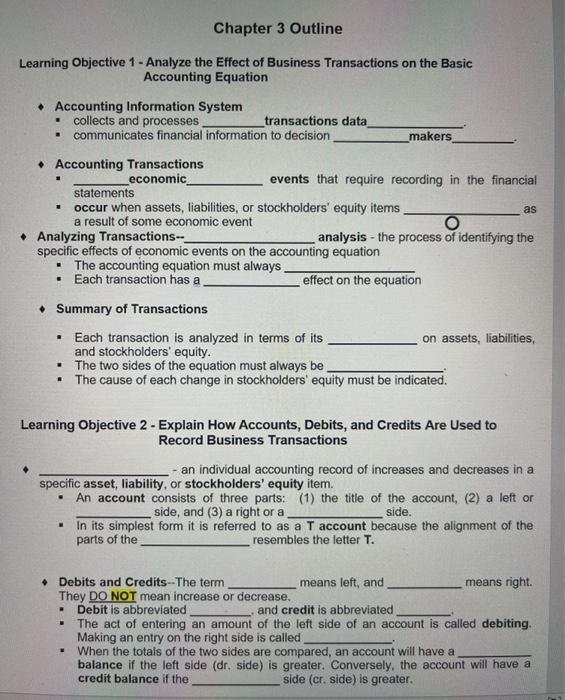

Question: Chapter 3 Outline Learning Objective 1 - Analyze the Effect of Business Transactions on the Basic Accounting Equation . . Accounting Information System collects and

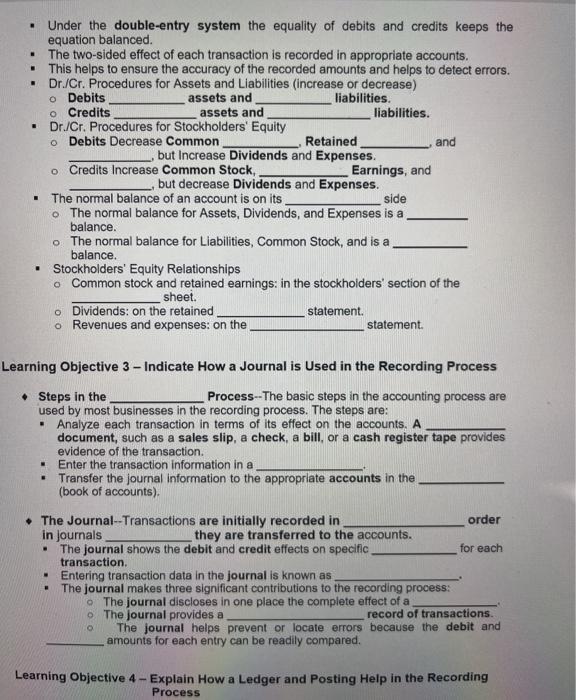

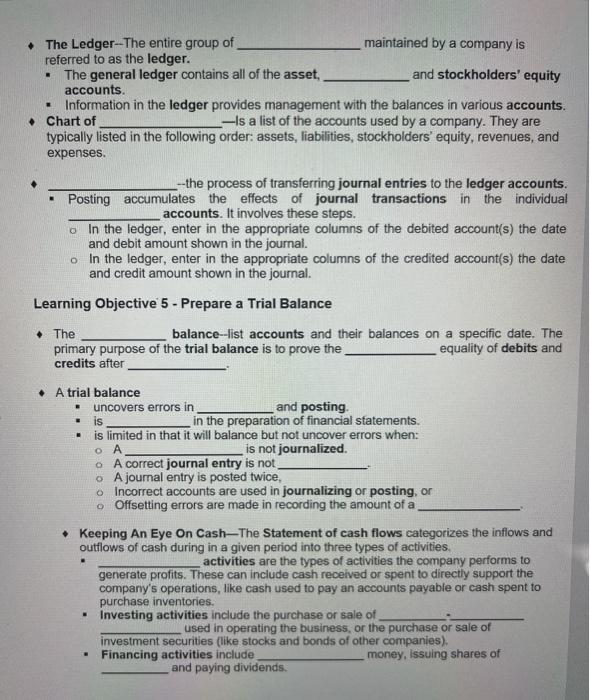

Chapter 3 Outline Learning Objective 1 - Analyze the Effect of Business Transactions on the Basic Accounting Equation . . Accounting Information System collects and processes transactions data communicates financial information to decision _makers Accounting Transactions economic events that require recording in the financial statements occur when assets, liabilities, or stockholders' equity items a result of some economic event O Analyzing Transactions- analysis - the process of identifying the specific effects of economic events on the accounting equation The accounting equation must always Each transaction has a effect on the equation Summary of Transactions . as . Each transaction is analyzed in terms of its on assets, liabilities, and stockholders' equity. The two sides of the equation must always be The cause of each change in stockholders' equity must be indicated. Learning Objective 2 - Explain How Accounts, Debits, and Credits Are Used to Record Business Transactions - an individual accounting record of increases and decreases in a specific asset, liability, or stockholders' equity item. An account consists of three parts: (1) the title of the account, (2) a left or side, and (3) a right or a side. In its simplest form it is referred to as a T account because the alignment of the parts of the resembles the letter T. Debits and Credits --The term means left, and means right. They DO NOT mean increase or decrease. Debit is abbreviated and credit is abbreviated The act of entering an amount of the left side of an account is called debiting. Making an entry on the right side is called When the totals of the two sides are compared, an account will have a balance if the left side (dr. side) is greater. Conversely, the account will have a credit balance if the side (cr. side) is greater. . . . Under the double-entry system the equality of debits and credits keeps the equation balanced. The two-sided effect of each transaction is recorded in appropriate accounts. . This helps to ensure the accuracy of the recorded amounts and helps to detect errors. . Dr./Cr. Procedures for Assets and Liabilities (increase or decrease) o Debits assets and liabilities. o Credits assets and liabilities. Dr./Cr. Procedures for Stockholders' Equity o Debits Decrease Common Retained and but Increase Dividends and Expenses. o Credits Increase Common Stock, Earnings, and .but decrease Dividends and Expenses. The normal balance of an account is on its side The normal balance for Assets, Dividends, and Expenses is a balance. The normal balance for Liabilities, Common Stock, and is a balance. Stockholders' Equity Relationships o Common stock and retained earnings: in the stockholders' section of the sheet. o Dividends on the retained statement. o Revenues and expenses: on the statement . Learning Objective 3 - Indicate How a Journal is used in the Recording Process Steps in the Process --The basic steps in the accounting process are used by most businesses in the recording process. The steps are: Analyze each transaction in terms of its effect on the accounts. A document, such as a sales slip, a check, a bill, or a cash register tape provides evidence of the transaction. - Enter the transaction information in a Transfer the journal information to the appropriate accounts in the (book of accounts) The Journal-- Transactions are initially recorded in order in journals they are transferred to the accounts. The journal shows the debit and credit effects on specific for each transaction. Entering transaction data in the journal is known as The journal makes three significant contributions to the recording process: o The journal discloses in one place the complete effect of a The Journal provides a record of transactions The journal helps prevent or locate errors because the debit and amounts for each entry can be readily compared. . o Learning Objective 4 - Explain How a Ledger and Posting Help in the Recording Process The Ledger--The entire group of maintained by a company is referred to as the ledger. The general ledger contains all of the asset, and stockholders' equity accounts. Information in the ledger provides management with the balances in various accounts. Chart of - Is a list of the accounts used by a company. They are typically listed in the following order: assets, liabilities, stockholders' equity, revenues, and expenses. --the process of transferring journal entries to the ledger accounts. Posting accumulates the effects of journal transactions in the individual accounts. It involves these steps. In the ledger, enter in the appropriate columns of the debited account(s) the date and debit amount shown in the journal. In the ledger, enter in the appropriate columns of the credited account(s) the date and credit amount shown in the journal. Learning Objective 5 - Prepare a Trial Balance The balance--list accounts and their balances on a specific date. The primary purpose of the trial balance is to prove the equality of debits and credits after A trial balance . uncovers errors in and posting is in the preparation of financial statements. . is limited in that it will balance but not uncover errors when: is not journalized A correct journal entry is not o A journal entry is posted twice, o Incorrect accounts are used in journalizing or posting, or o Offsetting errors are made in recording the amount of a Keeping An Eye On Cash-The Statement of cash flows categorizes the inflows and outflows of cash during in a given period into three types of activities activities are the types of activities the company performs to generate profits. These can include cash received or spent to directly support the company's operations, like cash used to pay an accounts payable or cash spent to purchase inventories. . Investing activities include the purchase or sale of used in operating the business, or the purchase or sale of investment securities (like stocks and bonds of other companies). Financing activities include money. Issuing shares of and paying dividends

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts