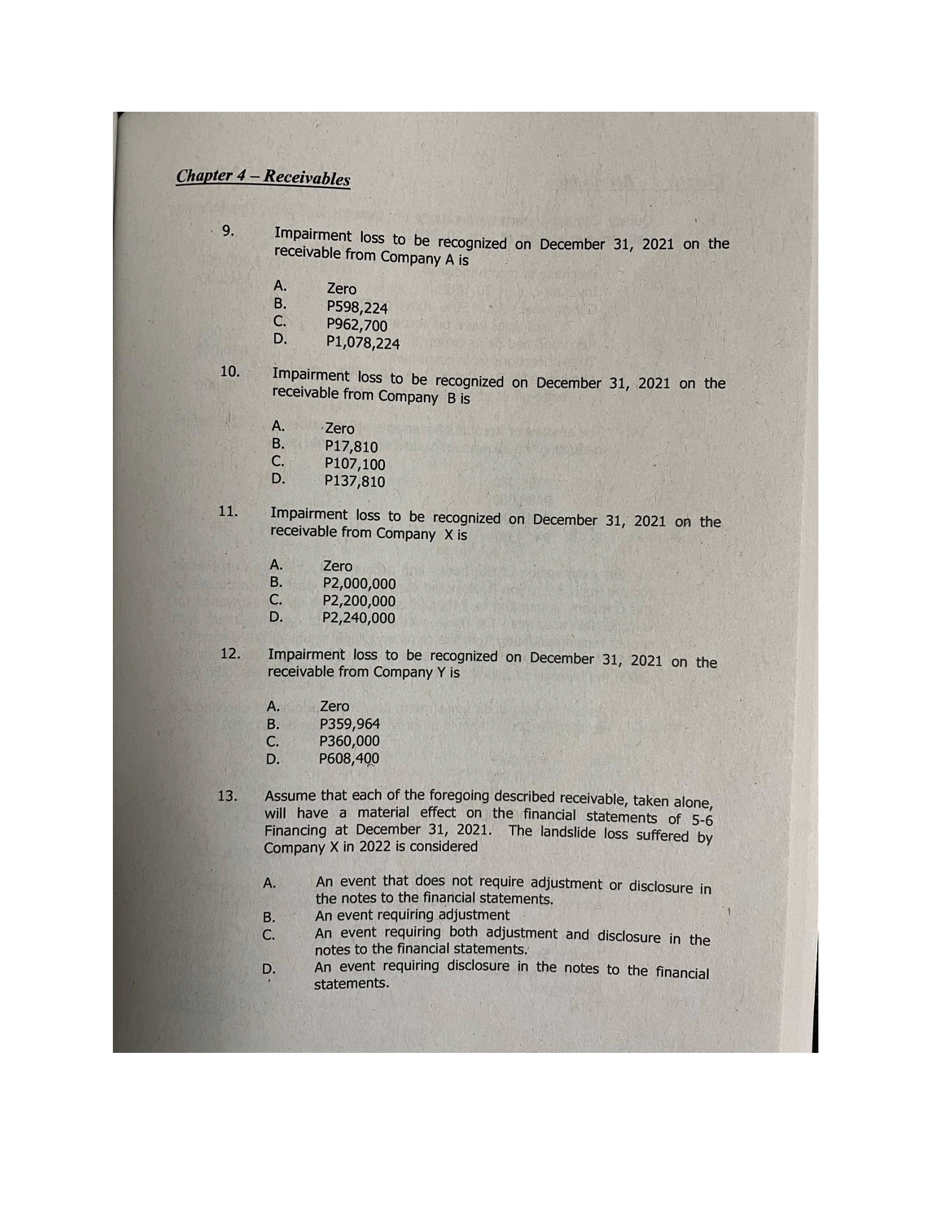

Question: Chapter 4 - Receivables 9. Impairment loss to be recognized on December 31, 2021 on the receivable from Company A is A. Zero P598,224 P962,700

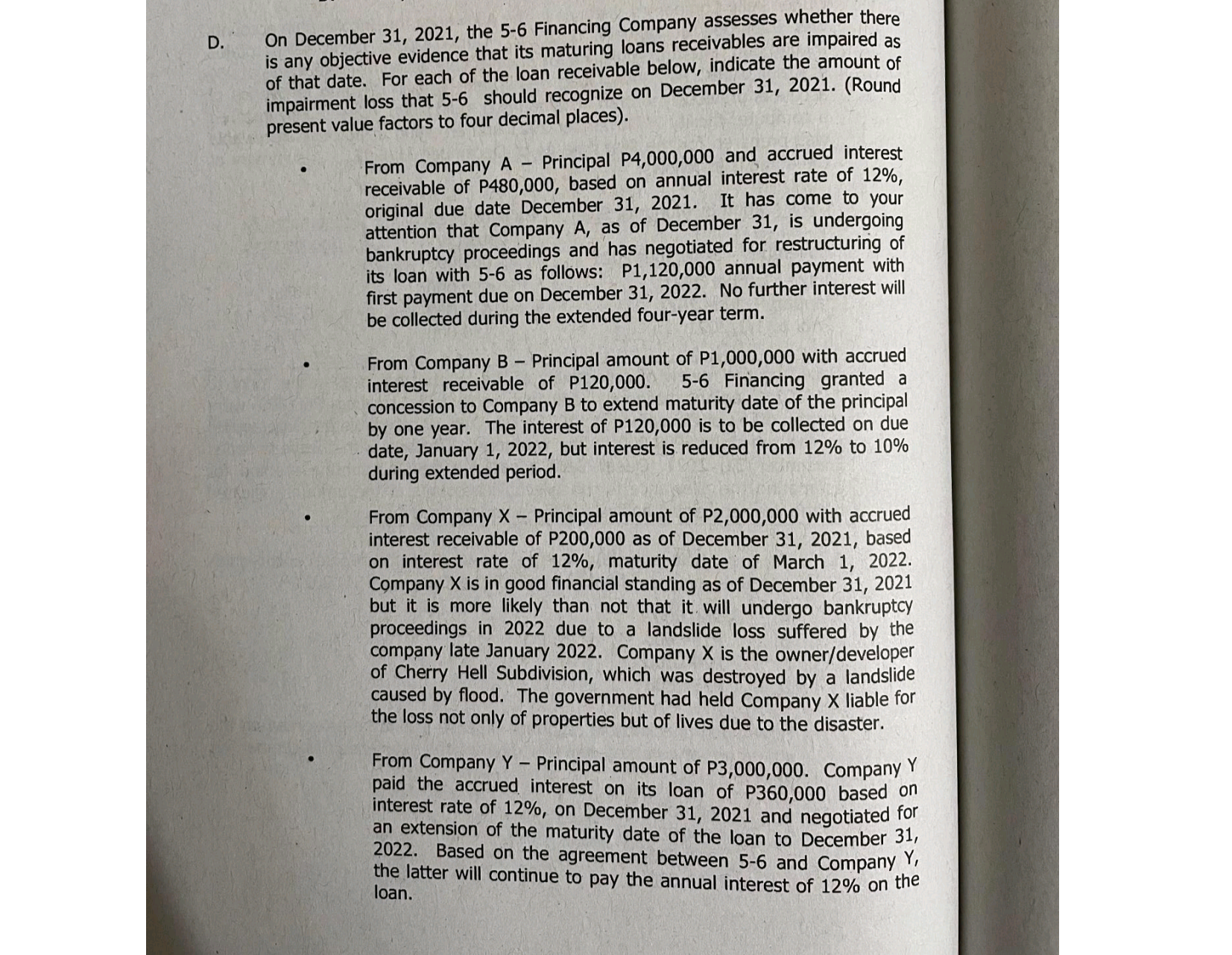

Chapter 4 - Receivables 9. Impairment loss to be recognized on December 31, 2021 on the receivable from Company A is A. Zero P598,224 P962,700 P1,078,224 10. Impairment loss to be recognized on December 31, 2021 on the receivable from Company B is Zero P17,810 P107,100 P137,810 11. Impairment loss to be recognized on December 31, 2021 on the receivable from Company X is Zero P2,000,000 P2,200,000 P2,240,000 12. Impairment loss to be recognized on December 31, 2021 on the receivable from Company Y is Zero P359,964 P360,000 P608,400 13. Assume that each of the foregoing described receivable, taken alone, will have a material effect on the financial statements of 5-6 Financing at December 31, 2021. The landslide loss suffered by Company X in 2022 is considered A. An event that does not require adjustment or disclosure in the notes to the financial statements. B. An event requiring adjustment C. An event requiring both adjustment and disclosure in the notes to the financial statements. D. An event requiring disclosure in the notes to the financial statements.D. On December 31, 2021, the 5-6 Financing Company assesses whether there is any objective evidence that its maturing loans receivables are impaired as of that date. For each of the loan receivable below, indicate the amount of impairment loss that 5-6 should recognize on December 31, 2021. (Round present value factors to four decimal places). From Company A - Principal P4,000,000 and accrued interest receivable of P480,000, based on annual interest rate of 12%, original due date December 31, 2021. It has come to your attention that Company A, as of December 31, is undergoing bankruptcy proceedings and has negotiated for restructuring of its loan with 5-6 as follows: P1,120,000 annual payment with first payment due on December 31, 2022. No further interest will be collected during the extended four-year term. From Company B - Principal amount of P1,000,000 with accrued interest receivable of P120,000. 5-6 Financing granted a concession to Company B to extend maturity date of the principal by one year. The interest of P120,000 is to be collected on due date, January 1, 2022, but interest is reduced from 12% to 10% during extended period. From Company X - Principal amount of P2,000,000 with accrued interest receivable of P200,000 as of December 31, 2021, based on interest rate of 12%, maturity date of March 1, 2022. Company X is in good financial standing as of December 31, 2021 but it is more likely than not that it will undergo bankruptcy proceedings in 2022 due to a landslide loss suffered by the company late January 2022. Company X is the owner/developer of Cherry Hell Subdivision, which was destroyed by a landslide caused by flood. The government had held Company X liable for the loss not only of properties but of lives due to the disaster. From Company Y - Principal amount of P3,000,000. Company Y paid the accrued interest on its loan of P360,000 based on interest rate of 12%, on December 31, 2021 and negotiated for an extension of the maturity date of the loan to December 31, 2022. Based on the agreement between 5-6 and Company Y, the latter will continue to pay the annual interest of 12 loan. of 12% on the

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock

Students Have Also Explored These Related Accounting Questions!