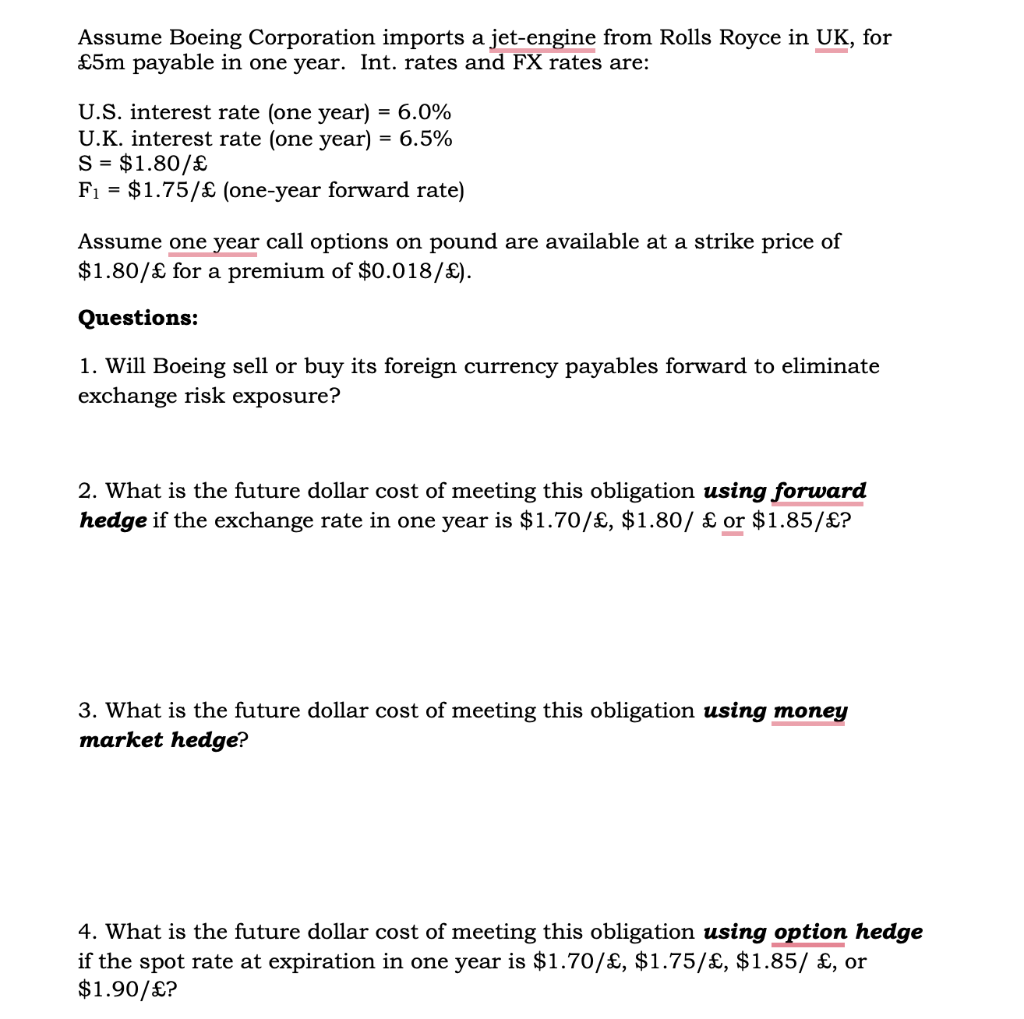

Question: Chapter 10 additional: U.S. interest rate (one year) =6.0% U.K. interest rate (one year) =6.5% S=$1.80/ F1=$1.75/ (one-year forward rate) Assume one year call options

Chapter 10 additional:

U.S. interest rate (one year) =6.0% U.K. interest rate (one year) =6.5% S=$1.80/ F1=$1.75/ (one-year forward rate) Assume one year call options on pound are available at a strike price of $1.80/ for a premium of $0.018/. Questions: 1. Will Boeing sell or buy its foreign currency payables forward to eliminate exchange risk exposure? 2. What is the future dollar cost of meeting this obligation using forward hedge if the exchange rate in one year is $1.70/,$1.80/ or $1.85/ ? 3. What is the future dollar cost of meeting this obligation using money market hedge? 4. What is the future dollar cost of meeting this obligation using option hedge if the spot rate at expiration in one year is $1.70/,$1.75/,$1.85/, or $1.90/

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts