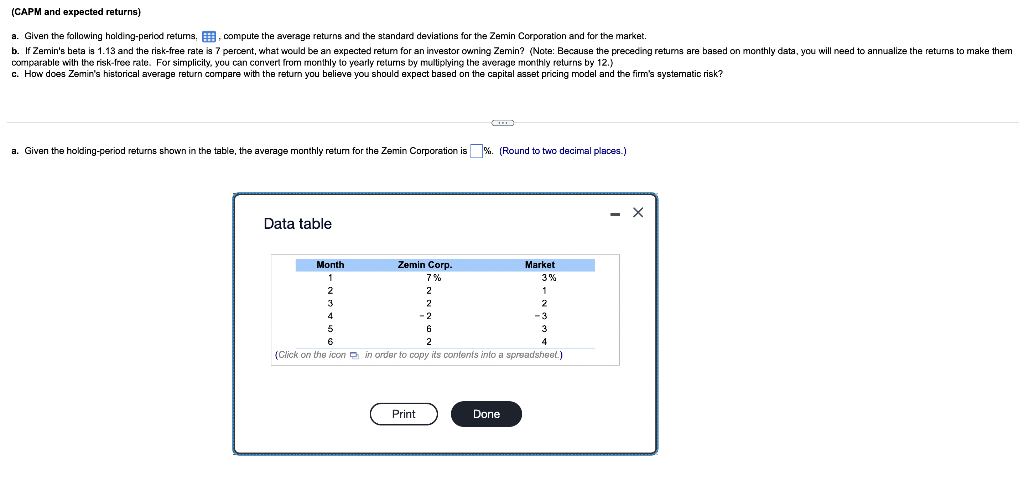

Question: (CAPM and expected returns) annualize the returns to make them a. Given the following holding-period retums, compute the average returns and the standard deviations for

(CAPM and expected returns) annualize the returns to make them a. Given the following holding-period retums, compute the average returns and the standard deviations for the Zemin Corporation and for the market. b. If Zemin's beta is 1.13 and the risk-free rate is 7 percent, what would be an expected retum for an investor owning Zemin? (Note: Because the preceding retums are based on monthly data, you will need comparable with the risk-frce rate. For simplicity, you can convert from monthly to yearly returns by multiplying the average monthly returns by 12.) c. How does Zemin's historical average return compare with the return you believe you should expect based on the capital asset pricing model and the firm's systematic risk? a. Given the holding-period returns shown in the table, the average monthly return for the Zemin Corporation is %. (Round to two decimal places.) Data table Month Zemin Corp. Market 7% 3% 2 2 1 2 2 4 -2 -3 5 6 3 2 4 (Click on the icon in order to copy its contents into a spreadsheet.) Print Done

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts