Question: Case Study Question1. A) Identify External factors (0, T) and create EFAS summary similar to Table 4.5 B) Identify Internal factors (S, W) and create

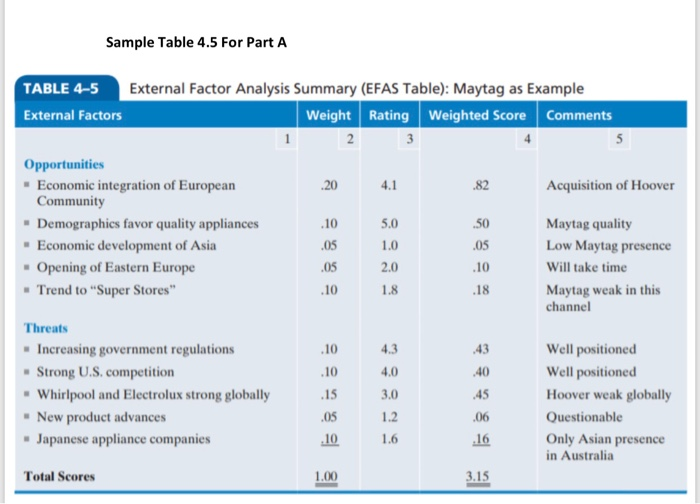

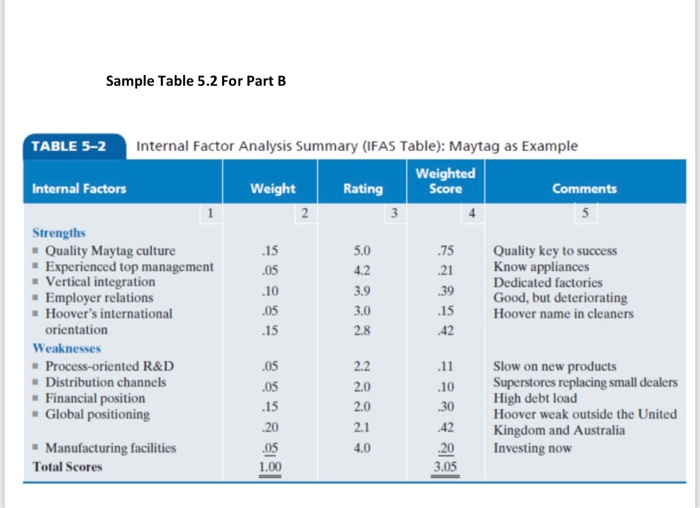

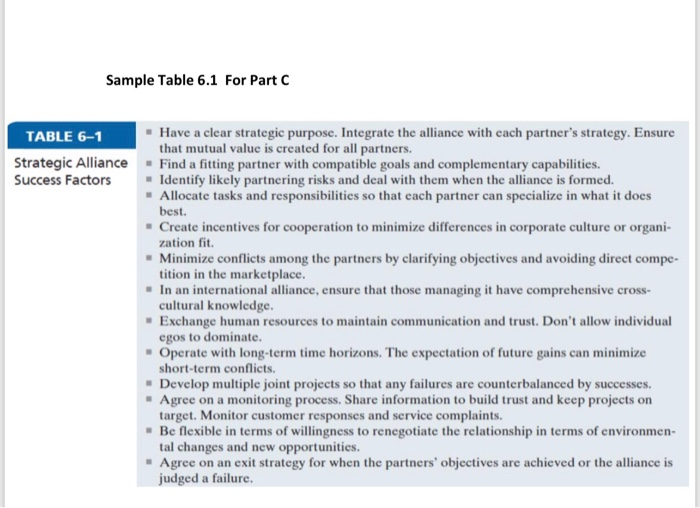

Case Study Question1. A) Identify External factors (0, T) and create EFAS summary similar to Table 4.5 B) Identify Internal factors (S, W) and create IFAS summary similar to Table 5.2 C) Identify strategic factors (SF) and create SFAS summary similar to Table 6.1 Emirates Airlines (EA) continues to overcome sovereign concerns as international rivals oppose EA's expansion into new and existing markets. In Sep 2013, EA launched new strategic and historic partnerships with Australian flagship carrier Qantas. In the deal Qantas moved its Australia-to-London Kangaroo Route" international hub from Asia to Dubai. 1. Passenger traffic out of Australasia rose 41.3 per cent in October compared to the same period last year. In September there was a 38.6 per cent increase compared to the same period in 2012. The relationship is clearly driving traffic not only through hub but into Dubai - where according to the Australian Consulate in Dubai up to 10,000 Australians now visit the UAE each week. 2. In Oct 2013, Etihad Airways announced it will be taking a 33.3 per cent stake in little known European regional airline Darwin Airlines, which will be rebranded "Etihad Regional - operated by Darwin Airlines". UAE's budget carriers, too, have expanded reach in 2013. Dubai-based flydubai announced 16 new routes in the year, besides increasing the frequency of several destinations across its network of 66 destinations. Sharjah's Air Arabia, meanwhile, added eight new airports to its route network in the year including Sialkot in Pakistan, Baghdad in Iraq, Lar and Mashhad in Iran, Yerevan in Armenia, and three Saudi routes - Abha, Hail and Hofuf. 3. The UAE's reputation as a global aviation hub also received an immediate boost on Wednesday night following the announcement Dubai will host Expo 2020. Expo 2020 is expected to draw 25 million visitors to Dubai with 70 per cent coming from overseas. New dynamics within the global aviation industry emerged at the recent Dubai Air Show and cannot be ignored as they will impact the future of air transport and reshape power centers for regional and international airlines. s. The first is the increasingly central role of Gulf-based carriers, particularly Emirates, Etihad and Qatar Airways, which together account for more than 80 per cent of the deals through 610 new aircraft worth $280 billion, and including the 510 jet ordered by the UAE airlines. 6. Aircraft manufacturers have realized the importance of cooperation with Gulf carriers who now acquire a large portion of their purchases, alongside European, American and Chinese orders. 7. In the aviation industry, Gulf countries will no longer be content with playing the role of a customer but will seek to gain aviation technologies. This will not be through complete manufacturing operations, as is the case in China which has started producing some Airbus planes, but through manufacturing parts for Airbus and Boeing, as is the case in the UAE, and the training of Emirati citizens and local workers to develop their skills and experience in the aerospace industry. GCC airlines have become a major player in contributing to the development of aviation technologies and easing of air traffic, thanks to their bold and thoughtful policies. It is also due to their investment in air transport infrastructure, which has developed rapidly in the past two decades that allowed them to compete with other centers in the world. . Dubai's economy has been on an upswing this year so far, driven by services, transportation, logistics, retail and tourism sectors, Simon Williams, chief economist for Middle East and North Africa at HSBC told Gulf News. 10. The emirate has recovered from the corporate debt crisis and real estate slump which it faced in 2009 and 2010 by enhancing its position as a major destination for travel and investment from the Middle East and Europe. 11. Dubai's real gross domestic product (GDP) is projected to climb 4.7 per cent in 2013, and by 4.5 per cent in 2014, according to estimates by Dubai's Department of Economic Development (DED). 12. The growth rate of Dubai's GDP stood at 4.7 per cent for the second quarter of 2013, compared to the same period a year ago, according to the Dubai Economic Outlook (DEO), Quarter 2/2013 report, issued by the Secretariat General of the Dubai Economic Council (DEC). The growth was driven by the wholesale and retail, transportation, manufacturing and real estate sectors. 13. Housing prices have increased as a result of an improvement in the economic environment and strong demand. Giyas Gokkent, chief economist at National Bank of Abu Dhabi (NBAD), pointed out that as of September 2013, average residential property prices in Dubai were up 34 per cent, over September 2012." 14. Although house prices in Dubai have climbed by more than 20 per cent in the last year, analysts told Gulf News previously that prices do not point to a property bubble. 15. The International Monetary Fund (IMF) estimated that Dubai's current debts, including the debt outstanding of government-related entities (GREs), stand at 100 per cent of its GDP 16. Gokkent estimates that UAE's economy in 2014-15 is estimated to reach 4.1 per cent (from 4.5% in 2013-14) "due to slow oil sector growth. 17. The annual Invesco Middle East Asset Management Study, which examines the asset management industry in the GCC (Gulf Cooperation Council) countries, showed that 43 per cent of funds entering into the UAE come from emerging markets, including India, China and Russia. The study indicated that, alongside investment opportunities, the UAE's political stability is driving the capital flow. 18. Emirates airline has posted a profit of Dhs2.3 billion ($622 million) for the financial year 2012-13, an increase of 52 per cent over last year's results. 19. The Dubai-government owned airline recorded revenue of Dhs73.1 billion ($19.9 billion) for the financial year 2012-13, up 17 per cent on last year. 20. The number of passengers carried by the airline rose by 15 per cent to 39.4 million, while seat factor stayed at 80 per cent, the same as last year's. 21. Although the average price of jet fuel did not increase over last year, it remains high and has impacted Emirates' bottom line, the company said in a statement. 22. In the 2012-13 financial year Emirates' fuel bill increased by 15 per cent over last year to reach Dhs27.9 billion (S7.6 billion). 23. The airline received 34 new aircraft in the last year, and has a further 198 aircraft on order worth over $71 billion. 24 Emirates raised more than Dhs28.6 billion ($7.8 billion) last year in new funding mainly to secure its on-going fleet expansion. 25. The airline also issued a 10-year Sukuk (Islamic Bond) for $1 billion and raised $750 million with a 12-year bond matched to the payment cycle for the aircraft. 26. Revenue generated from across Emirates' six regions continues to be well balanced, with no region contributing more than 30 per cent of overall revenues. 27. The state-owned Dubai airline was set to gain from its recent alliance agreement with Australian carrier Qantas. If anything, both carriers will benefit. There will be no net losses here. With Qantas now bringing in a swathe of traffic to Dubai that once flew through places like Singapore, Emirates can leverage its excellent Dubai hub to provide capacity and connections for even more travellers. This is a win-win situation for Qantas and Emirates alike. 28. "Although the airline does not pay taxes, it incurs a lot of other social costs, such as medical, education and family accommodation for its large employee base that has a direct contribution to the economy. 29. EA have a less than 5 per cent attrition rate since it offers the best packages to its employees and at the end of the day, they are the driver of growth. Sample Table 4.5 For Part A TABLE 4-5 External Factor Analysis Summary (EFAS Table): Maytag as Example External Factors Weight Rating Weighted Score Comments 2 3 5 Opportunities - Economic integration of European .20 4.1 .82 Acquisition of Hoover Community Demographics favor quality appliances .10 5.0 .50 Maytag quality - Economic development of Asia .05 1.0 .05 Low Maytag presence Opening of Eastern Europe .05 2.0 .10 Will take time - Trend to "Super Stores" Maytag weak in this channel Threats - Increasing government regulations .10 4.3 .43 Well positioned Strong U.S. competition .10 4.0 .40 Well positioned Whirlpool and Electrolux strong globally .45 Hoover weak globally New product advances 1.2 .06 Questionable Japanese appliance companies .10 1.6 Only Asian presence in Australia Total Scores 1.00 3.15 .10 1.8 .18 .15 3.0 .05 .16 Sample Table 5.2 For Part B TABLE 5-2 Internal Factor Analysis Summary (IFAS Table): Maytag as Example Weighted Internal factors Weight Rating Score Comments 2 3 5 Strengths Quality Maytag culture .15 5.0 .75 Quality key to success Experienced top management .05 4.2 .21 Know appliances Vertical integration .10 Employer relations 3.9 .39 Dedicated factories Good, but deteriorating Hoover's international .05 3.0 .15 Hoover name in cleaners orientation .15 2.8 .42 Weaknesses Process-oriented R&D .05 2.2 .11 Slow on new products - Distribution channels .05 2.0 .10 Superstores replacing small dealers - Financial position .15 Global positioning .30 High debt load Hoover weak outside the United .20 2.1 .42 Kingdom and Australia - Manufacturing facilities .05 4.0 .20 Investing now Total Scores 3.05 2.0 1.00 Sample Table 6.1 For Part TABLE 6-1 Have a clear strategic purpose. Integrate the alliance with each partner's strategy. Ensure that mutual value is created for all partners. Strategic Alliance - Find a fitting partner with compatible goals and complementary capabilities. Success Factors - Identify likely partnering risks and deal with them when the alliance is formed. Allocate tasks and responsibilities so that each partner can specialize in what it does best. Create incentives for cooperation to minimize differences in corporate culture or organi- zation fit. - Minimize conflicts among the partners by clarifying objectives and avoiding direct compe- tition in the marketplace. - In an international alliance, ensure that those managing it have comprehensive cross- cultural knowledge. Exchange human resources to maintain communication and trust. Don't allow individual egos to dominate. - Operate with long-term time horizons. The expectation of future gains can minimize short-term conflicts. - Develop multiple joint projects so that any failures are counterbalanced by successes. Agree on a monitoring process. Share information to build trust and keep projects on target. Monitor customer responses and service complaints. - Be flexible in terms of willingness to renegotiate the relationship in terms of environmen- tal changes and new opportunities. Agree on an exit strategy for when the partners' objectives are achieved or the alliance is judged a failure. Case Study Question1. A) Identify External factors (0, T) and create EFAS summary similar to Table 4.5 B) Identify Internal factors (S, W) and create IFAS summary similar to Table 5.2 C) Identify strategic factors (SF) and create SFAS summary similar to Table 6.1 Emirates Airlines (EA) continues to overcome sovereign concerns as international rivals oppose EA's expansion into new and existing markets. In Sep 2013, EA launched new strategic and historic partnerships with Australian flagship carrier Qantas. In the deal Qantas moved its Australia-to-London Kangaroo Route" international hub from Asia to Dubai. 1. Passenger traffic out of Australasia rose 41.3 per cent in October compared to the same period last year. In September there was a 38.6 per cent increase compared to the same period in 2012. The relationship is clearly driving traffic not only through hub but into Dubai - where according to the Australian Consulate in Dubai up to 10,000 Australians now visit the UAE each week. 2. In Oct 2013, Etihad Airways announced it will be taking a 33.3 per cent stake in little known European regional airline Darwin Airlines, which will be rebranded "Etihad Regional - operated by Darwin Airlines". UAE's budget carriers, too, have expanded reach in 2013. Dubai-based flydubai announced 16 new routes in the year, besides increasing the frequency of several destinations across its network of 66 destinations. Sharjah's Air Arabia, meanwhile, added eight new airports to its route network in the year including Sialkot in Pakistan, Baghdad in Iraq, Lar and Mashhad in Iran, Yerevan in Armenia, and three Saudi routes - Abha, Hail and Hofuf. 3. The UAE's reputation as a global aviation hub also received an immediate boost on Wednesday night following the announcement Dubai will host Expo 2020. Expo 2020 is expected to draw 25 million visitors to Dubai with 70 per cent coming from overseas. New dynamics within the global aviation industry emerged at the recent Dubai Air Show and cannot be ignored as they will impact the future of air transport and reshape power centers for regional and international airlines. s. The first is the increasingly central role of Gulf-based carriers, particularly Emirates, Etihad and Qatar Airways, which together account for more than 80 per cent of the deals through 610 new aircraft worth $280 billion, and including the 510 jet ordered by the UAE airlines. 6. Aircraft manufacturers have realized the importance of cooperation with Gulf carriers who now acquire a large portion of their purchases, alongside European, American and Chinese orders. 7. In the aviation industry, Gulf countries will no longer be content with playing the role of a customer but will seek to gain aviation technologies. This will not be through complete manufacturing operations, as is the case in China which has started producing some Airbus planes, but through manufacturing parts for Airbus and Boeing, as is the case in the UAE, and the training of Emirati citizens and local workers to develop their skills and experience in the aerospace industry. GCC airlines have become a major player in contributing to the development of aviation technologies and easing of air traffic, thanks to their bold and thoughtful policies. It is also due to their investment in air transport infrastructure, which has developed rapidly in the past two decades that allowed them to compete with other centers in the world. . Dubai's economy has been on an upswing this year so far, driven by services, transportation, logistics, retail and tourism sectors, Simon Williams, chief economist for Middle East and North Africa at HSBC told Gulf News. 10. The emirate has recovered from the corporate debt crisis and real estate slump which it faced in 2009 and 2010 by enhancing its position as a major destination for travel and investment from the Middle East and Europe. 11. Dubai's real gross domestic product (GDP) is projected to climb 4.7 per cent in 2013, and by 4.5 per cent in 2014, according to estimates by Dubai's Department of Economic Development (DED). 12. The growth rate of Dubai's GDP stood at 4.7 per cent for the second quarter of 2013, compared to the same period a year ago, according to the Dubai Economic Outlook (DEO), Quarter 2/2013 report, issued by the Secretariat General of the Dubai Economic Council (DEC). The growth was driven by the wholesale and retail, transportation, manufacturing and real estate sectors. 13. Housing prices have increased as a result of an improvement in the economic environment and strong demand. Giyas Gokkent, chief economist at National Bank of Abu Dhabi (NBAD), pointed out that as of September 2013, average residential property prices in Dubai were up 34 per cent, over September 2012." 14. Although house prices in Dubai have climbed by more than 20 per cent in the last year, analysts told Gulf News previously that prices do not point to a property bubble. 15. The International Monetary Fund (IMF) estimated that Dubai's current debts, including the debt outstanding of government-related entities (GREs), stand at 100 per cent of its GDP 16. Gokkent estimates that UAE's economy in 2014-15 is estimated to reach 4.1 per cent (from 4.5% in 2013-14) "due to slow oil sector growth. 17. The annual Invesco Middle East Asset Management Study, which examines the asset management industry in the GCC (Gulf Cooperation Council) countries, showed that 43 per cent of funds entering into the UAE come from emerging markets, including India, China and Russia. The study indicated that, alongside investment opportunities, the UAE's political stability is driving the capital flow. 18. Emirates airline has posted a profit of Dhs2.3 billion ($622 million) for the financial year 2012-13, an increase of 52 per cent over last year's results. 19. The Dubai-government owned airline recorded revenue of Dhs73.1 billion ($19.9 billion) for the financial year 2012-13, up 17 per cent on last year. 20. The number of passengers carried by the airline rose by 15 per cent to 39.4 million, while seat factor stayed at 80 per cent, the same as last year's. 21. Although the average price of jet fuel did not increase over last year, it remains high and has impacted Emirates' bottom line, the company said in a statement. 22. In the 2012-13 financial year Emirates' fuel bill increased by 15 per cent over last year to reach Dhs27.9 billion (S7.6 billion). 23. The airline received 34 new aircraft in the last year, and has a further 198 aircraft on order worth over $71 billion. 24 Emirates raised more than Dhs28.6 billion ($7.8 billion) last year in new funding mainly to secure its on-going fleet expansion. 25. The airline also issued a 10-year Sukuk (Islamic Bond) for $1 billion and raised $750 million with a 12-year bond matched to the payment cycle for the aircraft. 26. Revenue generated from across Emirates' six regions continues to be well balanced, with no region contributing more than 30 per cent of overall revenues. 27. The state-owned Dubai airline was set to gain from its recent alliance agreement with Australian carrier Qantas. If anything, both carriers will benefit. There will be no net losses here. With Qantas now bringing in a swathe of traffic to Dubai that once flew through places like Singapore, Emirates can leverage its excellent Dubai hub to provide capacity and connections for even more travellers. This is a win-win situation for Qantas and Emirates alike. 28. "Although the airline does not pay taxes, it incurs a lot of other social costs, such as medical, education and family accommodation for its large employee base that has a direct contribution to the economy. 29. EA have a less than 5 per cent attrition rate since it offers the best packages to its employees and at the end of the day, they are the driver of growth. Sample Table 4.5 For Part A TABLE 4-5 External Factor Analysis Summary (EFAS Table): Maytag as Example External Factors Weight Rating Weighted Score Comments 2 3 5 Opportunities - Economic integration of European .20 4.1 .82 Acquisition of Hoover Community Demographics favor quality appliances .10 5.0 .50 Maytag quality - Economic development of Asia .05 1.0 .05 Low Maytag presence Opening of Eastern Europe .05 2.0 .10 Will take time - Trend to "Super Stores" Maytag weak in this channel Threats - Increasing government regulations .10 4.3 .43 Well positioned Strong U.S. competition .10 4.0 .40 Well positioned Whirlpool and Electrolux strong globally .45 Hoover weak globally New product advances 1.2 .06 Questionable Japanese appliance companies .10 1.6 Only Asian presence in Australia Total Scores 1.00 3.15 .10 1.8 .18 .15 3.0 .05 .16 Sample Table 5.2 For Part B TABLE 5-2 Internal Factor Analysis Summary (IFAS Table): Maytag as Example Weighted Internal factors Weight Rating Score Comments 2 3 5 Strengths Quality Maytag culture .15 5.0 .75 Quality key to success Experienced top management .05 4.2 .21 Know appliances Vertical integration .10 Employer relations 3.9 .39 Dedicated factories Good, but deteriorating Hoover's international .05 3.0 .15 Hoover name in cleaners orientation .15 2.8 .42 Weaknesses Process-oriented R&D .05 2.2 .11 Slow on new products - Distribution channels .05 2.0 .10 Superstores replacing small dealers - Financial position .15 Global positioning .30 High debt load Hoover weak outside the United .20 2.1 .42 Kingdom and Australia - Manufacturing facilities .05 4.0 .20 Investing now Total Scores 3.05 2.0 1.00 Sample Table 6.1 For Part TABLE 6-1 Have a clear strategic purpose. Integrate the alliance with each partner's strategy. Ensure that mutual value is created for all partners. Strategic Alliance - Find a fitting partner with compatible goals and complementary capabilities. Success Factors - Identify likely partnering risks and deal with them when the alliance is formed. Allocate tasks and responsibilities so that each partner can specialize in what it does best. Create incentives for cooperation to minimize differences in corporate culture or organi- zation fit. - Minimize conflicts among the partners by clarifying objectives and avoiding direct compe- tition in the marketplace. - In an international alliance, ensure that those managing it have comprehensive cross- cultural knowledge. Exchange human resources to maintain communication and trust. Don't allow individual egos to dominate. - Operate with long-term time horizons. The expectation of future gains can minimize short-term conflicts. - Develop multiple joint projects so that any failures are counterbalanced by successes. Agree on a monitoring process. Share information to build trust and keep projects on target. Monitor customer responses and service complaints. - Be flexible in terms of willingness to renegotiate the relationship in terms of environmen- tal changes and new opportunities. Agree on an exit strategy for when the partners' objectives are achieved or the alliance is judged a failure

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts