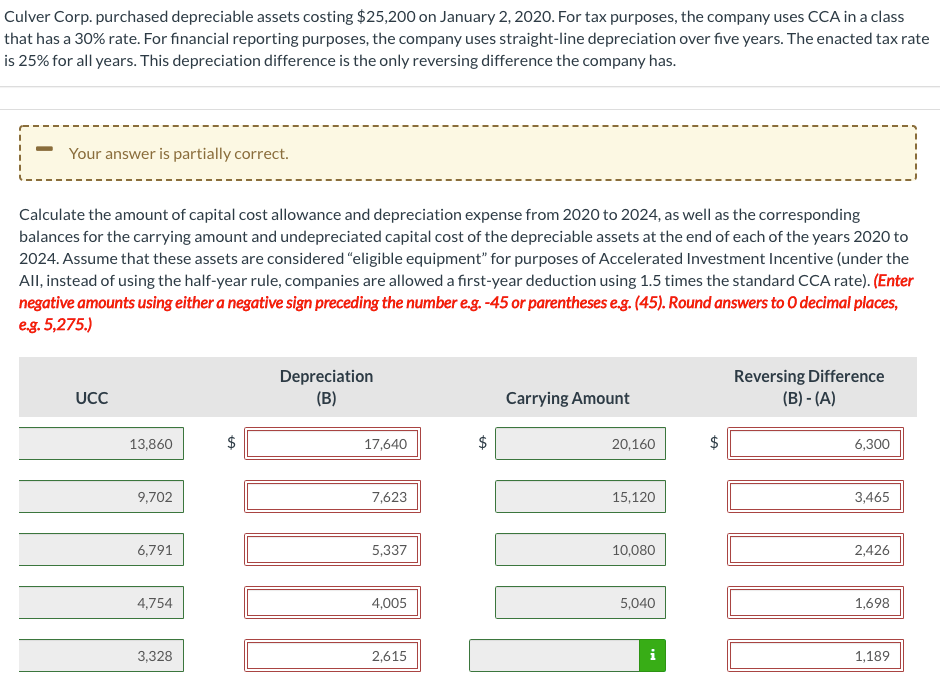

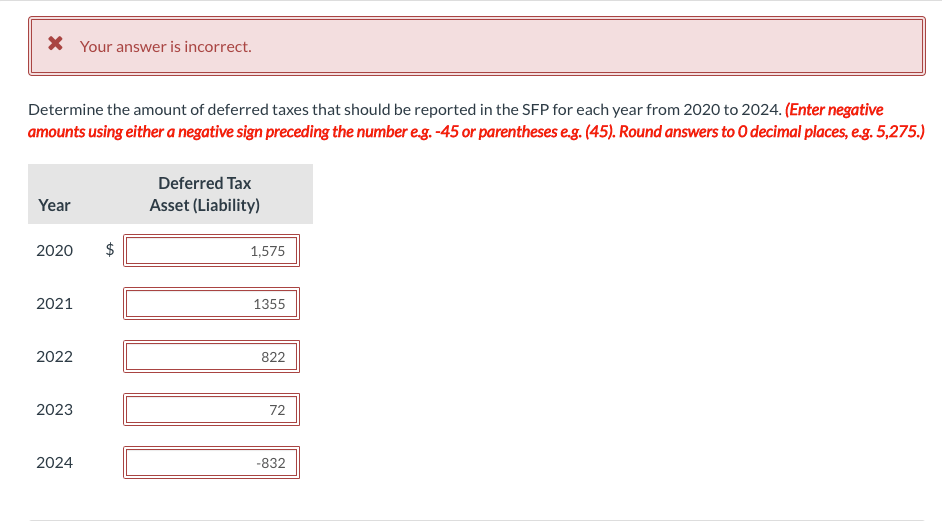

Culver Corp. purchased depreciable assets costing $25,200 on January 2, 2020. For tax purposes, the company uses CCA in a class that has a 30% rate. For financial reporting purposes, the company uses straight-line depreciation over five years. The enacted tax rate is 25% for all years. This depreciation difference is the only reversing difference the company has. Your answer is partially correct. Calculate the amount of capital cost allowance and depreciation expense from 2020 to 2024, as well as the corresponding balances for the carrying amount and undepreciated capital cost of the depreciable assets at the end of each of the years 2020 to 2024. Assume that these assets are considered "eligible equipment" for purposes of Accelerated Investment Incentive (under the All, instead of using the half-year rule, companies are allowed a first-year deduction using 1.5 times the standard CCA rate). (Enter negative amounts using either a negative sign preceding the number e.g.-45 or parentheses eg. (45). Round answers to O decimal places, e.g. 5,275.) Year Base CCA Rate CCA (A) UCC 2020 25,200 45 % A 11,340 TA 2021 13,860 30 % 4,158 2022 9,702 30 % 2,911 2023 6,791 30 % 2,037 2024 4,754 30 % 1,426 Culver Corp. purchased depreciable assets costing $25,200 on January 2, 2020. For tax purposes, the company uses CCA in a class that has a 30% rate. For financial reporting purposes, the company uses straight-line depreciation over five years. The enacted tax rate is 25% for all years. This depreciation difference is the only reversing difference the company has. Your answer is partially correct. Calculate the amount of capital cost allowance and depreciation expense from 2020 to 2024, as well as the corresponding balances for the carrying amount and undepreciated capital cost of the depreciable assets at the end of each of the years 2020 to 2024. Assume that these assets are considered "eligible equipment" for purposes of Accelerated Investment Incentive (under the All, instead of using the half-year rule, companies are allowed a first-year deduction using 1.5 times the standard CCA rate). (Enter negative amounts using either a negative sign preceding the number e.g. -45 or parentheses e.g. (45). Round answers to decimal places, eg. 5,275.) Depreciation (B) Reversing Difference (B) -(A) UCC Carrying Amount 13,860 $ 17,640 ta 20,160 $ 6,300 9,702 7,623 15,120 3,465 6,791 5,337 10,080 2,426 4,754 4,005 5,040 1,698 3,328 2,615 1,189 * Your answer is incorrect. Determine the amount of deferred taxes that should be reported in the SFP for each year from 2020 to 2024. (Enter negative amounts using either a negative sign preceding the number eg.-45 or parentheses e.g. (45). Round answers to 0 decimal places, eg. 5,275.) Deferred Tax Asset (Liability) Year 2020 $ 1,575 2021 1355 2022 822 2023 72 2024 -832

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts