Question: CASE STUDY: WASHINGTON TOWER Property/Analysis Data Washington Tower is a 60,000 SF office building located at 140 Washington Avenue, Houston, TX. The subject property was

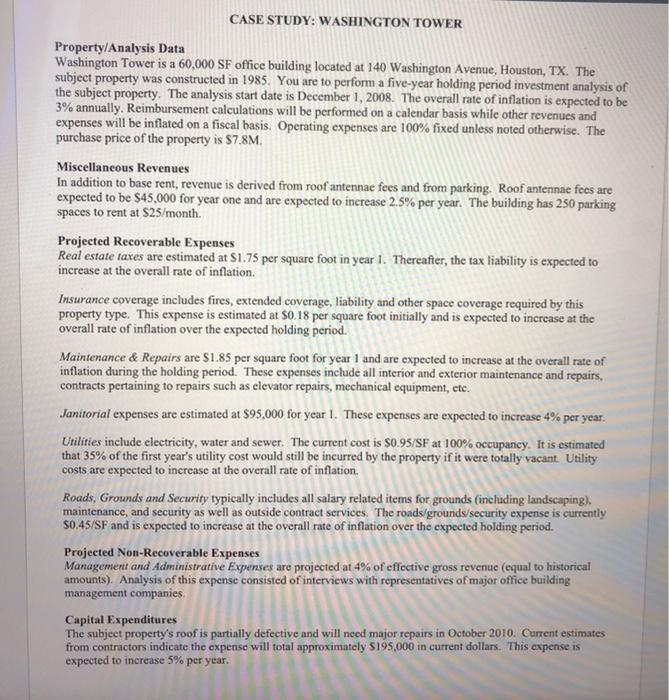

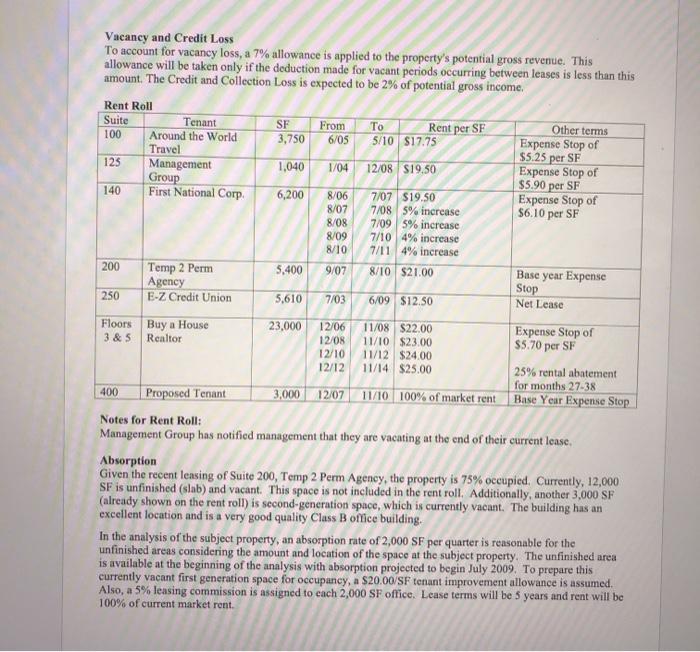

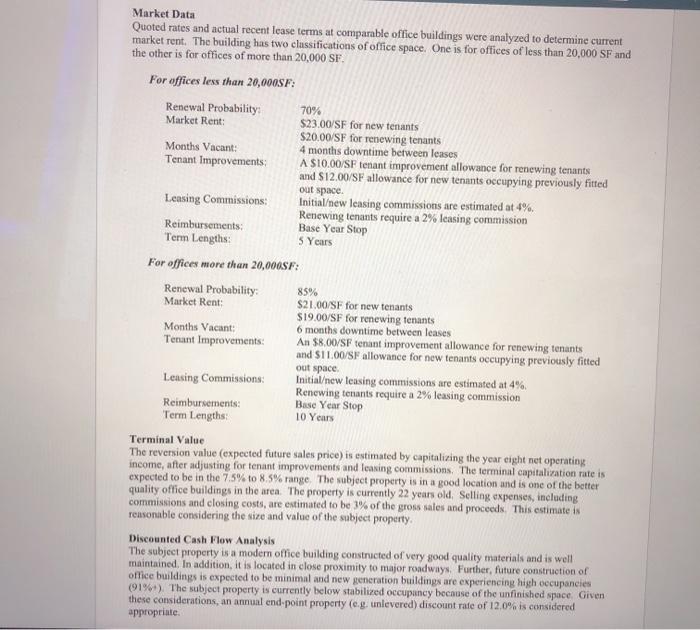

CASE STUDY: WASHINGTON TOWER Property/Analysis Data Washington Tower is a 60,000 SF office building located at 140 Washington Avenue, Houston, TX. The subject property was constructed in 1985. You are to perform a five-year holding period investment analysis of the subject property. The analysis start date is December 1, 2008. The overall rate of inflation is expected to be 3% annually. Reimbursement calculations will be performed on a calendar basis while other revenues and expenses will be inflated on a fiscal basis. Operating expenses are 100% fixed unless noted otherwise. The purchase price of the property is $7.8M. Miscellaneous Revenues In addition to base rent, revenue is derived from roof antennae fees and from parking. Roof antennae fees are expected to be $45,000 for year one and are expected to increase 2.5% per year. The building has 250 parking spaces to rent at $25/month. Projected Recoverable Expenses Real estate taxes are estimated at $1.75 per square foot in year 1. Thereafter, the tax liability is expected to increase at the overall rate of inflation. Insurance coverage includes fires, extended coverage, liability and other space coverage required by this property type. This expense is estimated at $0.18 per square foot initially and is expected to increase at the overall rate of inflation over the expected holding period. Maintenance & Repairs are $1.85 per square foot for year 1 and are expected to increase at the overall rate of inflation during the holding period. These expenses include all interior and exterior maintenance and repairs, contracts pertaining to repairs such as elevator repairs, mechanical equipment, etc. Janitorial expenses are estimated at 895,000 for year 1. These expenses are expected to increase 4% per year. Utilities include electricity, water and sewer. The current cost is $0.95/SF at 100% occupancy. It is estimated that 35% of the first year's utility cost would still be incurred by the property if it were totally vacant. Utility costs are expected to increase at the overall rate of inflation. Roads, Grounds and Security typically includes all salary related items for grounds (including landscaping). maintenance, and security as well as outside contract services. The roads/grounds/security expense is currently 0.45/SF and is expected to increase at the overall rate of inflation over the expected holding period. Projected Non-Recoverable Expenses Management and Administrative Expenses are projected at 4% of effective gross revenue (equal to historical amounts). Analysis of this expense consisted of interviews with representatives of major office building management companies. Capital Expenditures The subject property's roof is partially defective and will need major repairs in October 2010. Current estimates from contractors indicate the expense will total approximately $195,000 in current dollars. This expense is expected to increase 5% per year. Vacancy and Credit Loss To account for vacancy loss, a 7% allowance is applied to the property's potential gross revenue. This allowance will be taken only if the deduction made for vacant periods occurring between leases is less than this amount. The Credit and Collection Loss is expected to be 2% of potential gross income. Rent Roll Suite Tenant SF From To Rent per SF Other terms 100 Around the World 3,750 6/05 5/10 $17.75 Expense Stop of Travel $5.25 per SE 125 Management 1,040 1/04 12/08 $19.50 Expense Stop of Group $5.90 per SF 140 First National Corp 6,200 8/06 7/07 $19.50 Expense Stop of 8/07 7/08 5% increase $6.10 per SF 8/08 7/09 5% increase 8/09 7/10 4% increase 8/10 7/11 4% increase 200 Temp 2 Perm 5.400 9/07 8/10 $21.00 Base year Expense Agency Stop 250 E-Z Credit Union 5,610 7/03 6/09 $12.50 Net Lease Floors Buy a House 23,000 12/06 11/08 $22.00 Expense Stop of 3 & 5 Realtor 12/08 11/10 $23.00 $5.70 per SF 12/10 11/12 $24.00 12/12 11/14 $25.00 25% rental abatement for months 27-38 400 Proposed Tenant 3,000 12/07 11/10 100% of market rent Base Year Expense Stop Notes for Rent Roll: Management Group has notified management that they are vacating at the end of their current lease. Absorption Given the recent leasing of Suite 200, Temp 2 Perm Agency, the property is 75% occupied. Currently, 12,000 SF is unfinished (slab) and vacant. This space is not included in the rent roll. Additionally, another 3,000 SF (already shown on the rent roll) is second-generation space, which is currently vacant. The building has an excellent location and is a very good quality Class B office building. In the analysis of the subject property, an absorption rate of 2,000 SF per quarter is reasonable for the unfinished areas considering the amount and location of the space at the subject property. The unfinished area is available at the beginning of the analysis with absorption projected to begin July 2009. To prepare this currently vacant first generation space for occupancy, a $20.00/SF tenant improvement allowance is assumed. Also, a 5% leasing commission is assigned to each 2,000 SF office. Lease terms will be 5 years and rent will be 100% of current market rent. Market Data Quoted rates and actual recent lease terms at comparable office buildings were analyzed to determine current market rent. The building has two classifications of office space. One is for offices of less than 20,000 SF and the other is for offices of more than 20,000 SF. For offices less than 20,000SF: Renewal Probability 70% Market Rent $23.00/SF for new tenants $20.00/SF for renewing tenants Months Vacant: 4 months downtime between leases Tenant Improvements: A $10.00/SF tenant improvement allowance for renewing tenants and $12.00/SF allowance for new tenants occupying previously fitted out space. Leasing Commissions: Initialew leasing commissions are estimated at 4%. Renewing tenants require a 2% leasing commission Reimbursements: Base Year Stop Term Length: 5 Years For offices more than 20,000SF: Renewal Probability: 85% Market Rent: $21.00/SF for new tenants $19.00/SF for renewing tenants Months Vacant: 6 months downtime between leases Tenant Improvements: An $8.00/SF tenant improvement allowance for renewing tenants and S11.00/SF allowance for new tenants occupying previously fitted out space Leasing Commissions: Initialew leasing commissions are estimated at 4% Renewing tenants require a 2% leasing commission Reimbursements: Base Year Stop Term Length: 10 Years Terminal Value The reversion value (expected future sales price) is estimated by capitalizing the year eight net operating income, after adjusting for tenant improvements and leasing commissions. The terminal capitalization rate is expected to be in the 7.5% to 8.5% range. The subject property is in a good location and is one of the better quality office buildings in the area. The property is currently 22 years old. Selling expenses, including commissions and closing costs, are estimated to be 3% of the gross sales and proceeds. This estimate is reasonable considering the size and value of the subject property Discounted Cash Flow Analysis The subject property is a modem office building constructed of very good quality materials and is well maintained. In addition, it is located in close proximity to major roadways. Further, future construction of office buildings is expected to be minimal and new generation buildings are experiencing high occupancies (91%). The subject property is currently below stabilized occupancy because of the unfinished space. Given these considerations, an annual end point property (c.g. unlevered) discount rate of 12.0% is considered appropriate b. A 75% loan/value ratio loan with an 6.5% annual interest rate with monthly interest only payments for five years, one discount point, 2% other financing costs, and a 3% prepayment penalty. The loan begins to amortize after the initial five-year period. The amortization period is 25 years. The market required rate of retum on after debt, before tax equity for 75% L/V ratio loans is 16%. CASE STUDY: WASHINGTON TOWER Property/Analysis Data Washington Tower is a 60,000 SF office building located at 140 Washington Avenue, Houston, TX. The subject property was constructed in 1985. You are to perform a five-year holding period investment analysis of the subject property. The analysis start date is December 1, 2008. The overall rate of inflation is expected to be 3% annually. Reimbursement calculations will be performed on a calendar basis while other revenues and expenses will be inflated on a fiscal basis. Operating expenses are 100% fixed unless noted otherwise. The purchase price of the property is $7.8M. Miscellaneous Revenues In addition to base rent, revenue is derived from roof antennae fees and from parking. Roof antennae fees are expected to be $45,000 for year one and are expected to increase 2.5% per year. The building has 250 parking spaces to rent at $25/month. Projected Recoverable Expenses Real estate taxes are estimated at $1.75 per square foot in year 1. Thereafter, the tax liability is expected to increase at the overall rate of inflation. Insurance coverage includes fires, extended coverage, liability and other space coverage required by this property type. This expense is estimated at $0.18 per square foot initially and is expected to increase at the overall rate of inflation over the expected holding period. Maintenance & Repairs are $1.85 per square foot for year 1 and are expected to increase at the overall rate of inflation during the holding period. These expenses include all interior and exterior maintenance and repairs, contracts pertaining to repairs such as elevator repairs, mechanical equipment, etc. Janitorial expenses are estimated at 895,000 for year 1. These expenses are expected to increase 4% per year. Utilities include electricity, water and sewer. The current cost is $0.95/SF at 100% occupancy. It is estimated that 35% of the first year's utility cost would still be incurred by the property if it were totally vacant. Utility costs are expected to increase at the overall rate of inflation. Roads, Grounds and Security typically includes all salary related items for grounds (including landscaping). maintenance, and security as well as outside contract services. The roads/grounds/security expense is currently 0.45/SF and is expected to increase at the overall rate of inflation over the expected holding period. Projected Non-Recoverable Expenses Management and Administrative Expenses are projected at 4% of effective gross revenue (equal to historical amounts). Analysis of this expense consisted of interviews with representatives of major office building management companies. Capital Expenditures The subject property's roof is partially defective and will need major repairs in October 2010. Current estimates from contractors indicate the expense will total approximately $195,000 in current dollars. This expense is expected to increase 5% per year. Vacancy and Credit Loss To account for vacancy loss, a 7% allowance is applied to the property's potential gross revenue. This allowance will be taken only if the deduction made for vacant periods occurring between leases is less than this amount. The Credit and Collection Loss is expected to be 2% of potential gross income. Rent Roll Suite Tenant SF From To Rent per SF Other terms 100 Around the World 3,750 6/05 5/10 $17.75 Expense Stop of Travel $5.25 per SE 125 Management 1,040 1/04 12/08 $19.50 Expense Stop of Group $5.90 per SF 140 First National Corp 6,200 8/06 7/07 $19.50 Expense Stop of 8/07 7/08 5% increase $6.10 per SF 8/08 7/09 5% increase 8/09 7/10 4% increase 8/10 7/11 4% increase 200 Temp 2 Perm 5.400 9/07 8/10 $21.00 Base year Expense Agency Stop 250 E-Z Credit Union 5,610 7/03 6/09 $12.50 Net Lease Floors Buy a House 23,000 12/06 11/08 $22.00 Expense Stop of 3 & 5 Realtor 12/08 11/10 $23.00 $5.70 per SF 12/10 11/12 $24.00 12/12 11/14 $25.00 25% rental abatement for months 27-38 400 Proposed Tenant 3,000 12/07 11/10 100% of market rent Base Year Expense Stop Notes for Rent Roll: Management Group has notified management that they are vacating at the end of their current lease. Absorption Given the recent leasing of Suite 200, Temp 2 Perm Agency, the property is 75% occupied. Currently, 12,000 SF is unfinished (slab) and vacant. This space is not included in the rent roll. Additionally, another 3,000 SF (already shown on the rent roll) is second-generation space, which is currently vacant. The building has an excellent location and is a very good quality Class B office building. In the analysis of the subject property, an absorption rate of 2,000 SF per quarter is reasonable for the unfinished areas considering the amount and location of the space at the subject property. The unfinished area is available at the beginning of the analysis with absorption projected to begin July 2009. To prepare this currently vacant first generation space for occupancy, a $20.00/SF tenant improvement allowance is assumed. Also, a 5% leasing commission is assigned to each 2,000 SF office. Lease terms will be 5 years and rent will be 100% of current market rent. Market Data Quoted rates and actual recent lease terms at comparable office buildings were analyzed to determine current market rent. The building has two classifications of office space. One is for offices of less than 20,000 SF and the other is for offices of more than 20,000 SF. For offices less than 20,000SF: Renewal Probability 70% Market Rent $23.00/SF for new tenants $20.00/SF for renewing tenants Months Vacant: 4 months downtime between leases Tenant Improvements: A $10.00/SF tenant improvement allowance for renewing tenants and $12.00/SF allowance for new tenants occupying previously fitted out space. Leasing Commissions: Initialew leasing commissions are estimated at 4%. Renewing tenants require a 2% leasing commission Reimbursements: Base Year Stop Term Length: 5 Years For offices more than 20,000SF: Renewal Probability: 85% Market Rent: $21.00/SF for new tenants $19.00/SF for renewing tenants Months Vacant: 6 months downtime between leases Tenant Improvements: An $8.00/SF tenant improvement allowance for renewing tenants and S11.00/SF allowance for new tenants occupying previously fitted out space Leasing Commissions: Initialew leasing commissions are estimated at 4% Renewing tenants require a 2% leasing commission Reimbursements: Base Year Stop Term Length: 10 Years Terminal Value The reversion value (expected future sales price) is estimated by capitalizing the year eight net operating income, after adjusting for tenant improvements and leasing commissions. The terminal capitalization rate is expected to be in the 7.5% to 8.5% range. The subject property is in a good location and is one of the better quality office buildings in the area. The property is currently 22 years old. Selling expenses, including commissions and closing costs, are estimated to be 3% of the gross sales and proceeds. This estimate is reasonable considering the size and value of the subject property Discounted Cash Flow Analysis The subject property is a modem office building constructed of very good quality materials and is well maintained. In addition, it is located in close proximity to major roadways. Further, future construction of office buildings is expected to be minimal and new generation buildings are experiencing high occupancies (91%). The subject property is currently below stabilized occupancy because of the unfinished space. Given these considerations, an annual end point property (c.g. unlevered) discount rate of 12.0% is considered appropriate b. A 75% loan/value ratio loan with an 6.5% annual interest rate with monthly interest only payments for five years, one discount point, 2% other financing costs, and a 3% prepayment penalty. The loan begins to amortize after the initial five-year period. The amortization period is 25 years. The market required rate of retum on after debt, before tax equity for 75% L/V ratio loans is 16%

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts