Question: Chapter 1: Concepts/definitions: - When do you use the equity method? - When do you use the cost or fair value method? - When do

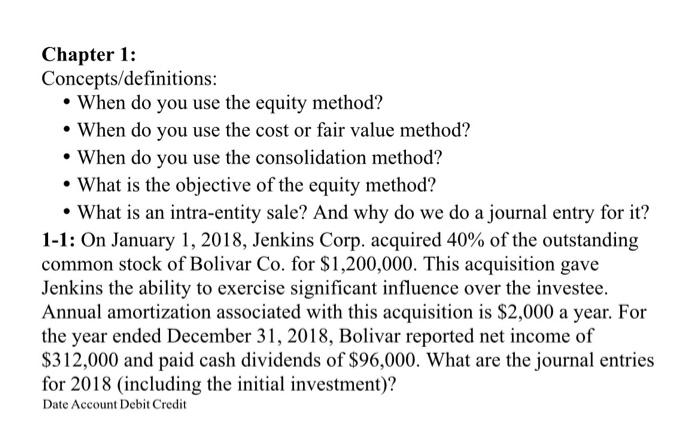

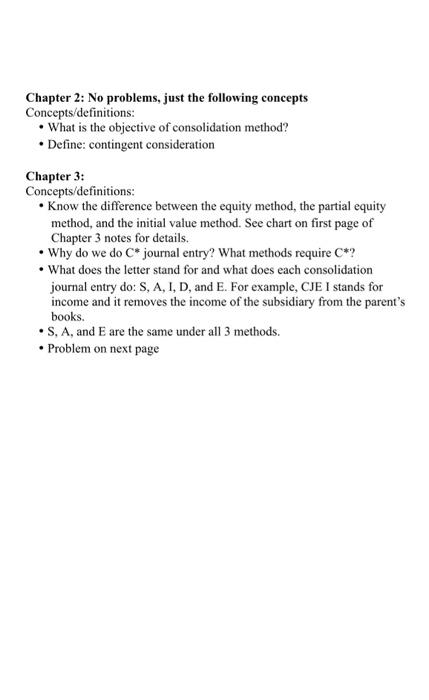

Chapter 1: Concepts/definitions: - When do you use the equity method? - When do you use the cost or fair value method? - When do you use the consolidation method? - What is the objective of the equity method? - What is an intra-entity sale? And why do we do a journal entry for it? 1-1: On January 1, 2018, Jenkins Corp. acquired 40% of the outstanding common stock of Bolivar Co. for $1,200,000. This acquisition gave Jenkins the ability to exercise significant influence over the investee. Annual amortization associated with this acquisition is $2,000 a year. For the year ended December 31,2018, Bolivar reported net income of $312,000 and paid cash dividends of $96,000. What are the journal entries for 2018 (including the initial investment)? Date Account Debit Credit Chapter 2: No problems, just the following concepts Concepts/definitions: - What is the objective of consolidation method? - Define: contingent consideration Chapter 3: Concepts/definitions: - Know the difference between the equity method, the partial equity method, and the initial value method. See chart on first page of Chapter 3 notes for details. - Why do we do C journal entry? What methods require C ? - What does the letter stand for and what does each consolidation journal entry do: S, A, I, D, and E. For example, CJE I stands for income and it removes the income of the subsidiary from the parent's books. - S, A, and E are the same under all 3 methods. - Problem on next page

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts