Question: Case Example - Personal Financial Statements John and Mary Henderson, ages 52 and 48, respectively, are engaging in private wealth management and have the following

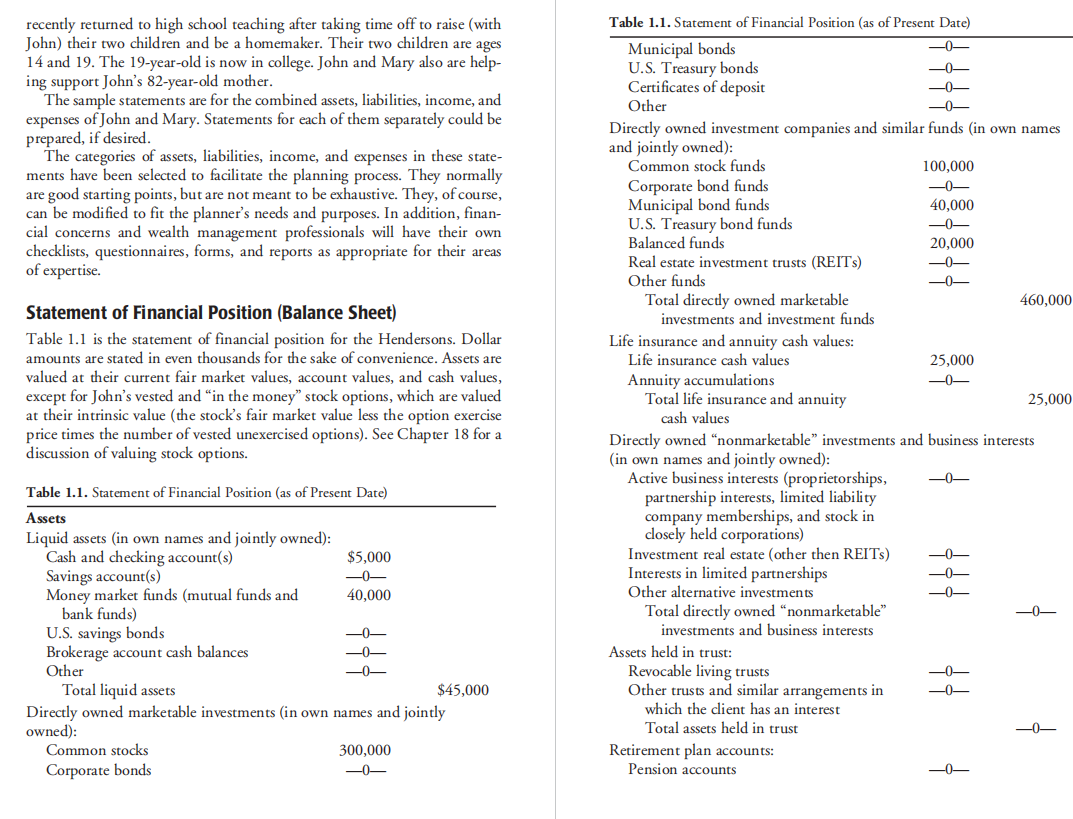

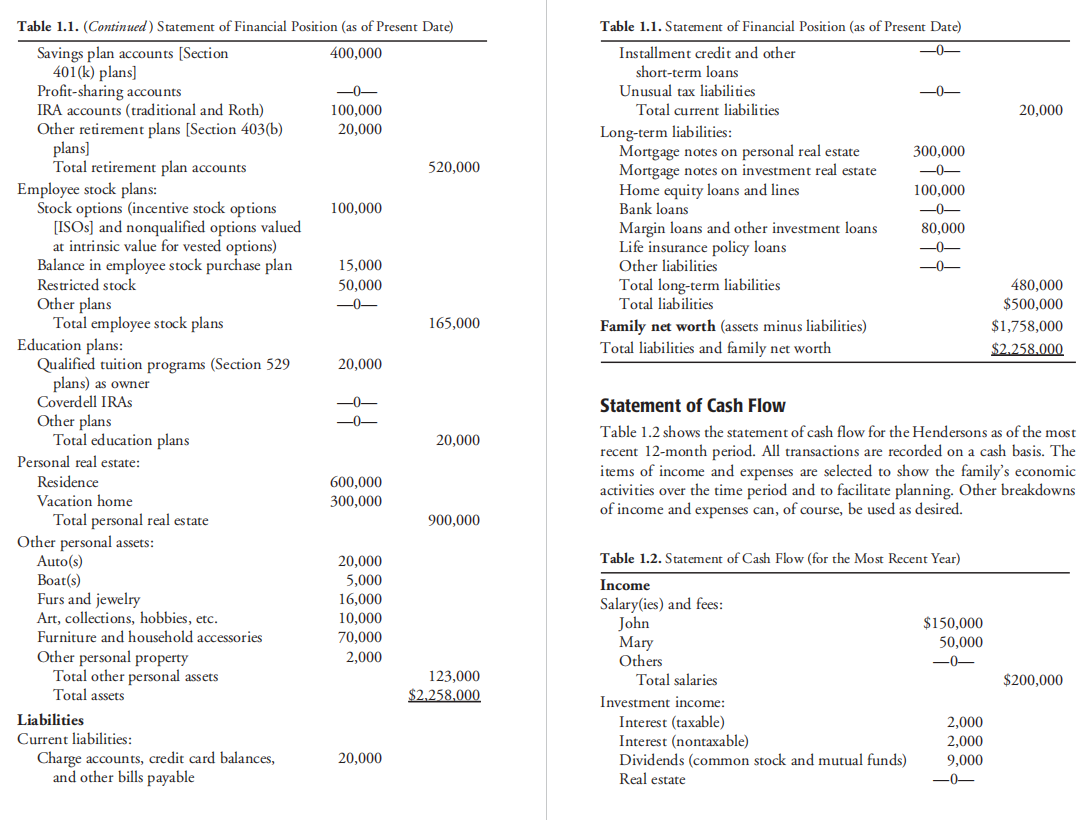

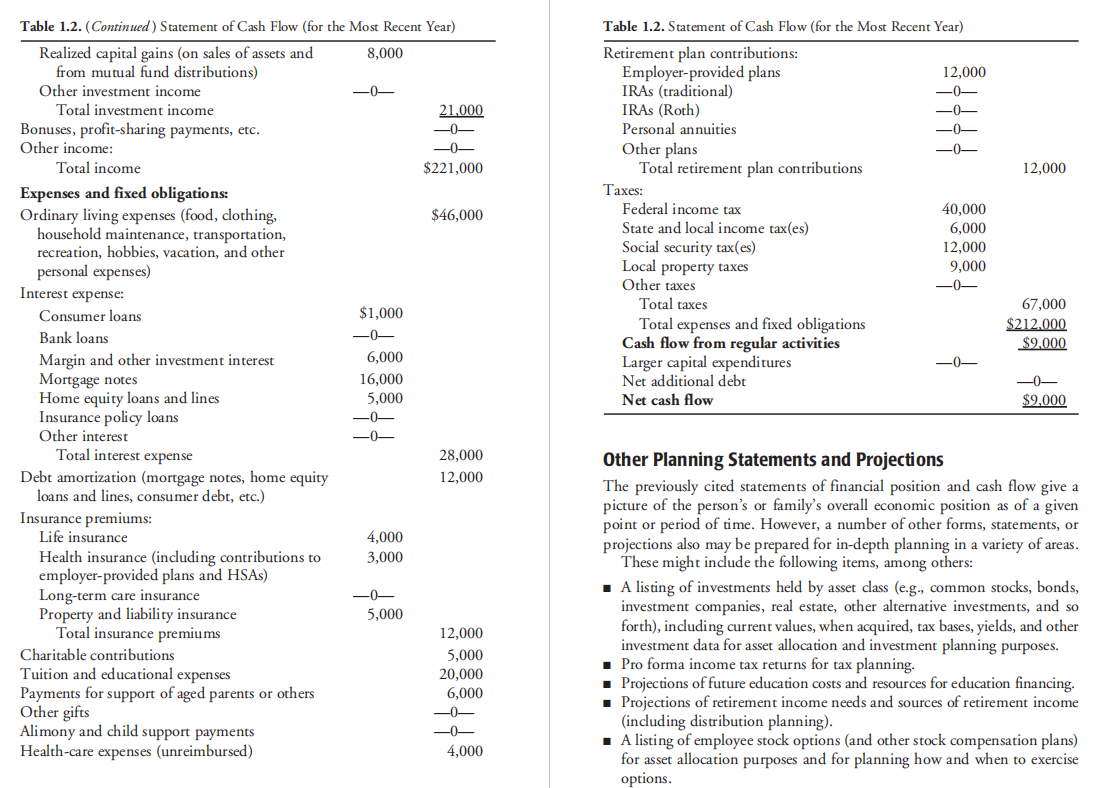

Case Example - Personal Financial Statements John and Mary Henderson, ages 52 and 48, respectively, are engaging in private wealth management and have the following personal financial statements: a statement of financial position and a statement of cash flow. John is a marketing manager for a large publicly traded corporation, while Mary has recently returned to high school teaching after taking time off to raise (with Table 1.1. Statement of Financial Position (as of Present Date) John) their two children and be a homemaker. Their two children are ages 14 and 19. The 19-year-old is now in college. John and Mary also are helping support John's 82 -year-old mother. The sample statements are for the combined assets, liabilities, income, and expenses of John and Mary. Statements for each of them separately could be prepared, if desired. The categories of assets, liabilities, income, and expenses in these statements have been selected to facilitate the planning process. They normally are good starting points, but are not meant to be exhaustive. They, of course, can be modified to fit the planner's needs and purposes. In addition, financial concerns and wealth management professionals will have their own checklists, questionnaires, forms, and reports as appropriate for their areas of expertise. Statement of Financial Position (Balance Sheet) Table 1.1 is the statement of financial position for the Hendersons. Dollar amounts are stated in even thousands for the sake of convenience. Assets are valued at their current fair market values, account values, and cash values, except for John's vested and "in the money" stock options, which are valued at their intrinsic value (the stock's fair market value less the option exercise price times the number of vested unexercised options). See Chapter 18 for a discussion of valuing stock options. Statement of Cash Flow Table 1.2 shows the statement of cash flow for the Hendersons as of the most recent 12 -month period. All transactions are recorded on a cash basis. The items of income and expenses are selected to show the family's economic activities over the time period and to facilitate planning. Other breakdowns of income and expenses can, of course, be used as desired. Other Planning Statements and Projections The previously cited statements of financial position and cash flow give a picture of the person's or family's overall economic position as of a given point or period of time. However, a number of other forms, statements, or projections also may be prepared for in-depth planning in a variety of areas. These might include the following items, among others: - A listing of investments held by asset class (e.g., common stocks, bonds, investment companies, real estate, other alternative investments, and so forth), including current values, when acquired, tax bases, yields, and other investment data for asset allocation and investment planning purposes. - Pro forma income tax returns for tax planning. - Projections of future education costs and resources for education financing. - Projections of retirement income needs and sources of retirement income (including distribution planning). - A listing of employee stock options (and other stock compensation plans) for asset allocation purposes and for planning how and when to exercise options. In our case study on The Hendersons, what is the reason why we could not calculate their Housing-to-Income and Consumer-Debt-to-Income ratios? Case Example - Personal Financial Statements John and Mary Henderson, ages 52 and 48, respectively, are engaging in private wealth management and have the following personal financial statements: a statement of financial position and a statement of cash flow. John is a marketing manager for a large publicly traded corporation, while Mary has recently returned to high school teaching after taking time off to raise (with Table 1.1. Statement of Financial Position (as of Present Date) John) their two children and be a homemaker. Their two children are ages 14 and 19. The 19-year-old is now in college. John and Mary also are helping support John's 82 -year-old mother. The sample statements are for the combined assets, liabilities, income, and expenses of John and Mary. Statements for each of them separately could be prepared, if desired. The categories of assets, liabilities, income, and expenses in these statements have been selected to facilitate the planning process. They normally are good starting points, but are not meant to be exhaustive. They, of course, can be modified to fit the planner's needs and purposes. In addition, financial concerns and wealth management professionals will have their own checklists, questionnaires, forms, and reports as appropriate for their areas of expertise. Statement of Financial Position (Balance Sheet) Table 1.1 is the statement of financial position for the Hendersons. Dollar amounts are stated in even thousands for the sake of convenience. Assets are valued at their current fair market values, account values, and cash values, except for John's vested and "in the money" stock options, which are valued at their intrinsic value (the stock's fair market value less the option exercise price times the number of vested unexercised options). See Chapter 18 for a discussion of valuing stock options. Statement of Cash Flow Table 1.2 shows the statement of cash flow for the Hendersons as of the most recent 12 -month period. All transactions are recorded on a cash basis. The items of income and expenses are selected to show the family's economic activities over the time period and to facilitate planning. Other breakdowns of income and expenses can, of course, be used as desired. Other Planning Statements and Projections The previously cited statements of financial position and cash flow give a picture of the person's or family's overall economic position as of a given point or period of time. However, a number of other forms, statements, or projections also may be prepared for in-depth planning in a variety of areas. These might include the following items, among others: - A listing of investments held by asset class (e.g., common stocks, bonds, investment companies, real estate, other alternative investments, and so forth), including current values, when acquired, tax bases, yields, and other investment data for asset allocation and investment planning purposes. - Pro forma income tax returns for tax planning. - Projections of future education costs and resources for education financing. - Projections of retirement income needs and sources of retirement income (including distribution planning). - A listing of employee stock options (and other stock compensation plans) for asset allocation purposes and for planning how and when to exercise options. In our case study on The Hendersons, what is the reason why we could not calculate their Housing-to-Income and Consumer-Debt-to-Income ratios

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts