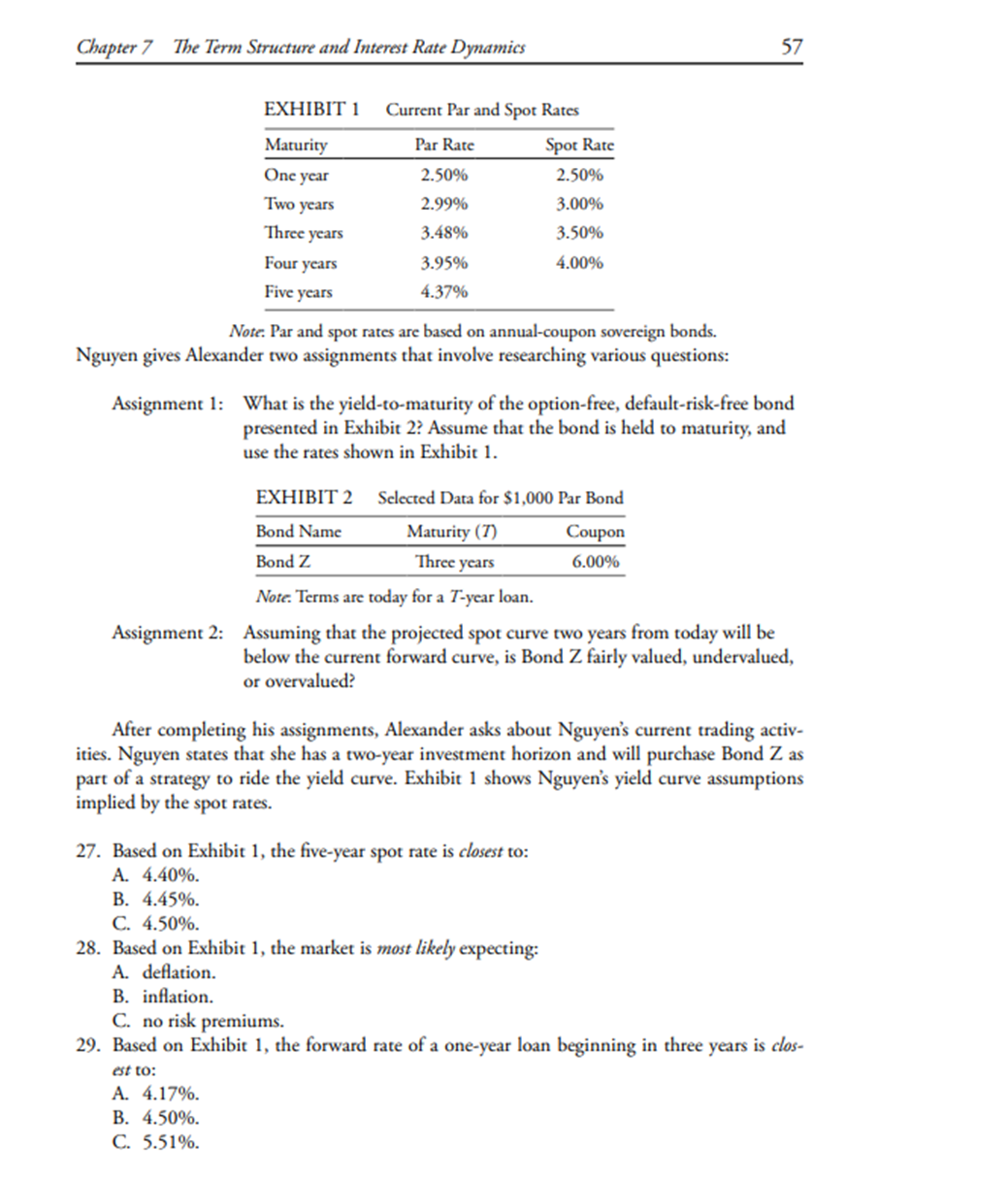

Question: Chapter 7 The Term Structure and Interest Rate Dynamics 57 EXHIBIT 1 Current Par and Spot Rates Maturity Par Rate Spot Rate One year 2.50%

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts