Question: Cemeraldinsight OF Emerald Emerging Markets Case Studies AirAsia Berhad's accounting in the spotlight Siti Seri DelimaAbdul Malak, Wan Nordin B.Wan Hussin, Article information: To cite

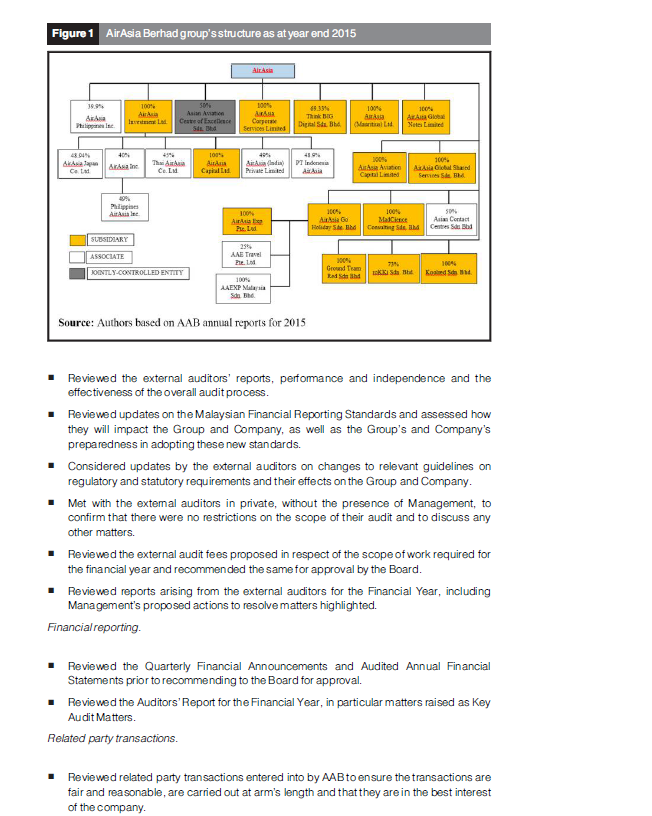

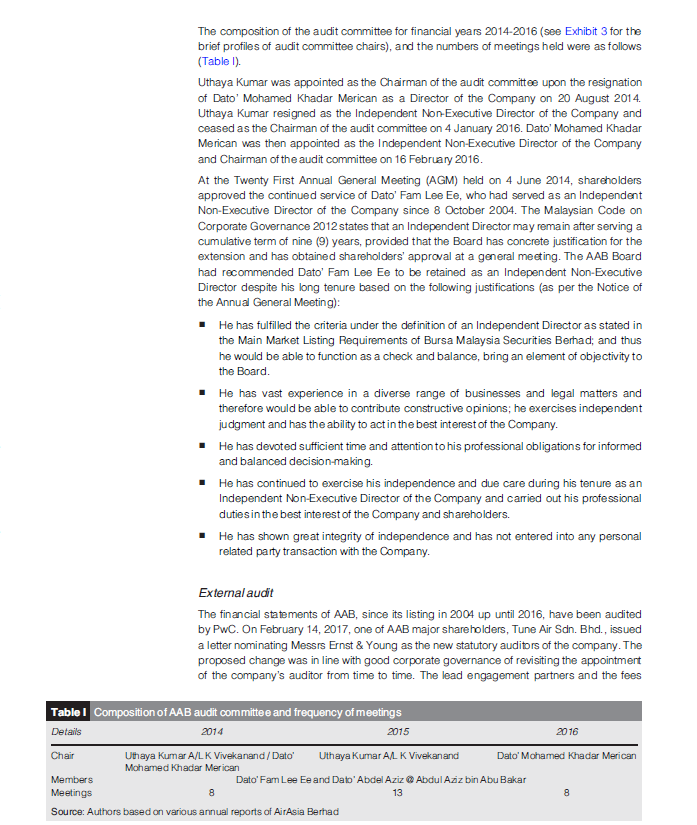

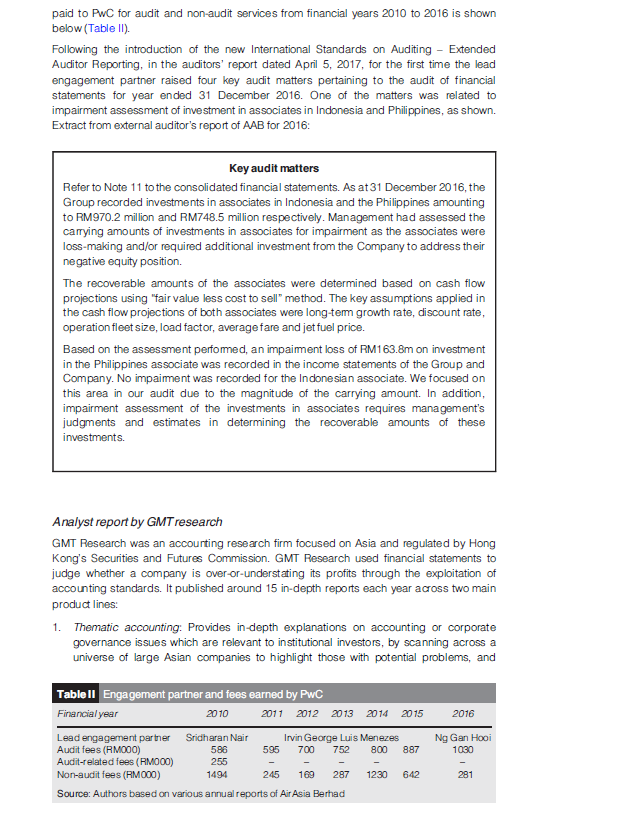

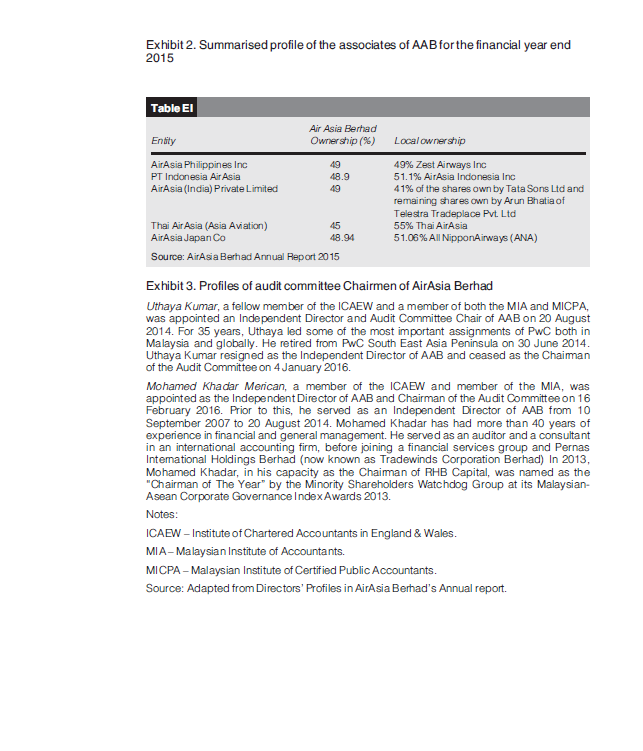

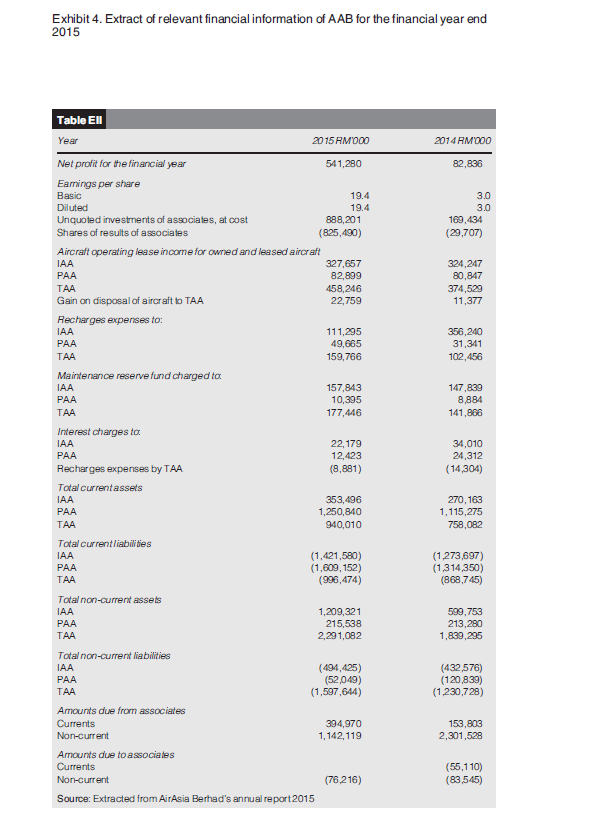

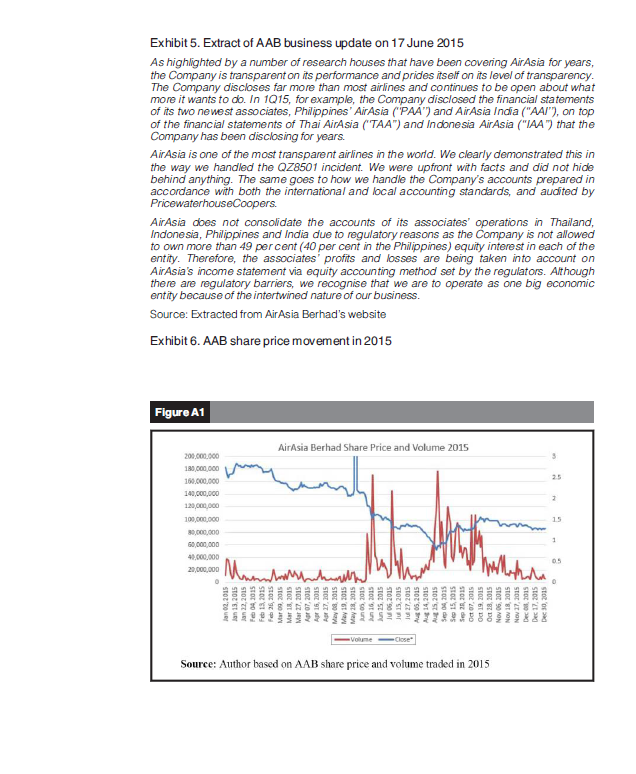

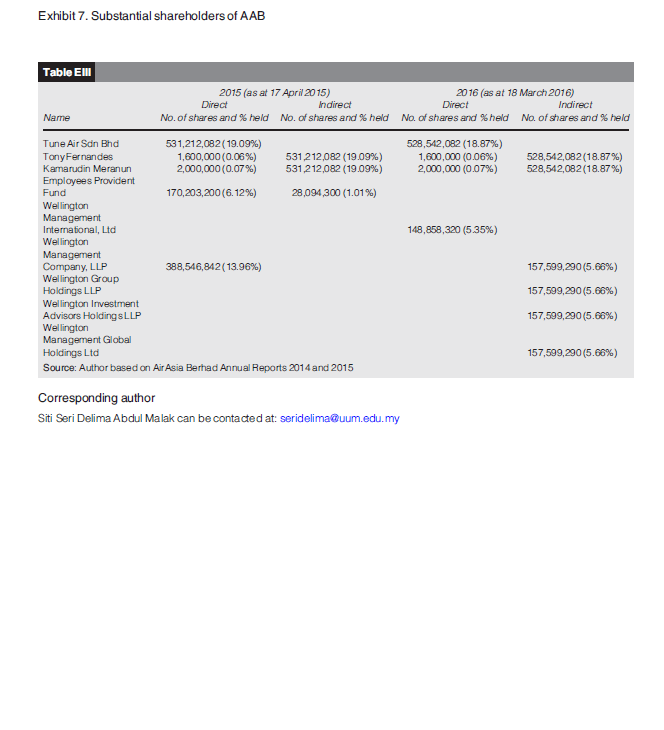

Cemeraldinsight OF Emerald Emerging Markets Case Studies AirAsia Berhad's accounting in the spotlight Siti Seri DelimaAbdul Malak, Wan Nordin B.Wan Hussin, Article information: To cite this document: Siti Seri DelimaAbdul Malak, Wan Nordin B.Wan Hussin, (2019) "AirAsia Berhad's accounting in the spotlight", Emerald Emerging Markets Case Studies, Vol. 9 Issue: 1, pp.1-26, https://doi.org/10.1108/EEMCS-06-2018-0115 Permanent link to this document: https://doi.org/10.1108/EEMCS-06-2018-0115 Downloaded on: 28 June 2019, At: 23:59 (PT) References: this document contains references to 19 other documents. To copy this document: permissions@emeraldinsight.com The fulltext of this document has been downloaded 203 times since 2019* Users who downloaded this article also downloaded: (2018), "Corporate governance failure at Ricoh India: rebuilding lost trust", Emerald Emerging Markets Case Studies, Vol. 8 Iss 4 pp. 1-20 https://doi.org/10.1108/EEMCS-06-2017-0166 (2018),"Responsible investment at Old Mutual: a case of institutional entrepreneurship", Emerald Emerging Markets Case Studies, Vol. 8 Iss 4 pp. 1-29 https://doi.org/10.1108/ EEMCS-02-2018-0025 1866 AUB American University of Beirut Access to this document was granted through an Emerald subscription provided by emerald-srm:365702 For Authors If you would like to write for this, or any other Emerald publication, then please use our Emerald for Authors service information about how to choose which publication to write for and submission guidelines are available for all. Please visit www.emeraldinsight.com/authors for more information. About Emerald www.emeraldinsight.com Emerald is a global publisher linking research and practice to the benefit of society. The company manages a portfolio of more than 290 journals and over 2, 350 books and book series volumes, as well as providing an extensive range of online products and additional customer resources and services. Emerald is both COUNTER 4 and TRANSFER compliant. The organization is a partner of the Committee on Publication Ethics (COPE) and also works with Portico and the LOCKSS initiative for digital archive preservation. *Related content and download information correct at time of download.Associate Companies. Any change in our present relationship with the Associate Companies, be it in equity shareholdings or Shareholders Agreement that gives AAB legal control will result in loss of the Associates' Airline Operating Licenses. PWC has however taken the strict interpretation of power in MERS 10 (Consolidated Financial Statements Accounting Standard) and advised that AAB cannot consolidate its Associate Companies because it does not have legal power" (The Star, 2015a). On June 28, 2015, Financial Times further reported that Tan Sri (Dr) Tony Femandes, the co-founder and Group CEO of AAB, dismissed the negative GMT Research analyst report as rubbish and preposterous, and was confident that at the end of the day, AAB would prove its skeptics wrong (Financial Times, 2015b). Company background AAB was registered in 1993 and began operation in 1996. It was then owned by DRB- Hicom, a Malaysian Goverment-linked company. In 2001, Tony Fernandes of Tune Air Son. Bhd. bought the airline laden with RM40m debts for a token sum of RM1, together with his business partner Datuk Kamarudin Meranun (see Exhibit 1 for the brief profiles on the co-founders). With a tagline of "Now everyone can fly", AAB revolutionised the airline industry. It offered a no-frill and low cost travel across and beyond Asia. Within two years of acquiring AAB, the inherited debt was cleared off. It was listed on Bursa Malaysia in November 2004. AAB has been named the World's Best Low-Cost Airline in the annual World Airline Survey by Skytrax for eight consecutive years from 2009 to 2016 and the World's Leading Low-Cost Airline in the annual World Travel Awards for four consecutive years from 2013 to 2016. Starting from just two ancient Boeing 737-300 aircrafts, by 2017, it had a fleet of over 174 Airbus A320 aircrafts serving over 225 routes and over 109 destinations from 18 countries. Along with its affiliates (Thai AirAsia, Indonesia AirAsia, Philippines AirAsia and AirAsia India), AAB was the largest low-cost carrier in Asia in terms of fleet size and the number of passengers carried[ 1]. Figure 1 illustrates the group structure of AAB before the acquisition of AirAsia Singapore in September 2016. As being publicly listed, AAB treated all their foreign operated airlines companies as associates except for AirAsia (Mauritus) Lid that was deemed a subsidiary. Foreign ownership restrictions prohibited the majority ownership of commerical air transport licenses across much of Southeast Asia (see Exhibit 2 for summary of the associates). AAB required every airlines to sign brand licence agreements that allow for usage of AAB brand, trademarks and logos. The agreements also dictated that airlines had to consult with AAB for their operating decisions and promotional fares. This includes their annual budgets. In addition, airlines also had to pay a brand licensing fee to AAB 1.5 per cent of the consolidated revenue per audited financial statements per fiscal year (Economic Times India, 2016). In 2015, AAB reported that the value of its investment in associates was RM1,020,640,000. The financial reporting ecosytem Audit committee The duties and responsibilities of the audit committee of AAB were set out in its Terms of Reference. The audit committee of AAB was also guided by the AC Charter, approved by the Board. The activities carried out by the audit committee, related to external auditing, financial reporting and related party transactions (as disclosed in the annual report of 2016), include: External audit. Reviewed the external auditors' overall work plan and recommended to the Board the Terms of Engagement.AirAsia Berhad's accounting in the spotlight Siti Seri Delima Abdul Malak and Wan Nordin B. Wan Hussin Introduction Siti Seri Delima Abdul Malak is Doctor atthe It was early April 2017. As a non-professional investor, you had just finished reading through College of Business, the enhanced auditors' report for AirAsia Berhad (AAB) containing the new section on key Univer siti Utara Malaysia, audit matters. One of the critical audit matters raised by the lead engagement partner from Sintok, Kedah, Malaysia. PricewaterhouseCoopers (PWC) caught your attention - the impairment assessment of Wan Nordin B. Wan Hussin investments in associates in Indonesia and the Philippines. is Professor at Othman It brought back the memories of the turbulent events in June 2015, where AAB was Yeop Abdullah Graduate School of Business embroiled in a public relation nightmare that could potentially tamish its corporate Universiti Utara Malaysia, reputation. On June 17, 2015, Financial Times reported that shares in AAB fell almost 7 per Sintok, Malaysia. cent following "investor concern over analysts' reports that have questioned the sustainability of the low-cost carrier's business. The move came as AAB revealed plans to raise convertible bonds for its lossmaking Indonesian and Philippine units, ahead of a proposed stock market listing for each business by 2017 (Financial Times, 2015a). The report also states that "Investors were alarmed after a report by GMT Research, a research firm, alleged on June 10 that AAB used transactions with its affiliate companies to boost earnings. AAB shares on Wednesday closed down 6.7 per cent at RM1.53. The shares have fallen about 25 per cent since the GMT report was published. " To counter the allegations of aggressive accounting practices (including non-consolidation of associates), AAB made the following announcement to Bursa Malaysia on June 17, 2015 (AirAsia Berhad Business Update, 2015): "AAB does not consolidate the accounts of its associates' operations in Thailand, Indonesia, Philippines and India due to regulatory reasons as the Company is not allowed to own more than 49 per cent (40 per cent in the Philippines) equity interest in each of the entity. Therefore, the associates' profits and losses are being taken into account on AAB's income statement via equity accounting method set by the regulators. Although there are regulatory barriers, we recognise that we are to operate as one big economic entity because of the intertwined nature of our business. For the best part of last year having made it known to all, the Company has been trying to get the auditors and regulators to This case study is funded under allow it to consolidate. This has just not been possible but as mentioned before to the a case study grant by Institute for Management and Business investment community, the second quarter will see the Company including a pro forma Research, Universiti Utara consolidation while the Management continues to work with the regulators to allow the Malaysia Company to consolidate". Disclaimer. This case is written solely for educational purposes and is not intended to represent Subsequently, on June 22, 2015, the audit committee of AAB issued a press statement, successfulor unsuccessful addressing the alleged accounting gimmicks. The audit committee reiterated: managerial decision-making. The authors may have "Whilst in practice there is a control in substance, due to aviation regulations in Indonesia, disguised names; financial and other recognizable information Philippines, Thailand and India, AAB cannot have legal control or legal power over its to protect confidentiality.Figure 1 AirAsia Berhad group's structure as at year end 2015 AirAsia 107 Asian Aviation Carperat Think BIG Az.Anta Global SAL EM Services Limited Digital Sia. BbA Canritual Lid Notei Limited 40 100%% Thai Airbain dinaria PT Indorui 100% Co. Lid. Capital Lid. AuAsia Aviation AnAna Global Shaind 100%% 100% AirMain Exp MadCROCE Mian Contact Pic. Led Conairing Sde, BL Centres Bidu Bhi ASSOCIATE AAE Travel Fle. Lol 10044 JOINTLY-CONTROLLED ENTITY Ground Team 100% LAEXP Malaysia Source: Authors based on AAB annual reports for 2015 Reviewed the external auditors' reports, performance and independence and the effectiveness of the overall audit process. Reviewed updates on the Malaysian Financial Reporting Standards and assessed how they will impact the Group and Company, as well as the Group's and Company's preparedness in adopting these new standards. Considered updates by the external auditors on changes to relevant guidelines on regulatory and statutory requirements and their effects on the Group and Company. Met with the external auditors in private, without the presence of Management, to confirm that there were no restrictions on the scope of their audit and to discuss any other matters. Reviewed the external audit fees proposed in respect of the scope of work required for the financial year and recommended the same for approval by the Board. Reviewed reports arising from the external auditors for the Financial Year, including Management's proposed actions to resolve matters highlighted. Financial reporting. Reviewed the Quarterly Financial Announcements and Audited Annual Financial Statements prior to recommending to the Board for approval. Reviewed the Auditors' Report for the Financial Year, in particular matters raised as Key Audit Matters. Related party transactions. Reviewed related party transactions entered into by AAB to ensure the transactions are fair and reasonable, are carried out at arm's length and that they are in the best interest of the company.The composition of the audit committee for financial years 2014-2016 (see Exhibit 3 for the brief profiles of audit committee chairs), and the numbers of meetings held were as follows (Table I). Uthaya Kumar was appointed as the Chairman of the audit committee upon the resignation of Dato' Mohamed Khadar Merican as a Director of the Company on 20 August 2014. Uthaya Kumar resigned as the Independent Non-Executive Director of the Company and ceased as the Chairman of the audit committee on 4 January 2016. Dato' Mohamed Khadar Merican was then appointed as the Independent Non-Executive Director of the Company and Chairman of the audit committee on 16 February 2016. At the Twenty First Annual General Meeting (AGM) held on 4 June 2014, shareholders approved the continued service of Dato' Fam Lee Ee, who had served as an Independent Non-Executive Director of the Company since 8 October 2004. The Malaysian Code on Corporate Governance 2012 states that an Independent Director may remain after serving a cumulative term of nine (9) years, provided that the Board has concrete justification for the extension and has obtained shareholders' approval at a general meeting. The AAB Board had recommended Dato' Fam Lee Ee to be retained as an Independent Non-Executive Director despite his long tenure based on the following justifications (as per the Notice of the Annual General Meeting): He has fulfilled the criteria under the definition of an Independent Director as stated in the Main Market Listing Requirements of Bursa Malaysia Securities Berhad; and thus he would be able to function as a check and balance, bring an element of objectivity to the Board. He has vast experience in a diverse range of businesses and legal matters and therefore would be able to contribute constructive opinions; he exercises independent judgment and has the ability to act in the best interest of the Company. He has devoted sufficient time and attention to his professional obligations for informed and balanced decision-making. He has continued to exercise his independence and due care during his tenure as an Independent Non-Executive Director of the Company and carried out his professional duties in the best interest of the Company and shareholders. He has shown great integrity of independence and has not entered into any personal related party transaction with the Company. External audit The financial statements of AAB, since its listing in 2004 up until 2016, have been audited by PWC. On February 14, 2017, one of AAB major shareholders, Tune Air Sdn. Bhd., issued a letter nominating Messes Ernst & Young as the new statutory auditors of the company. The proposed change was in line with good corporate governance of revisiting the appointment of the company's auditor from time to time. The lead engagement partners and the fees Table I Composition of AAB audit committee and frequency of meetings Details 2014 2015 2016 Chair Uthaya Kumar A/LK Vivekanand / Dato' Uthaya Kumar A/L K Vivekanand Dato' Mohamed Khadar Merican Mohamed Khadar Merican Members Dato' Fam Lee Ee and Dato' Abdel Aziz @ Abdul Aziz bin Abu Bakar Meetings B 13 8 Source: Authors based on various annual reports of AirAsia Barhadpaid to PWC for audit and non-audit services from financial years 2010 to 2016 is shown below (Table II). Following the introduction of the new International Standards on Auditing - Extended Auditor Reporting, in the auditors' report dated April 5, 2017, for the first time the lead engagement partner raised four key audit matters pertaining to the audit of financial statements for year ended 31 December 2016. One of the matters was related to impairment assessment of investment in associates in Indonesia and Philippines, as shown. Extract from external auditor's report of AAB for 2016: Key audit matters Refer to Note 11 to the consolidated financial statements. As at 31 December 2016, the Group recorded investments in associates in Indonesia and the Philippines amounting to RM970.2 million and RM748.5 million respectively. Management had assessed the carrying amounts of investments in associates for impairment as the associates were loss-making and/or required additional investment from the Company to address their negative equity position. The recoverable amounts of the associates were determined based on cash flow projections using "fair value less cost to sell" method. The key assumptions applied in the cash flow projections of both associates were long-term growth rate, discount rate, operation fleet size, load factor, average fare and jet fuel price. Based on the assessment performed, an impairment loss of RM163.8m on investment in the Philippines associate was recorded in the income statements of the Group and Company. No impairment was recorded for the Indonesian associate. We focused on this area in our audit due to the magnitude of the carrying amount. In addition, impairment assessment of the investments in associates requires management's judgments and estimates in determining the recoverable amounts of these investments. Analyst report by GMT research GMT Research was an accounting research firm focused on Asia and regulated by Hong Kong's Securities and Futures Commission. GMT Research used financial statements to judge whether a company is over-or-understating its profits through the exploitation of accounting standards. It published around 15 in-depth reports each year across two main product lines: 1 . Thematic accounting: Provides in-depth explanations on accounting or corporate governance issues which are relevant to institutional investors, by scanning across a universe of large Asian companies to highlight those with potential problems, and Table II Engagement partner and fees earned by PWC Financial year 2010 2011 2012 2013 2014 2015 2016 Lead engagement partner Sridharan Nair Irvin George Luis Menezes Ng Gan Hooi Audit fees (RMOOO) 586 595 700 752 800 8:87 1030 Audit-related fees ( RMOOO) 255 Non-audit fees (RMOOD) 1494 245 109 287 1230 642 281 Source: Authors based on various annual reports of Air Asia Berhadproviding detailed explanations and comment on how these problems might affect the investment argument. 2. Accounting exposes: Highlights companies with particularly egregious accounting where there is significant downside to fair value which is not reflected in the market. Following a request from institutional client-cum-shareholder in AAB to scrutinise its accounting practices, on June 10, 2015, GMT Research issued a "SELL" report that questioned the accounting practices of AAB (GMT Research, 2015): "We estimate that it has managed to inflate profits by 39 per cent over the past five years through related party transactions with associates [. ..] The company is basically creating profits and flattering its operating cash flow by abusing its associates. Real profits have collapsed and Air Asia now needs a recapitalisation that will dilute existing shareholders by more than 100 per cent. We see at least 42 per cent downside with fair value less than RM1.23/share." The report, accused AAB of using transactions with associate companies to inflate earnings, and was widely picked up by the local and international media, and a research institute[2]. KiniBiz reported that "AirAsia generated RM603 million from leasing aircraft to associates and another RM466 million in other income from activities such as selling aircraft to them at a profit in financial year 2014. The around RM1. 1 billion in lease and other income from associates boosted AirAsia profits by 39 per cent" (KiniBiz, 2015b). GMT Research indicated that the value of related party transactions have risen from RM13m in 2004 to RM1.7bn in 2014. As related party transactions grew, the associates' contribution to AAB's operating profit has risen from 22 to 213 per cent over the same period. If it were not for the transfer pricing to related parties, AAB would have been loss-making. GMT Research also claimed that Indonesia AirAsia and AirAsia Philippines of late have not been paying AAB as debts owed by related parties have ballooned from RM170m at end-2007, to RM2.8bn by end-1015, with the amounts owed outstripping the sales those associates generate. It is not just the amounts owed by those affiliates that were a concern for GMT Research, as AAB had also been extending money for working capital to its associates in Indonesia and the Philippines. In 2014, that amount was RM1.1 billion and a further RM323m was extended in the first quarter of 2015. Troubles in its associates, according to GMT Research, has now dragged operating cash flows of AAB by 46 per cent to RM1.3bn, which was not helped by AAB's spending on capital expenditure which was close to a record high. With the amount owed by associates such as Indonesia AirAsia and AirAsia Philippines growing and reached 60 per cent of shareholders' funds, a non-payment of that debt and a write-down would have an adverse impact on the financials of AAB. Financial reporting standards on consolidation Up until 31 December 2016, the foreign associates and related intercompany transactions were recorded and recognised by AAB using equity method as per IAS 28. The audit commitee of AAB defended this accounting policy choice by stating "So whilst we are of the view that consolidation would present a true and fair view of AAB's relationships with its Associate companies, we have been advised to do so would be a breach of MFRS 10 and in addition the "true and fair' override would also not be allowed." To understand AAB's accounting policy choice, you gathered some information by revisiting the history behind the introduction of IFRS 10 into the accounting standards. The creation of "off balance sheet" special purpose entities (SPEs) was partially blamed for the financial crisis in 2007. Shareholders were exposed to additional risks from these special vehicles. Companies claimed they did not control these SPEs because they did not have majority ownership. The inconsistencies between the concept of control in the IAS 27 (2008)"Consolidated Financial Statements and Accounting for Investments in Subsidiaries" and SIC 12 "Consolidation - Special Purpose Entities" were used for non-consolidation of these entities[3]. IASB was then asked by the G20 leaders, the Financial Stability Board and others to review this practice. In 2011, the IFRS 10 "Consolidated Financial Statements" was introduced and it replaced IAS 27 (2008) and SIC 12. The new IFRS 10 developed a single control model that can be applied to all entities. The new control model moved away from merely looking at absolute control (usually from holding majority share ownership) to effective control. It defined control as "when the investor is exposed, or has rights, to variable returns from its involvement with the investee and has the ability to affect those returns through its power over the investee"[4]. An investor need to satisfy all these three elements for control to occur. Share ownership was no longer the single determining factor of control. In effect, the IFRS required the application of 'substance over form' in applying this new control model[ 5]. In the presence of control, companies have to recognise the investee as subsidiary and to consolidate[6]. All intercompany transactions including gains and losses are eliminated. This will avoid double counting of the resources and obligations of the companies. In effect, the companies within the group are recognised as a single reporting entity. Investee that is not controlled will fall under the categories of associates, joint arrangements, share investments or "available for sale" investments. For an associate, under the equity method as prescribed by IAS 28 "Investments in Associates and Joint Ventures," the investor will only recognize the share of profit or loss from its associate into the carrying amount[7]. An investor controls an investee when the investor is exposed, or has rights, to variable returns from its involvement with the investee and has the ability to affect those retums through its power over the investee. Intercompany transactions with associate companies AAB had a number of contracts with its airline associates that covered leasing, maintenance and repair, merchandise, booking, inflight entertainment, insurance and others. Associates did not lease planes directly from third parties; instead AAB leased the planes on their behalf (through AirAsia Aviation Capital Limited). They were then subleased to the associates at higher prices. In 2015, AAB charged RM68,770,000 to its associates for fees for commercial air transport services. Airlines associates were also subjected to profit sharing terms in accordance to the license agreement. The terms dictate the business units' revenue management, catering, flight operations, marketing, finance, branding, ancillary revenue and organizational structure (Live Mint, 2016). In 2015, the reported current amount due from associates was RM394,970,000 and long- term overdue from associates was RM1, 142,119. These figures were reported as assets of AAB. A significant portion of these amount due came from Indonesia AirAsia and AirAsia Philippines that were suffering from extensive losses. An impairment loss for associates of RM876,000,000 was eventually recognized in 2015 and RM163,750,000 the following year in the income statement of AAB (see Exhibit 4 for extract of financial statements of AAB). Reactions to GMT research's analyst report AirAsia group A few days after the release of GMT Research's analyst report, on June 15, Tony sent a personal letter addressed to AAB investors. In the letter he wrote that "We believe that 2015 will be a very good year on the back of a better operating environment and a much more rational market. We have shown you good progress in 1015 [.. .] We believe in results, not words." The letter also addressed the turnaround plans for Indonesia AirAsia and AirAsia Philippines[8].Subsequently, on June 17, 2015, AAB issued a four-page business update, which appeared in the Bursa Malaysia website (Exhibit 5). It stressed upon its transparency in reporting all its accounts including its associates and leasing business. All was done in accordance to the accounting standards and audited by PWC. AAB also disclosed that they had been trying to consolidate all its entities but regulatory barrier and auditor's resistance had impeded the process. It had also set a target of producing a pro forma consolidation report starting from the second quarter of 2015. However, the Securities Commission opposed the idea of issuing another AAB financial report given that it may confuse the shareholders (KiniBiz, 2015a). Thus, in the unaudited consolidated financial statements for the year ended December 31, 2015, Thai AirAsia, Indonesia AirAsia, AirAsia Philippines, AirAsia India and AirAsia Japan were still equity accounted as associates[9]. AAB rebutted the claim of overcharging on the leasing of aircrafts to its associates stating that it was comparable to other third party commercial lessors. The business update also included its plan for Indonesia AirAsia and AirAsia Philippines that owed AAB substantial intercompany transactions. Both planned to raise fund via new equity offers, with the proceeds to be partially used to pay for the amount due. AAB expected a cash repayment of RM1 bn from these two associates. At the sidelines, Tony also rubbished those assertions by GMT Research. Tony in a Financial Times interview (Financial Times, 2015b) was quoted as saying "This [GMT] report is rubbish. We're doing extremely well. Frankly I've been disappointed with the equity market. They've known us for 14 years and there's nothing in that report that hasn't been disclosed already. It's preposterous to suggest that there's any intention to hide. The fact that we're so transparent allowed them to write that report. We declared far more than we needed to." At the Paris Airshow, he responded to concerns on the feasibility of the public offerings on the loss making associates by saying "We have so many cash-raising opportunities from our fleet, our investments, from our national cash operations, there is no need for a capital raise. We don't want to do too many because we don't need that much cash. But it's just to show the market that it can be done and crystallize the value" (Reuters, 2015b). His bullish sentiment was probably triggered by the fact that AAB won the World's and Asia's Best Low Cost Airline at the Skytrax World's Airline Awards held during the air show. Meanwhile, the audit committee of AAB gave the following explanations to counter the alleged accounting malpractices by abusing its associates: "AAB (The Board, Audit Committee and management) are of a clear opinion that it should consolidate its Associate companies. It has for at least over 12 months, had a whole series of meetings with PWC, legal advisers, management of the Associate companies and aviation regulators to effect consolidation of its Associate companies. These meetings were not mere discussions but supported by board papers and opinions from our Auditors and legal advisers from the territories in which the Associate Companies operate. AAB has expressed a clear view to PWC that it is exposed to or has rights to variable retums from its involvement with its Associate companies. In fact it is involved to the extent that AAB does affect the returns over its Associate companies. AAB believes this is a critical criteria and the "raison" for consolidation of Associate companies. It should therefore be allowed to consolidate its Associate companies as it does reflect the actual performance and financial position of AAB. Power in practice is however not legal control. Whilst in practice there is control in substance, due to aviation regulations in Indonesia, Philippine, Thailand and India, AAB cannot have legal control or legal power over its Associate companies. Any change in our present relationship with the Associate companies, be it in equity shareholdings or Shareholders Agreement, that gives AAB legal control will result in loss of the Associates' Airline Operating Licenses [.. .] PWC advised that AAB cannot consolidate its Associates Companies because it does not have legal power. Their view is power in substance is insufficient to meet the criteria forconsolidation, as such substantive power can be withdrawn at anytime by the Associate companies (The Star, 2015a)." Institutional investors and minority shareholder watchdog group Exhibit 6 presents the movements in AAB share price in 2015. The share price nosedived immediately following the release of the analyst reports questioning the accounting methods used by AAB in June 2015. AAB stock fell to MYR1.73 on June 12, 2015, a five- year low, and continued to tumble to an all-time low of below MYRO.80 by end August 2015. However, since September 2015, it recovered gradually, reaching RM3. 20 in August 2016 The two largest institutional investors, Wellington Management Company, LLP and Employees Provident Fund had gradually reduced its shareholding in AAB during 2015-2016 (Exhibit 7). The Minority Shareholder Watchdog Group made the following comments in relation to the questionable accounting (Minority Shareholder Watchdog Group, The Observer, 2015): "The non-consolidation of its associates' account is in compliance with the requirements of MERS 10 and the regulatory requirements of operating countries [...] As to Indonesia AirAsia (IAA) and AirAsia Inc. (Philippines AirAsia) advances of about RM900 million at around 6 per cent interest given to them, questions would arise on whether these associates would be able to service these debts, considering that they are in the "red" in the light of tougher operating conditions in Philippines and Indonesia". Other analysts On June 15, a local research house CIMB Research gave an "ADD" stock recommendation. The analyst Raymond Yap predicted a target price of RM226, "based on the belief that Air Asia will be able to avoid a punishing rights issue by successfully bringing new investors into Indonesia Air Asia and AirAsia Philippines and obtaining an RM Ibn repayment of the associate balances owed to it. This is on top of securing the sale and leaseback of 16 older planes for total proceeds of US$384m (RM1,440m); eight deals have already been concluded [10]. CIMB Research had a different view on the accounting practices of AAB. While AAB detractors accused AAB of "exploiting the associates with high leasing and other operating charges in order to benefit the mainline carrier", according to CIMB "Air Asia's disclosure is first-class and is better than SIA's. Air Asia has never hidden the fact that Air Asia charges a variety of fees to the associates. These fees are disclosed in the financial statements and profits on them can be estimated." On June 16, 2015, another local research house, Alliance DBS Research, also highlighted several concems about the group's eamings quality. The analyst Tan Kee Hoong gave a "HOLD" stock rating with a 12-month target price of RM1.80, and issued the following statements: "First, Air Asia's depreciation policies seem aggressive vis-a-vis its peers. It assumes 25 years useful life and 10 per cent residual value for its aircraft, which implies an annual depreciation rate of 3.6 per cent vs. peers' range of 4.5-6.3 per cent. This distorts earnings quality, and could lead to future losses when the aircraft are eventually disposed. Recognition of interest income on amounts due from associates & JVs, which made up 22 per cent of core net profit in 1015, has helped Air Asia to prop up bottom-line. But this does not reflect economic reality and distorts earnings quality, given it could be challenging to collect the dues from Indonesia Air Asia and Philippines Air Asia. Also, this income stream is not sustainable going forward when the underlying dues are reduced via partial pay-out and a debt-equity swap. What these distortions means? After adjusting for the above distortions, our calculations suggest net profit would be 30-35 per cent lower than our current core net profit forecasts for FY15-17 (which is premised on Air Asia's current accounting policies)'[ 1 1].The way forward On May 9, 2016, after the AAB general meeting, Tony Fernandes was quoted "This has always been my plan to consolidate but we have to talk to many different authorities to do so. There is no timeframe yet at the moment. If you compare us with easylet or Ryanair, Keywords: they don't have an easyJet Poland. They just have one entity. Because of ownership rules Corporate governance, we have to have that kind of structure that we have today" (The Star Online, 2016). Accountability, Accounting/accountancy, A year after the last AGM held in May 2016, as a non-professional investor in AAB, you were Accounting standards, concerned about the alleged aggressive accounting in relation to the foreign associates Auditing and wondered how you should raise your concern with the management, audit committee Audit committees/culture and external auditor during the incoming AGM scheduled next month. Notes 1. AirAsia Berhad website visited on April 23, 2018. 2. See for examples; Reuters (2015a), Barron's (2015), The Business Times Singapore (2015a, 2015b), The Star (2015b), KiniBiz (2015a), The Malaysian Reserve (2015) and NUS Risk Management Institute (2015) 3. IFRS 10 Consolidated Financial Statements, IN (Interpretation) 1. 4. IFRS 10 Consolidated Financial Statements, Para 7. 5. In Malaysia, the IFRS is adopted in total and directly translated into Malaysian Financial Reporting Standards ( MFRSs). 6. IFRS 10 Consolidated Financial Statements, Para 4. 7. Refer to interaction between IFRSs 7, 9, 10, 11 and 12 and IAS 28 by IFRS Foundation. 8. Extract of the letters available from the news article by Reuters (June 14,2015) Exclusive AirAsia CEO Tells Investors Plans Up to 300 million Bonds Jet Sales as Shares Skid, available at: www.reuters. com/article/us-air asia- accounts/exclusive-airasia-ceo-tells-investors-plans-up-to-300-million-bonds- jet-sales-as-share id-idUSKBNOOVO3W201 506 15. 9. Example of statement in the unaudited consolidated report on the accounting policy choices for its foreign entities "Indonesia AirAsia is an associate company Indonesia AirAsia is an associate company owned 49 per cent by Air Asia Berhad. As such it is accounted for using the equity method, as permitted by the Malaysian Accounting Standards Board MFRS128, Investments in Associates owned 49 per cent by AirAsia Berhad. As such it is accounted for using the equity method, as permitted by the Malaysian Accounting Standards Board MFRS128, Investments in Associates". 10. CIMB Research (June 15, 2015)-Solutions' announced, relief rally? 11. Alliance DBS Research, June 16, 2015-Weak earnings quality. References AirAsia Berhad Business Update (2015), available at: https:/ir.airasia.comewsroom/AAB_Statement_ ( Final).pdf Barron's (2015), AirAsia under Pressure as Accounting Questioned, Barron's. Economic Times India (2016), "AirAsia executives alerted board tatas about lapses in business practices", available at: https://economictimes.indiatimes.com/industry/transportation/airlines-/- aviation/airasia-executives-alerted-board-tatas-about-lapses-in-business-practices/articleshow/ 55281027.cms Financial Times (2015a), "Air Asia shares fall on questions about accounting and cash flow", available at: www.ft.com/content/31360c22-14ba-11e5-851f-00144feabdc0 Financial Times (2015b), "AirAsia CEO pledges to prove air line's critics wrong", available at: www.ft.com/ content/423828ce-184c-1 1e5-8130-2e7db721/996 GMT Research (2015), Sell: New Dog, Old Tricks, GMT Research.KiniBiz (2015a), "Did AirAsia engage in accounting shenanigans", available at www.kinibiz.com/story/ issues/174872/did-airasia-engage-in-accounting-shenanigans.html KiniBiz (2015b), "Is AirAsia in trouble?", available at: www.kinbiz com/story/issues/175110/is-airasia-in- trouble.html LiveMint (2016), "Who really runs AirAsia India", available at: www.livemint.com/Companies/ dXN7 jGDvloYOx2jQWf139L/Who-really-runs-AirAsia-India.htm Minority Shareholder Watchdog Group, The Observer (2015), available at www.mswg.org.my/sites/ default/files/26.06.2015.pdf NUS Risk Management Institute (2015), "Murky financial transactions tarnish the credit outlook for AirAsia", available at: www.mmicri.org/media/static/images/thumbnail-pdf/WCBJUN16JUN2220 15.pdf Reuters (2015a), "GMT research report questions Air Asia accounting practices", available at: www. reuters. com/article/20 15/06/1 2/malaysia-air asia-accounts-idUSL3NOVY32X20150612 Reuters (2015b), "Air Asia shares tumble as CEO fund-raising talk cuts no ice", available at: www. reuters.com/article/airasia-stocks/update-3-airasia-shares-tumble-as-ceo-fund-raising-talk-cuts- no-ice-idUSL 3NOZ 31G4201506 17 The Business Times Singapore (2015a), "AirAsia falls further amid fresh accounting-method concerns", available at: www.businesstimes. com.sg/transportairasia-falls-further-amid-fresh-accounting-method-concerns The Business Times Singapore (2015b), "AirAsia audit committee clarifies non-consolidation of associates", available at www.businesstimes. com.sg/companies-markets/airasia-audit-committee- clarifies-non-consolidation-of-associates The Malaysian Reserve (2015), "Someone stole our AirAsia report, says GMT research", available at: https://themalaysianreserve. com/2017/03/31/someone-stole-our-airasia-report-says-gmt-research The Star (2015a), "AirAsia audit committee issues statement over GMT research report", available at: www.thestar.com.my/business/business-news/2015/06/22/airasia-audit-committee-issues- statement-over-gmt-research-report The Star (2015b), "AirAsia seeks to consolidate associates' accounts, upbeat on Indonesia, Philippines" available at www.thestar.com.my/business/business-news/2015/06/17/airasia-seeks-to-consolidate- associates-account-upbeat-on-indonesia-philippines The Star Online (2016), "Tony lobbies for single ownership of business units", available at: www.thestar. com.my/business/business-news/2016/05/10/tony-bbbies-for-consolidation Exhibit 1. Profiles of co-founders of AirAsia Berhad Tony Fernandes co-founded Tune Air Son. Bhd., the major shareholder of AAB, in 2001. Tony has been the Group CEO of AAB since December 2001. Prior to AAB, he was the Financial Controller of Virgin Communications London before joining Wamer Music International London in 1989. He was promoted to Managing Director, Warner Music Malaysia in 1992 and to Regional Managing Director, Warner Music South East Asia in 1996. In 1999, he became the Vice President of Wamer Music South East Asia. He graduated with a Bachelor Degree in Accounting from the London School of Economics in 1987, and admitted as an Associate Member of the ACCAin 1991. Kamarudin Meranum, a co-founder of Tune Air Sdn. Bhd, has been the Executive Chairman of AAB since November 6, 2013. On 13 January 2012, Kamarudin was re-designated from Group Deputy CEO (a position he held since December 2005) to Deputy Group CEO & President of Group Finance, Treasury, Corporate Finance and Legal. In January 2004, he was appointed Executive Director of the company after three years being in the role of Director, of which he was appointed on 12 December 2001. Prior to AAB, he served at Arab-Malaysian Merchant Bank as a Portfolio Manager from 1988 to 1993, managed both institutional and high net-worth individual clients' investment funds. Note: ACCA-Association of Chartered Certified Accountants. Source: Adapted from Directors' Profiles in AirAsia Berhad's Annual report.Exhibit 2. Summarised profile of the associates of AAB for the financial year end 2015 Table EI Air Asia Berhad Entity Ownership (%) Local ownership AirAsia Philippines Inc 19 19% Zest Airways Inc PT Indonesia Air Asia 48.9 51.1% AirAsia Indonesia Inc AirAsia (India) Private Limited 49 41% of the shares own by Tata Sons Lid and remaining shares own by Arun Bhatia of Telestra Tradeplace Put. Ltd Thai Air Asia (Asia Aviation) 45 55% Thai AirAsia AirAsia Japan Co 48.94 51.06% All NipponAirways (ANA) Source: AirAsia Berhad Annual Report 20 15 Exhibit 3. Profiles of audit committee Chairmen of AirAsia Berhad Uthaya Kumar, a fellow member of the ICAEW and a member of both the MIA and MICPA, was appointed an Independent Director and Audit Committee Chair of AAB on 20 August 2014. For 35 years, Uthaya led some of the most important assignments of PWC both in Malaysia and globally. He retired from PWC South East Asia Peninsula on 30 June 2014. Uthaya Kumar resigned as the Independent Director of AAB and ceased as the Chairman of the Audit Committee on 4 January 2016. Mohamed Khadar Merican, a member of the ICAEW and member of the MIA, was appointed as the Independent Director of AAB and Chairman of the Audit Committee on 16 February 2016. Prior to this, he served as an Independent Director of AAB from 10 September 2007 to 20 August 2014. Mohamed Khadar has had more than 40 years of experience in financial and general management. He served as an auditor and a consultant in an international accounting firm, before joining a financial services group and Pernas International Holdings Berhad (now known as Tradewinds Corporation Berhad) In 2013, Mohamed Khadar, in his capacity as the Chairman of RHB Capital, was named as the 'Chairman of The Year" by the Minority Shareholders Watchdog Group at its Malaysian- Asean Corporate Governance Index Awards 2013. Notes: ICAEW - Institute of Chartered Accountants in England & Wales. MIA- Malaysian Institute of Accountants. MICPA - Malaysian Institute of Certified Public Accountants. Source: Adapted from Directors' Profiles in AirAsia Berhad's Annual report.Exhibit 4. Extract of relevant financial information of AAB for the financial year end 2015 Tablo Ell Year 20 15 RM'D00 2014 RM'000 Net profit for the financial year 541,280 82,836 Eamings per share Basic 19.4 3.0 Diluted 19.4 30 Unquoted investments of associates, at cost 888,201 109, 434 Shares of results of associates (825, 490) (29,707) Aircraft operating lease income for owned and leased aircraft IAA 327,657 324,247 PAA 82,899 80, 847 TAA 458,246 374,529 Gain on disposal of aircraft to TAA 22,759 11,377 Recharges expenses to: IAA 11 1,295 356,240 PAA 49,665 31,341 TAA 159,766 102,456 Maintenance reserve fund charged to. IAA 157,843 147,839 PAA 10,395 8,884 TAA 177,446 141,806 Interest charges to. IAA 22,179 34,010 PAA 12,423 24,312 Recharges expenses by TAA (8,881) (14,304) Total current assets IAA 353,196 270, 163 PAA 1,250,840 1, 115,275 TAA 940,010 758, 082 Total currentliabilities IAA (1,421,580) (1,273,697) PAA (1,609, 152) (1,314,350) TAA (996, 474) (868,745) Total non-current assets IAA 1,209,321 599, 753 PAA 215,538 213,280 TAA 2,291,082 1,839,295 Total non-current liabilities IAA (494, 425) (432,576) PAA (52,049) (120,839) TAA (1,597 ,644) (1,230,728) Amounts due from associates Currents 394,970 153,803 Non-current 1, 142, 119 2,301,528 Amounts due to associates Currents (55,1 10) Non-current (76,216) (83,545) Source: Extracted from AirAsia Berhad's annual report 2015Exhibit 5. Extract of AAB business update on 17 June 2015 As highlighted by a number of research houses that have been covering AirAsia for years, the Company is transparent on its performance and prides itself on its level of transparency. The Company discloses far more than most airlines and continues to be open about what more it wants to do. In 1015, for example, the Company disclosed the financial statements of its two newest associates, Philippines' AirAsia ("PAA") and AirAsia India ("AAI"), on top of the financial statements of Thai AirAsia ("TAA") and Indonesia AirAsia ("IAA ") that the Company has been disclosing for years. AirAsia is one of the most transparent airlines in the world. We clearly demonstrated this in the way we handled the QZ8501 incident. We were upfront with facts and did not hide behind anything. The same goes to how we handle the Company's accounts prepared in accordance with both the international and local accounting standards, and audited by PricewaterhouseCoopers. AirAsia does not consolidate the accounts of its associates' operations in Thailand, Indonesia, Philippines and India due to regulatory reasons as the Company is not allowed to own more than 49 percent (40 per cent in the Philippines) equity interest in each of the entity. Therefore, the associates' profits and losses are being taken into account on AirAsia's income statement via equity accounting method set by the regulators. Although there are regulatory barriers, we recognise that we are to operate as one big economic entity because of the intertwined nature of our business. Source: Extracted from AirAsia Berhad's website Exhibit 6. AAB share price movement in 2015 Figure A1 AirAsia Berhad Share Price and Volume 2015 204.003.800 180,601,060 154.600.800 35 140,000,000 126,010,060 100,000,090 15 19,000.000 60,000,000 44.003.000 t 26, 2015 Feb 04 10 15 Jan 25, 2015 Jul 96,2015 Jul 27,2015 Jui 15,2015 Feta 15, 2015 Aug 05,2015 Jan 16, 2015 Ja 05, 2015 Sep 15, 2015 Aug 25,2015 Sep 28, 3025 Jan 12,2015 Apr 16, 2015 Apr 07, 2015 Oct 28, 2015 Oct 07. 2015 Nov 06, 2015 Apr 17, 2015 Aug 14,2015 Mar 09, 2015 Nov 18, 2015 Mar 18, 2015 May 28, 2015 Oct 19, 2015 Dec 17, 2015 Mar 27, 2015 Dec oil. 3015 May ba, 2015 May 15, 2015 Dec 30, 2015 Nov 17, 2015 Jan 13, 2015 Jan 62,2015 -Volume Close" Source: Author based on AAB share price and volume traded in 2015Exhibit 7. Substantial shareholders of AAB Tablo EllI 2015 (as at 17 April 2015) 2016 (as at 18 March 2016) Direct Indirect Direct Indirect Name No. of shares and % held No. of shares and % held No. of shares and % held No. of shares and % held Tune Air Son Bhd 531,212,082 (19.09%) 528,512,082 (18.87%) Tony Fernandes 1,600,000 (0.06%) 531,212,082 (19.09%) 1,600,000 (0.06%) 528,512,082 (18.87%) Kamarudin Meranun 2,000,000 (0.07%) 531,212,082 (19.09%) 2,000,000 (0.07%) 528,542,082 (18.87%) Employees Provident Fund 170,203,200 (6.12%) 28,094,300 (1.01%) Wellington Management International, Lid 148,858,320 (5.35%) Wellington Management Company, LLP 388,546,842 (13.96%) 157,599,290 (5.60%) Wellington Group Holdings LLP 157,599,290 (5.60%) Wellington Investment Advisors Holding s LLP 157,599,200 (5.60%) Wellington Management Global Holdings Lid 157,599,290 (5.06%) Source: Author based on Air Asia Berhad Annual Reports 2014 and 2015 Corresponding author Siti Seri Delima Abdul Malak can be contacted at: seridelima@uum.edu.my

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock

Students Have Also Explored These Related Accounting Questions!