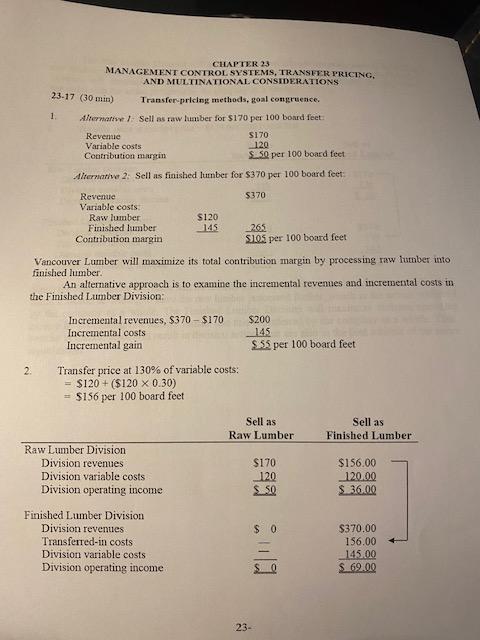

Question: CHAPTER 23 MANAGEMENT CONTROL SYSTEMS, TRANSFER PRICING, 23-17 (30 min) 1. AND MULTINATIONAL CONSIDERATIONS Transfer pricing methods, goal congruence. Alternative 1: Sell as raw

CHAPTER 23 MANAGEMENT CONTROL SYSTEMS, TRANSFER PRICING, 23-17 (30 min) 1. AND MULTINATIONAL CONSIDERATIONS Transfer pricing methods, goal congruence. Alternative 1: Sell as raw lumber for $170 per 100 board feet: Revenue Variable costs Contribution margin $170 120 $50 per 100 board feet Alternative 2: Sell as finished lumber for $370 per 100 board feet: Revenue $370 Variable costs Raw lumber $120 Finished lumber 145 265 Contribution margin $105 per 100 board feet Vancouver Lumber will maximize its total contribution margin by processing raw lumber into, finished lumber. An alternative approach is to examine the incremental revenues and incremental costs in the Finished Lumber Division: Incremental revenues, $370-$170 $200 Incremental costs 145 $55 per 100 board feet Incremental gain Transfer price at 130% of variable costs: 2. = $120+ ($120 x 0.30) $156 per 100 board feet Raw Lumber Division Division revenues Division variable costs. Division operating income Finished Lumber Division Division revenues Transferred-in costs Division variable costs. Division operating income Sell as Raw Lumber Sell as Finished Lumber $170 $156.00 120 120.00 $.50 $ 36.00 23- $ 0 $370.00 156.00 145.00 $ 69.00

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts