Question: Can you please write down the solutions on paper? Don't use excel. We consider a portfolio composed of unit quantity of each of these two

Can you please write down the solutions on paper? Don't use excel.

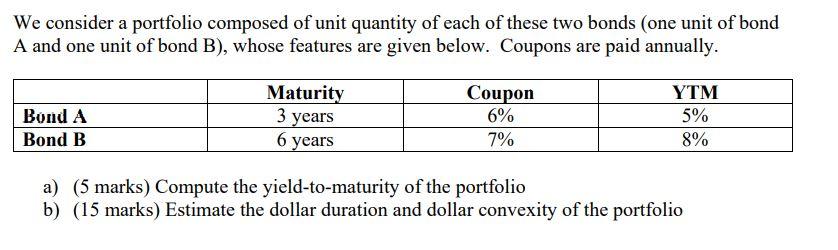

We consider a portfolio composed of unit quantity of each of these two bonds (one unit of bond A and one unit of bond B), whose features are given below. Coupons are paid annually. Bond A Bond B Maturity 3 years 6 years Coupon 6% 7% YTM 5% 8% a) (5 marks) Compute the yield-to-maturity of the portfolio b) (15 marks) Estimate the dollar duration and dollar convexity of the portfolio We consider a portfolio composed of unit quantity of each of these two bonds (one unit of bond A and one unit of bond B), whose features are given below. Coupons are paid annually. Bond A Bond B Maturity 3 years 6 years Coupon 6% 7% YTM 5% 8% a) (5 marks) Compute the yield-to-maturity of the portfolio b) (15 marks) Estimate the dollar duration and dollar convexity of the portfolio

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts