Question: Case Study 1 : ACME Limited Dianne Lochan is a senior auditor with Bella Buster and Associates ( Bella Buster ) , an external auditing

Case Study : ACME Limited

Dianne Lochan is a senior auditor with Bella Buster and Associates Bella Buster an external auditing firm based in Oshawa.

Dianne is currently working on the audit of the accounts receivable of Acme Limited Acme one of Bella Busters clients.

During the risk assessment stage, Dianne conducted an audit data analytic using data provided directly by Acme, by grouping Accounts Receivable by days overdue to assess the risk of the accuracy, valuation, and allocation assertion and an overstatement of accounts receivable.

During the past few weeks, Dianne conducted interviews with Acmes accounts receivable manager, its CFO, and the staff working in the accounts receivable department.

Dianne has also overseen the external confirmations of accounts receivable, percent of which required the recipient to respond as to whether or not the amount stated was correct.

Dianne also conducted a review of subsequent cash receipts from Acmes customers. She vouched a sample of accounts receivable balances back to the underlying invoices, cash receipts, and sales returns, and traced a sample of these documents to the accounts receivable ledger.

Required

List the types of audit evidence gathered by Dianne and comment on the persuasiveness of each type.

Link each type of evidence to the relevant accounts receivable assertions.

Case Study : Sampling

Part a

Match the numbered situations below with one of the following types of audit sampling or sampling risk: Statistical sampling or nonstatistical sampling. Sampling risk, Nonsampling risk:

Rather than looking only for authorized signatures, an auditor checked to see if there were any signatures in the credit approval box on a sample of sales orders.

An auditor concluded that, based on a statistical sample, the clients control system was working acceptably when, in fact, the population deviation rate was unacceptable.

Using the laws of probability, an auditor selected a sample and evaluated the results of her sample.

Part b

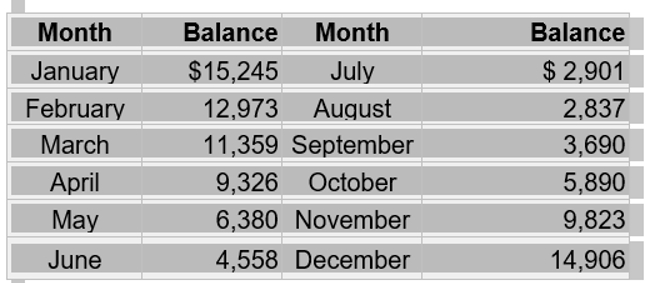

Karina, a firstyear auditor, is asked to select a sample of invoices to audit the utility expense account. Below is the account detail.

Month

Balance

Month

Balance

January

$

July

$

February

August

March

September

April

October

May

November

June

December

The audit program asks to select a sample of four items.

Required

Using systematic selection, determine which four months will be selected.

Using haphazard selection, determine which four months will be selected.

Using block selection, determine which four months will be selected.

begintabularcrcr

hline Month & Balance & Month & Balance

hline January & $ & July & $

hline February & & Auqust &

hline March & & September &

hline April & & October &

hline May & & November &

hline June & & December &

hline

endtabular

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock