Question: Cash Flows from Operating Activities - Indirect Method The net income reported on the income statement for the current year was $213,300. Depreciation recorded on

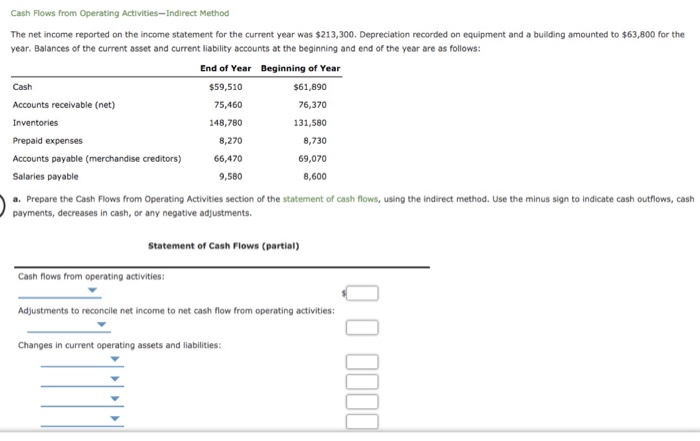

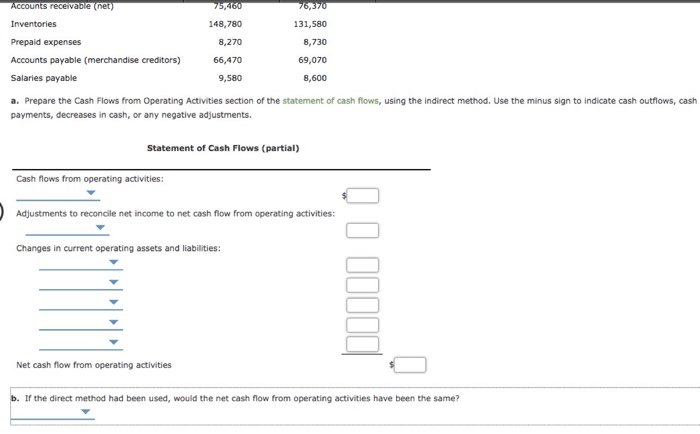

Cash Flows from Operating Activities - Indirect Method The net income reported on the income statement for the current year was $213,300. Depreciation recorded on equipment and a building amounted to $63,800 for the year. Balances of the current asset and current liability accounts at the beginning and end of the year are as follows: End of Year Beginning of Year Cash $59,510 $61,890 Accounts receivable (net) 75,460 76,370 Inventories 148,780 131,580 Prepaid expenses 8,270 8,730 Accounts payable (merchandise creditors) 66,470 69,070 Salaries payable 9,580 8,600 a. Prepare the Cash Flows from Operating Activities section of the statement of cash flows, using the indirect method. Use the minus sign to indicate cash outflows, cash payments, decreases in cash, or any negative adjustments. Statement of Cash Flows (partial) Cash flows from operating activities: Adjustments to reconcile net income to net cash flow from operating activities: Changes in current operating assets and liabilities: [ 1 llll Accounts receivable net) 75,460 76,370 Inventories 148,780 131,580 Prepaid expenses 8,270 8,730 Accounts payable (merchandise creditors) 66,470 69,070 Salaries payable 9,580 8,600 a. Prepare the Cash Flows from Operating Activities section of the statement of cash flows, using the Indirect method. Use the minus sign to indicate cash outflows, cash payments, decreases in cash, or any negative adjustments. Statement of Cash Flows (partial) Cash flows from operating activities: Adjustments to reconcile net income to net cash flow from operating activities: Changes in current operating assets and liabilities: Net cash flow from operating activities b. If the direct method had been used, would the net cash flow from operating activities have been the same

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts