Question: Case 6 / Intangible Assets (7 Points) and Company R is in the automotive industry. It's main field of business is the development production of

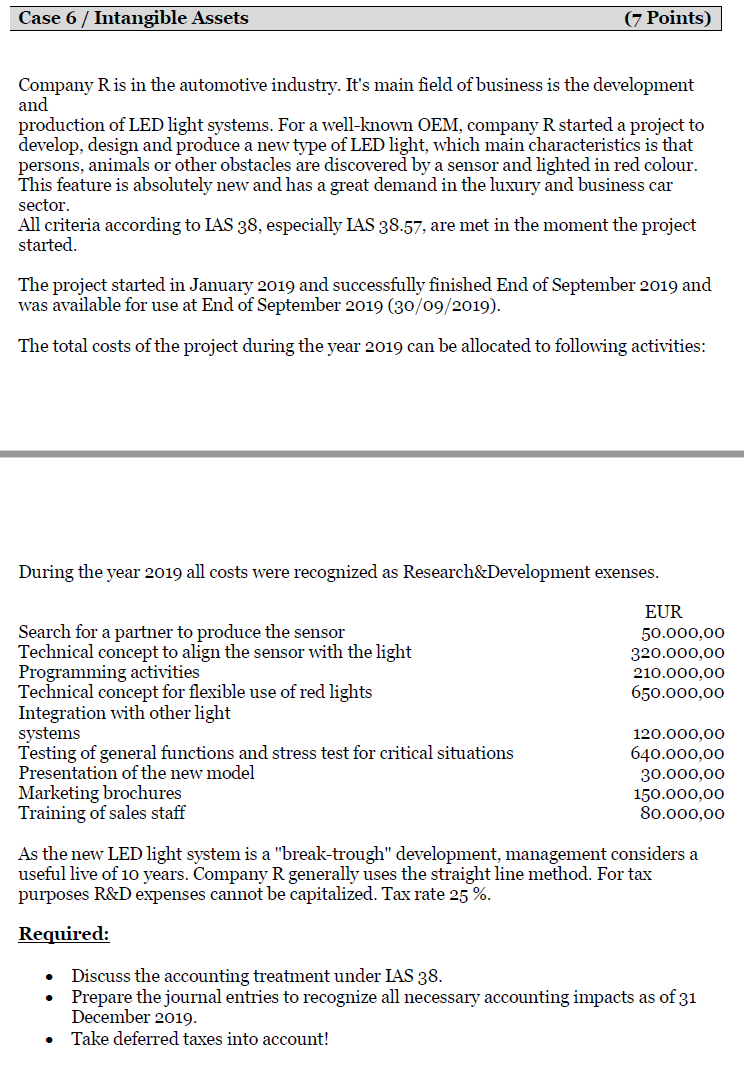

Case 6 / Intangible Assets (7 Points) and Company R is in the automotive industry. It's main field of business is the development production of LED light systems. For a well-known OEM, company R started a project to develop, design and produce a new type of LED light, which main characteristics is that persons, animals or other obstacles are discovered by a sensor and lighted in red colour. This feature is absolutely new and has a great demand in the luxury and business car sector. All criteria according to IAS 38, especially IAS 38.57, are met in the moment the project started. The project started in January 2019 and successfully finished End of September 2019 and was available for use at End of September 2019 (30/09/2019). The total costs of the project during the year 2019 can be allocated to following activities: During the year 2019 all costs were recognized as Research&Development exenses. EUR 50.000,00 320.000,00 210.000,00 650.000,00 Search for a partner to produce the sensor Technical concept to align the sensor with the light Programming activities Technical concept for flexible use of red lights Integration with other light systems Testing of general functions and stress test for critical situations Presentation of the new model Marketing brochures Training of sales staff 120.000,00 640.000,00 30.000,00 150.000,00 80.000,00 As the new LED light system is a "break-trough" development, management considers a useful live of 10 years. Company R generally uses the straight line method. For tax purposes R&D expenses cannot be capitalized. Tax rate 25%. Required: Discuss the accounting treatment under IAS 38. Prepare the journal entries to recognize all necessary accounting impacts as of 31 December 2019. Take deferred taxes into account! Case 6 / Intangible Assets (7 Points) and Company R is in the automotive industry. It's main field of business is the development production of LED light systems. For a well-known OEM, company R started a project to develop, design and produce a new type of LED light, which main characteristics is that persons, animals or other obstacles are discovered by a sensor and lighted in red colour. This feature is absolutely new and has a great demand in the luxury and business car sector. All criteria according to IAS 38, especially IAS 38.57, are met in the moment the project started. The project started in January 2019 and successfully finished End of September 2019 and was available for use at End of September 2019 (30/09/2019). The total costs of the project during the year 2019 can be allocated to following activities: During the year 2019 all costs were recognized as Research&Development exenses. EUR 50.000,00 320.000,00 210.000,00 650.000,00 Search for a partner to produce the sensor Technical concept to align the sensor with the light Programming activities Technical concept for flexible use of red lights Integration with other light systems Testing of general functions and stress test for critical situations Presentation of the new model Marketing brochures Training of sales staff 120.000,00 640.000,00 30.000,00 150.000,00 80.000,00 As the new LED light system is a "break-trough" development, management considers a useful live of 10 years. Company R generally uses the straight line method. For tax purposes R&D expenses cannot be capitalized. Tax rate 25%. Required: Discuss the accounting treatment under IAS 38. Prepare the journal entries to recognize all necessary accounting impacts as of 31 December 2019. Take deferred taxes into account

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts