Question: Case Study #6: Cash Inquiry Key Information: Client: Carr Parts Company Fiscal year end: December 31 Tolerable misstatement: $50,000 Planned scope for testing outstanding checks

Case Study #6: Cash Inquiry

Key Information:

Client: Carr Parts Company Fiscal year end: December 31 Tolerable misstatement: $50,000 Planned scope for testing outstanding checks = 1/10 of tolerable misstatement Number of Employees = 25

Key Players:

Justin Tyme -- Staff auditor with Smart & Co., LLP Iona Carr -- Owner/President, Carr Parts Company Norma Lee CFO, Carr Parts Company Otto Mobile -- Accounts payable manager Willy Makit -- Bookkeeping clerk

Workpapers:

Bank reconciliations and cancelled checks follow the script below. Justin Tyme refers to them during his inquiry.

Instructions: Read the following client inquiry scenario. Highlight significant audit evidence/issues and identify potential management letter comments. Be prepared to consider Dos and Donts of interviewing techniques based on this given scenario. What would you do differently in this situation? Extra credit for figuring out the actual issues behind the responses to Justins inquiry.

Script Justin Tyme, Staff Accountant: Hi, Norma Lee! Whats happening? (Standing in doorway with chewing gum and a wrinkled shirt.)

Norma Lee, CFO: (Looking frazzled and distracted.) Huh? Oh, hi, Justin Tyme. Did I miss seeing a meeting scheduled with you on my calendar?

Justin Tyme: No, we didnt have anything scheduled, but I have a few quick questions about cash that I wanted to get out of the way. (Walking into the office and sitting down without being invited.)

Norma Lee: (Speaking sarcastically, while looking at watch). Well, why dont you have a seat? Justin Tyme: Thanks, Norma! Im trying to get out of here in time to catch a pick-up basketball

game at the gym and then catch drinks with the fellas. This will just take a minute.

Norma Lee: (Sarcastically again.) Really? Literally, just a minute?

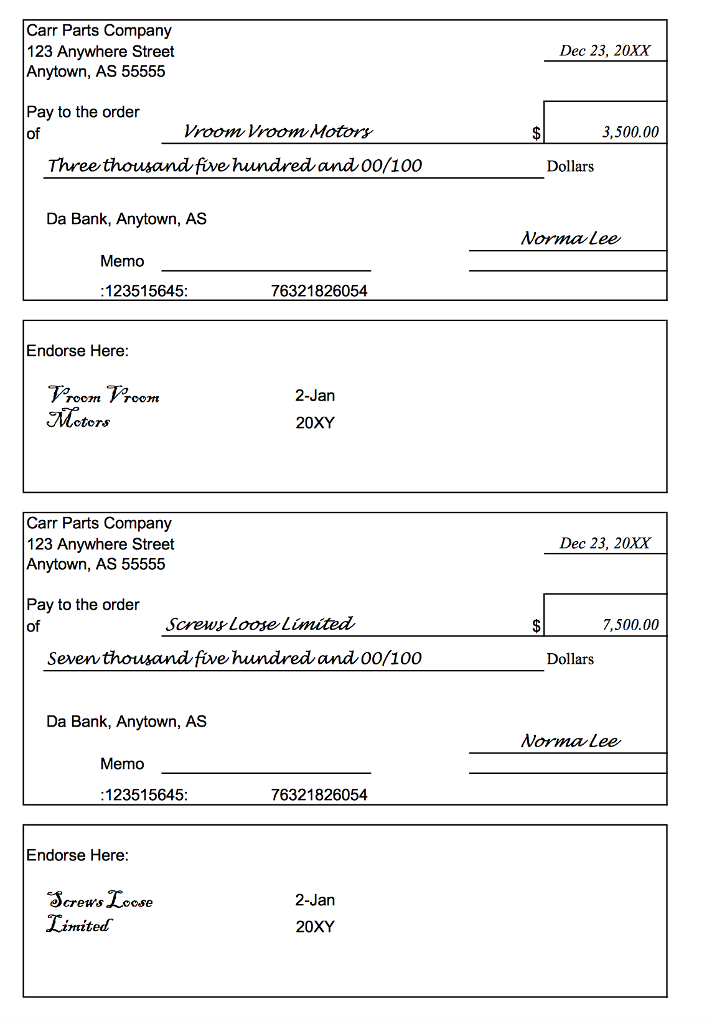

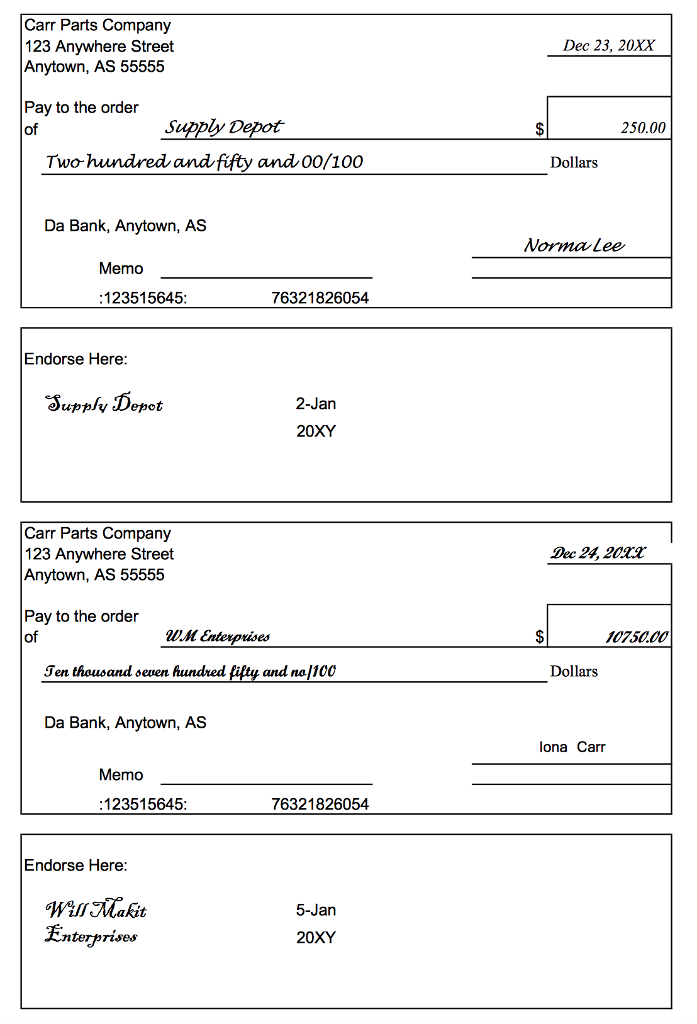

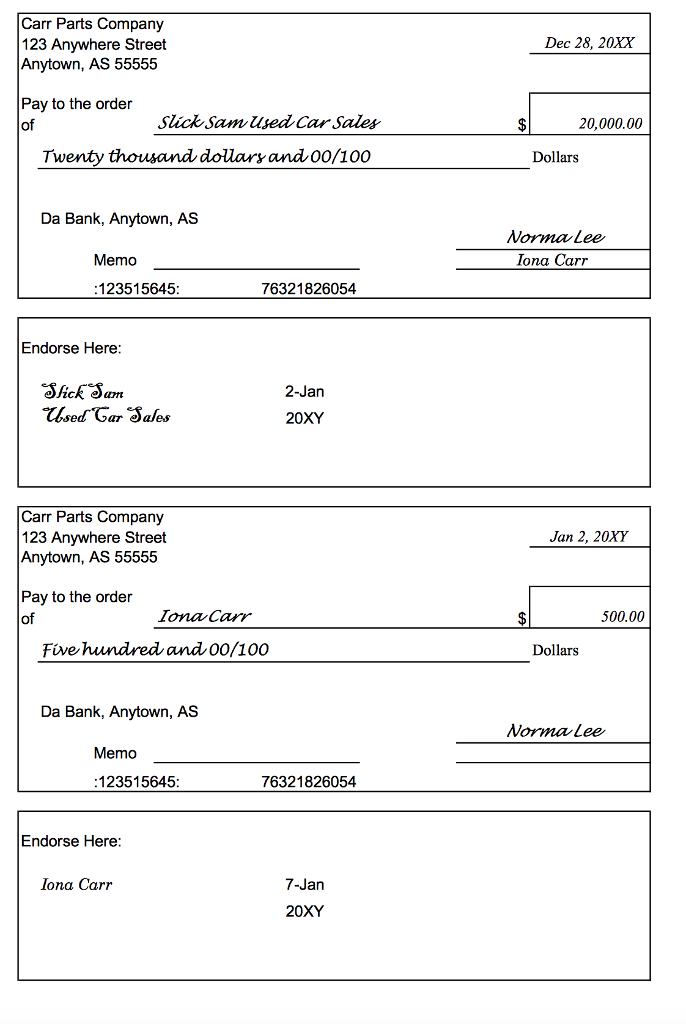

Justin Tyme: Would I lie to you, my friend? Hey, I noticed that theres a $3,000 check on your operating accounts outstanding check list that appears pretty old. Do you know whats up with that?

Norma Lee: No, not really. If you have a check number, I can get Otto Mobile, the accounts payable manager, to look it up for you. I recall there may be a check to one of our vendors that were holding because of a dispute over what we owe.

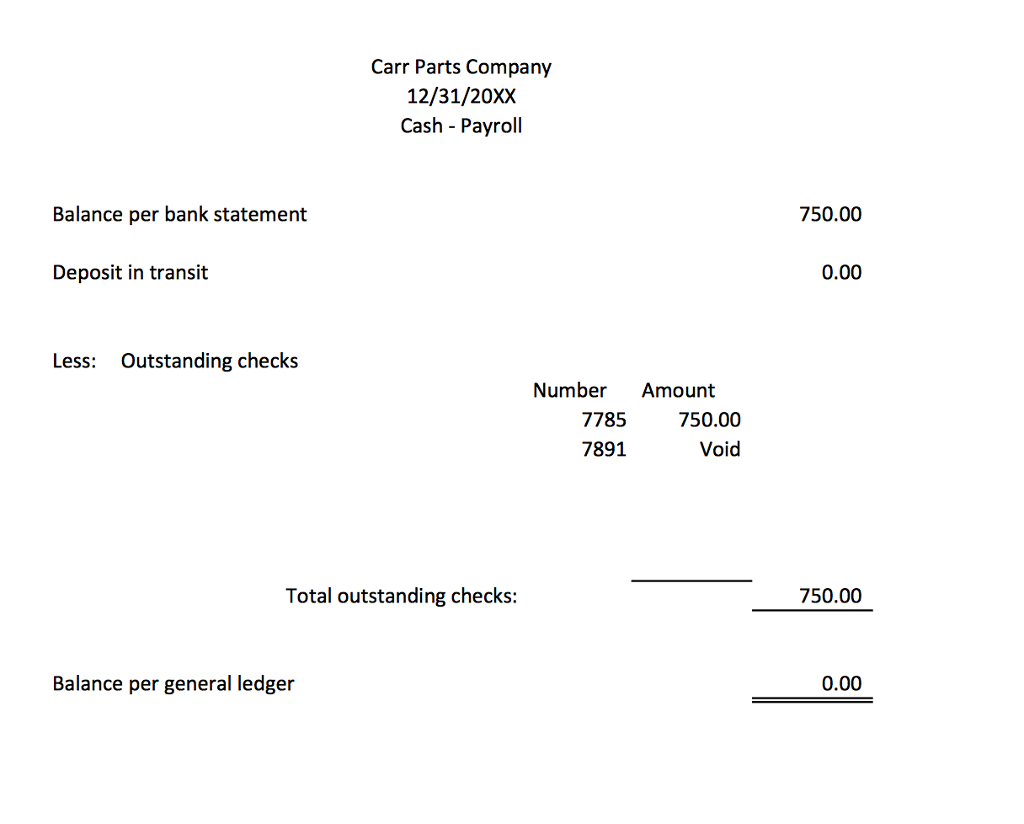

Justin Tyme: Nah, unfortunately I dont have the specific check details. Ill drop that by in the morning, but I cant promise what time because I dont know what time Ill get home tonight! (Laughing a little too loudly.) I also noticed theres a payroll check for $750 outstanding. Any idea what thats about?

Norma Lee: Yes. Its for a bookkeeping clerk, Willy Makit, whos on emergency extended personal leave. He left unexpectedly and didnt have a chance to collect his check. Were just holding onto it until we figure out how to properly handle the situation. Most of the employees have direct deposit, so we usually carry a zero balance right after payroll is processed.

Justin Tyme: Oh. I hope everything is all right. I know that Otto thinks of him as a son. Hey, who are authorized check signers around here again?

Norma Lee: Well, I sign all checks under $10,000. All checks over $10,000 require the signature of Iona Carr, the owner and President.

Justin Tyme: Did you hold any other checks at year-end besides the one you just mentioned? Norma Lee: Not that I recall.

Justin Tyme: (Shuffling through a stack of loose papers.) Uhhmm ...do you have a bank reconciliation for your savings account? I seem to be missing it.

Norma Lee: We actually dont perform a formal reconciliation of the savings account, other than putting in the journal entry request to post the interest earned. I post these adjustments periodically. In fact, I post all the journal entries for cash reconciling items.

Justin Tyme: Okay. Ill just create a bank reconciliation to put in our workpapers for me to document my testing for that account. I dont want to get a review note asking me to do it later. By the way, how often is the operating account reconciled?

Norma Lee: Otto reconciles it by the fifteenth of the following month. He gives the necessary journal entries to me to post.

Justin Tyme: Cool. Who reviews the operating account reconciliation? Norma Lee: Iona. Justin Tyme: Does she ever note anything unusual?

Norma Lee: Well, this month Otto noted an error in the banks posting of check number 6020. The correct amount was $825, not $1,825 as the bank processed it. You will see $1,000 as a reconciling item in December.

Justin Tyme: Oh! So, have you talked to the bank about what happened yet? Norma Lee: (Sitting in silence for a few moments. Looking off in distance and not reacting.) Justin Tyme: (Shifting uncomfortably in seat.) So did you get a credit from the bank yet?

Norma Lee: (Still unresponsive.) Justin Tyme: But your bank account balances otherwise, right?

Norma Lee: (Shaking head like coming out of deep thought.) What? Oh, Im writing up a journal entry to post to correct the error.

Justin Tyme: Wow! Good thing you caught that! Norma Lee: (Looking sullen and distracted.) Yeah, good thing.

Justin Tyme: Hey, I read in last years workpapers that petty cash is generally reconciled monthly with a reimbursement check. However, I didnt see any checks written in December or January to post the current activity.

Norma Lee: The receptionist maintains petty cash. I know I just signed a check in February for $250.

Justin Tyme: What was the petty cash that was being reimbursed used for?

Norma Lee: Typically, its for charitable contributions, postage, and office supplies.

Justin Tyme: Cool. Maybe you can help me with this next one. I was testing some expenses at year-end, and I noted that this $10,750 invoice for WM Enterprises that was paid for with Check #6054 was not approved for payment. Im assuming this is probably an oversight. Was this invoice approval just missed? (Hands invoice to the client, wiping something off it.) Oops! Let me wipe that off! It looks like I got a little careless with my coffee late last night when I was working on this at home.

Norma Lee: Yeah. (Looking a little nervous.) Justin Tyme: Can you tell me more about this company? I notice it has a P.O. Box for an

address.

Norma Lee: (In a very defensive and angry tone.) Look! Whats this all about? I really dont have time to tell you about all of our vendors.

Justin Tyme: Hey, relax! I just want to make sure that this invoice was properly approved. Norma Lee: (Very assertively.) Trust me, it was!

Justin Tyme: Great! Ill document it that way as an isolated exception. Are you aware of any accounts subject to withdrawal restrictions or designated for a special purpose?

Norma Lee: No. (Looking very annoyed and answering very curtly.)

Justin Tyme: (Looking uncomfortable and uncertain about what to do.) Uhhmm ...I guess Ill be going now. See you tomorrow. (Rushing out quickly without saying thank you, shaking hands, or waiting for a response.)

Norma Lee: (Shakes head and puts head in hands.)

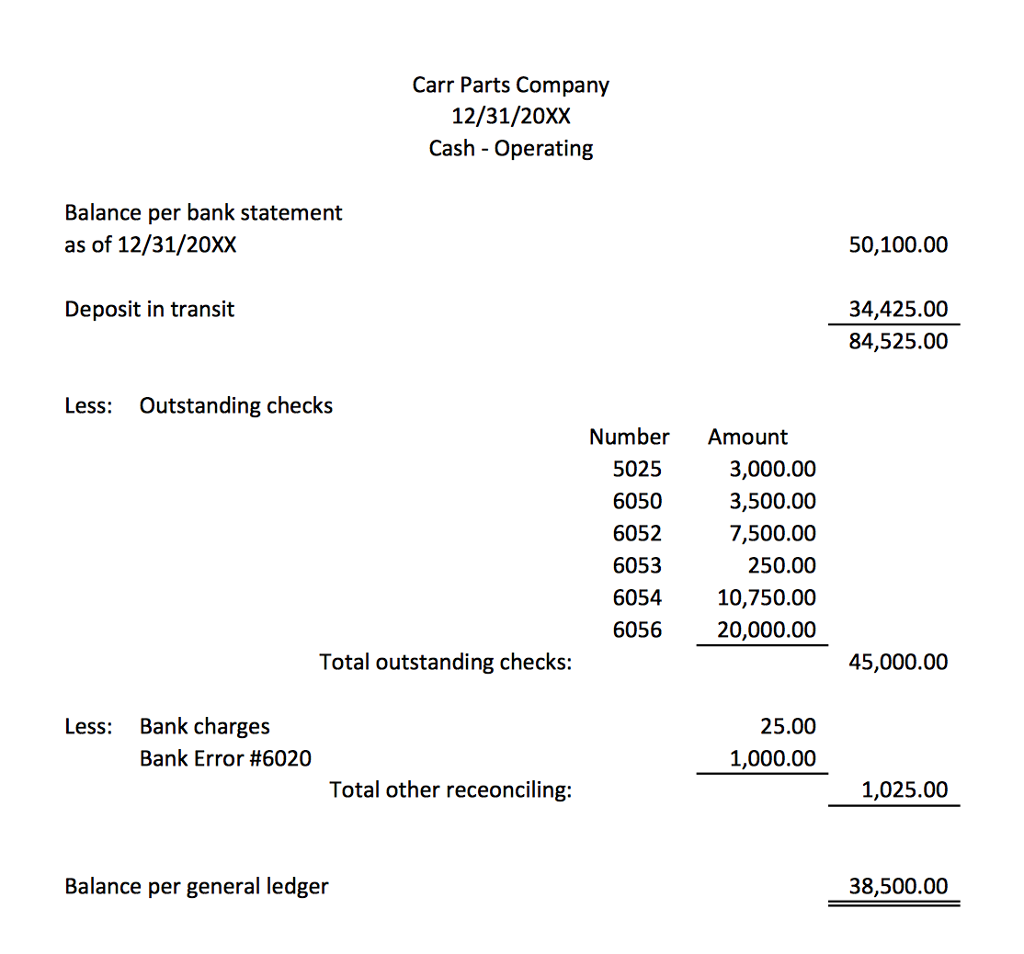

Carr Parts Company 12/31/20 XX Cash Operating Balance per bank statement as of 12/3 1/20XX Deposit in transit Less: Outstanding checks Number Amount 5025 3,000.00 6050 3,500.00 6052 7,500.00 6053 250.00 6054 10,750.00 6056 20,000.00 Total outstanding checks: Less: Bank charges 25.000 1,000.00 Bank Error #6020 Total other receonciling: Balance per general ledger 50,100.00 34,425.00 84,525.00 45,000.00 1,025.00 38,500.00 Carr Parts Company 12/31/20 XX Cash Operating Balance per bank statement as of 12/3 1/20XX Deposit in transit Less: Outstanding checks Number Amount 5025 3,000.00 6050 3,500.00 6052 7,500.00 6053 250.00 6054 10,750.00 6056 20,000.00 Total outstanding checks: Less: Bank charges 25.000 1,000.00 Bank Error #6020 Total other receonciling: Balance per general ledger 50,100.00 34,425.00 84,525.00 45,000.00 1,025.00 38,500.00

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts