Question: Chapter 7 Question 20 20. Interest Rate Risk [LO2] Bond J has a coupon rate of 3 percent. Bond K has a coupon rate of

![Chapter 7 Question 20 20. Interest Rate Risk [LO2] Bond J](https://dsd5zvtm8ll6.cloudfront.net/si.experts.images/questions/2024/10/66ffb328d8ec7_57666ffb32868427.jpg)

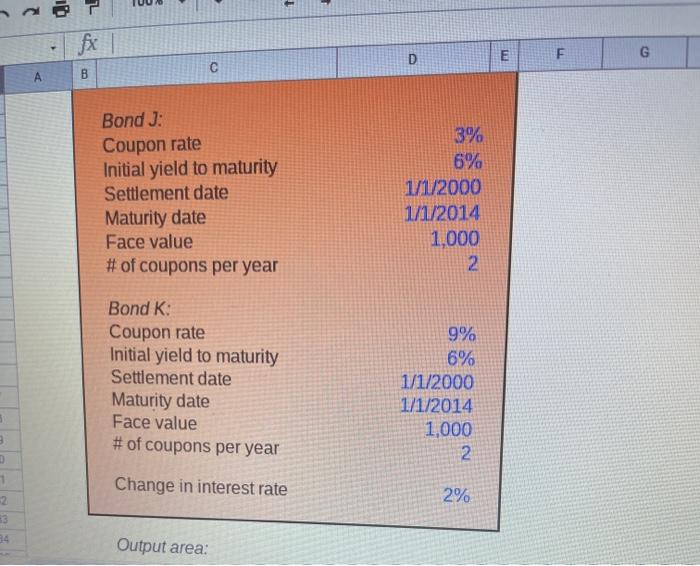

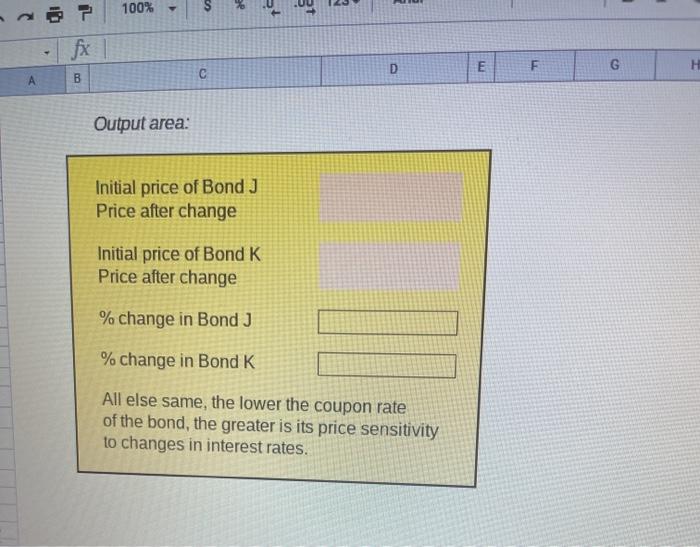

Chapter 7 Question 20 20. Interest Rate Risk [LO2] Bond J has a coupon rate of 3 percent. Bond K has a coupon rate of 9 percent. Both bonds have 14 years to maturity, make semiannual payments, and have a YTM of 6 percent. If interest rates suddenly rise by 2 percent, what is the percentage price change of these bonds? What if rates suddenly fall by 2 percent instead? What does this problem tell you about the interest rate risk of lower-coupon bonds? Input area: Bond J: Coupon rate Initial yield to maturity Settlement date Maturity date Face value # of coupons per year 3% 6% 1/1/2000 1/1/2014 1,000 2 10 1 E F D G A Bond J: Coupon rate Initial yield to maturity Settlement date Maturity date Face value # of coupons per year 3% 6% 1/1/2000 1/1/2014 1,000 2. Bond K Coupon rate Initial yield to maturity Settlement date Maturity date Face value # of coupons per year 9% 6% 1/1/2000 1/1/2014 1,000 2 3 9 D Change in interest rate 1 2 43 2% 34 Output area: ee 100% fx E D F G B Output area: Initial price of Bond J Price after change Initial price of Bond K Price after change % change in Bond J % change in Bond K All else same, the lower the coupon rate of the bond, the greater is its price sensitivity to changes in interest rates

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts