Question: Cash Flows from Operating Activities-Indirect Method Operating Activities Indirect Method The net income reported on the income statement for the current year was $146,300. Depreciation

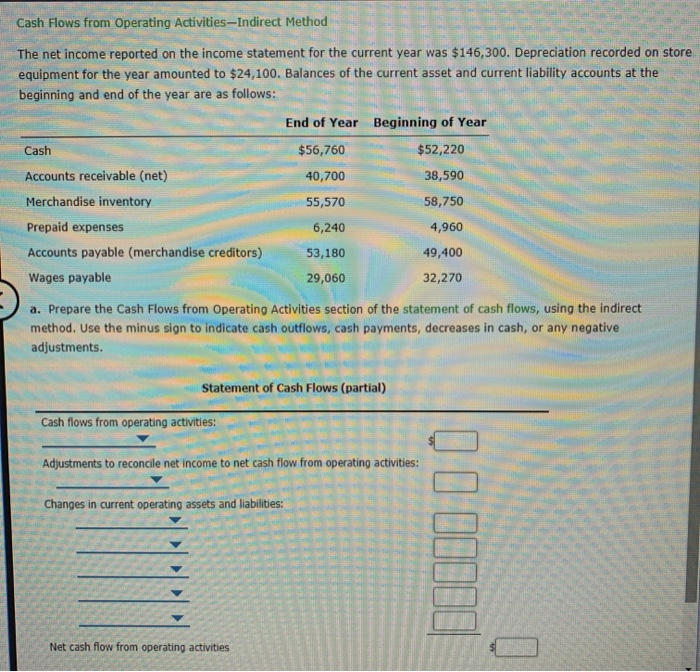

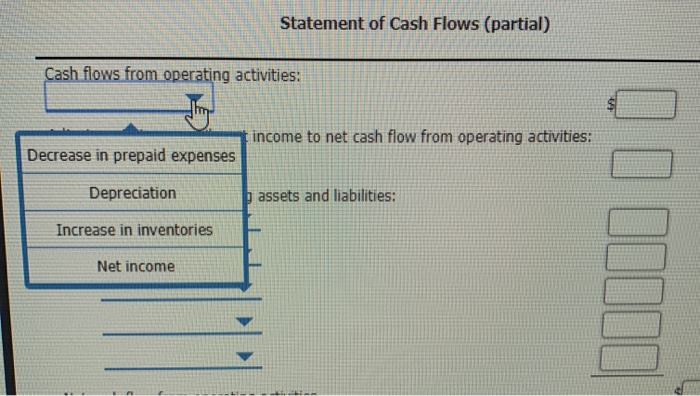

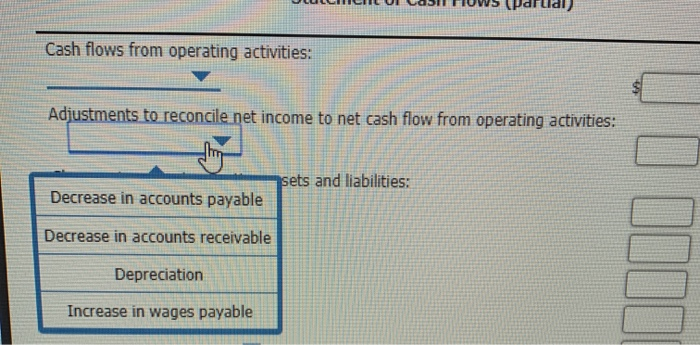

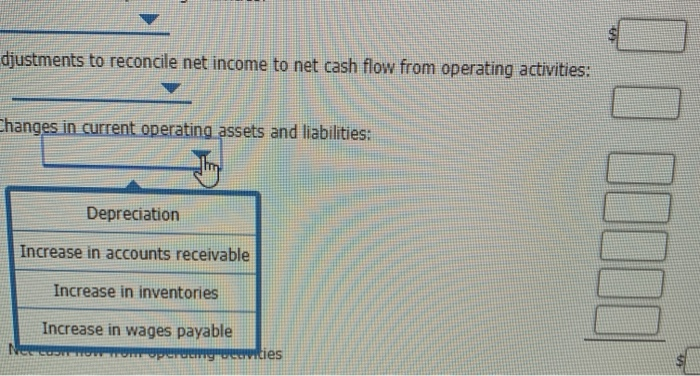

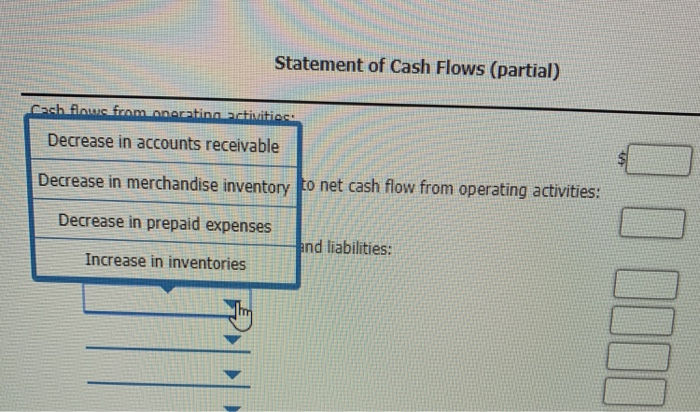

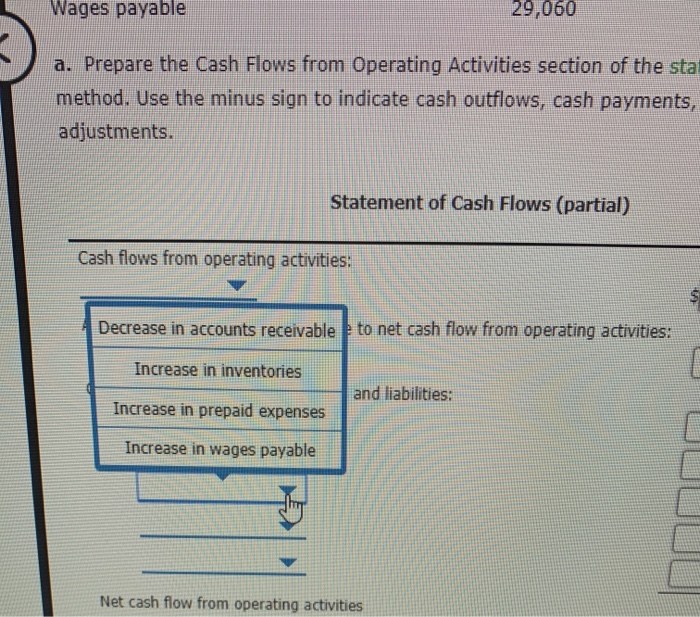

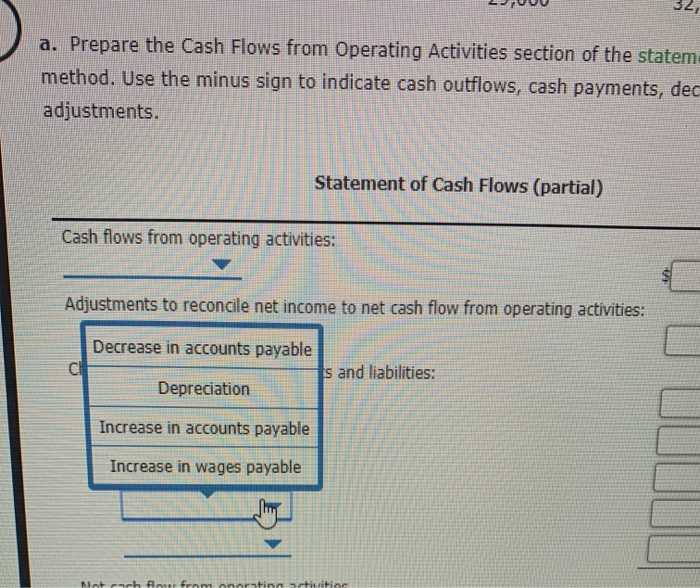

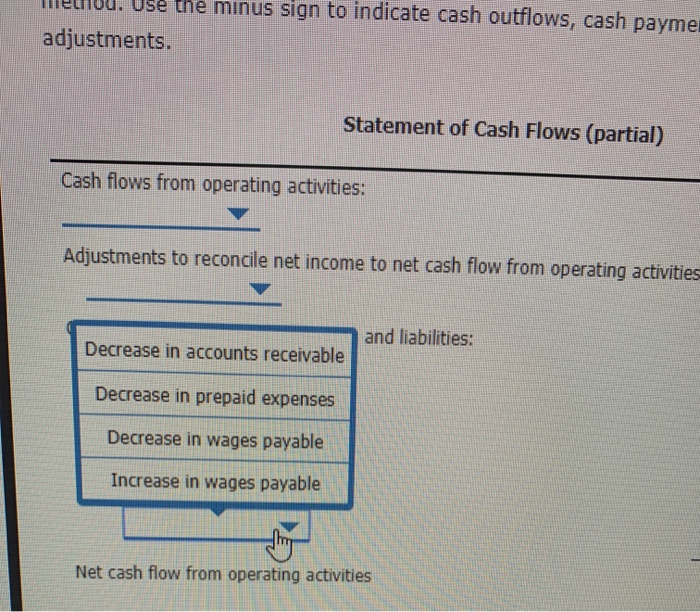

Cash Flows from Operating Activities-Indirect Method Operating Activities Indirect Method The net income reported on the income statement for the current year was $146,300. Depreciation recorded on store equipment for the year amounted to $24,100. Balances of the current asset and current liability accounts at the beginning and end of the year are as follows: End of Year Beginning of Year Cash $56,760 $52,220 Accounts receivable (net) 40,700 38,590 Merchandise inventory 55,570 58,750 6,240 4,960 Prepaid expenses Accounts payable (merchandise creditors) Wages payable 53,180 29,060 49,400 32,270 a. Prepare the Cash Flows from Operating Activities section of the statement of cash flows, using the indirect method. Use the minus sign to indicate cash outflows, cash payments, decreases in cash, or any negative adjustments. Statement of Cash Flows (partial) Cash flows from operating activities: perating activities: Adjustments to reconcile net income to net cash flow from operating activities: 0 Changes in current operating assets and liabilities: RE Net cash flow from operating activities Statement of Cash Flows (partial) Cash flows from operating activities: income to net cash flow from operating activities: Decrease in prepaid expenses Depreciation y assets and liabilities: Increase in inventories Net income IMI I LEILUL LUDILIUS PULUI Cash flows from operating activities: Adjustments to reconcile net income to net cash flow from operating activities: sets and liabilities: Decrease in accounts payable Decrease in accounts receivable Depreciation Increase in wages payable djustments to reconcile net income to net cash flow from operating activities: Changes in current operating assets and liabilities: Depreciation Increase in accounts receivable MI Increase in inventories Increase in wages payable COMOTOperum vicies Statement of Cash Flows (partial) Cash floure from onerating activities: Decrease in accounts receivable Decrease in merchandise inventory to net cash flow from operating activities: Decrease in prepaid expenses and liabilities: Increase in inventories JINN Wages payable 29,060 a. Prepare the Cash Flows from Operating Activities section of the sta method. Use the minus sign to indicate cash outflows, cash payments, adjustments. Statement of Cash Flows (partial) Cash flows from operating activities: Decrease in accounts receivable to net cash flow from operating activities: Increase in inventories | and liabilities: Increase in prepaid expenses Increase in wages payable Net cash flow from operating activities OU 02 a. Prepare the Cash Flows from Operating Activities section of the statem method. Use the minus sign to indicate cash outflows, cash payments, dec adjustments. Statement of Cash Flows (partial) Cash flows from operating activities: Adjustments to reconcile net income to net cash flow from operating activities: Decrease in accounts payable s and liabilities: Depreciation Increase in accounts payable Increase in wages payable Finatiuitiae H UU. Use the minus sign to indicate cash outflows, cash payme adjustments. Statement of Cash Flows (partial) Cash flows from operating activities: Adjustments to reconcile net income to net cash flow from operating activities and liabilities: Decrease in accounts receivable Decrease in prepaid expenses Decrease in wages payable Increase in wages payable Net cash flow from operating activities to net cash flow from operating activities: and liabilities: wities accrual basis cash basis activities differs from net income because it does not use the nues are recorded on the income statement when Net cash flow from operating activities they are earned cash is received b. Cash flows from operating activities differs from net income because it does accounting. For example revenues are recorded on the income statement when

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts