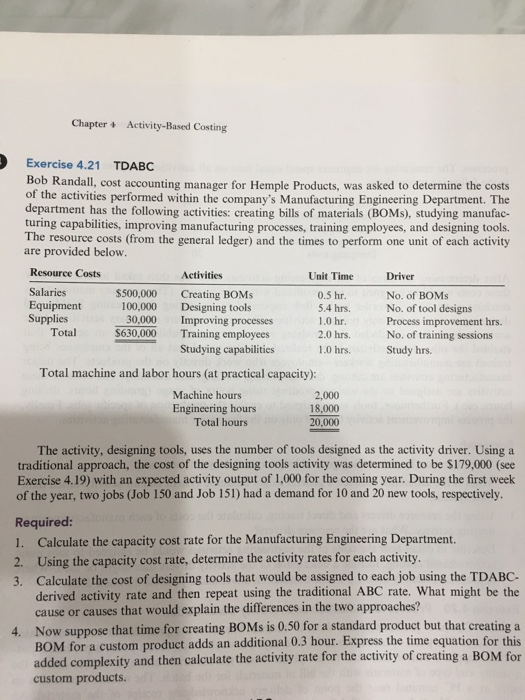

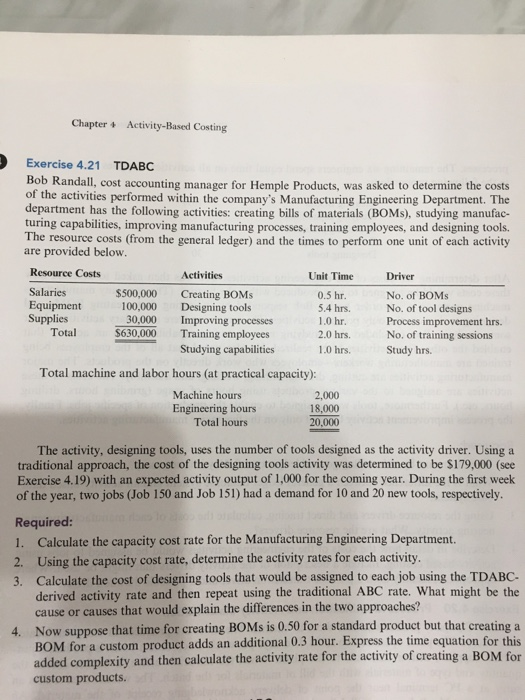

Question: Chapter + Activity-Based Costing Exercise 4.21 TDABC Bob Randall, cost accounting manager for Hemple Products, was asked to determine the costs of the activities performed

Chapter + Activity-Based Costing Exercise 4.21 TDABC Bob Randall, cost accounting manager for Hemple Products, was asked to determine the costs of the activities performed within the company's Manufacturing Engineering Department. The department has the following activities: creating bills of materials (BOMs), studying manufac- turing capabilities, improving manufacturing processes, tr The resource costs (from the general ledger) and the times to perform one unit of each activity are provided below. Driver Resource Costs Activities Unit Time Salaries $500,000 Creating BOMS M: 0.5 hr. Equipment 100,000 Designing tools 5.4 hrs. Supplies 30,000 Improving processes 1.0 hr. Total $630,000 Training employees 2.0 hrs. Studying capabilities 1.0 hrs. Total machine and labor hours (at practical capacity): Machine hours 2,000 Engineering hours 18.000 Total hours 20,000 No. of BOM No. of tool designs Process improvement hrs. No. of training sessions Study hrs. The activity, designing tools, uses the number of tools designed as the activity driver. Using a traditional approach, the cost of the designing tools activity was determined to be $179,000 (see Exercise 4.19) with an expected activity output of 1,000 for the coming year. During the first week of the year, two jobs (Job 150 and Job 151) had a demand for 10 and 20 new tools, respectively. Required: 1. Calculate the capacity cost rate for the Manufacturing Engineering Department. 2. Using the capacity cost rate, determine the activity rates for each activity. 3. Calculate the cost of designing tools that would be assigned to each job using the TDABC. derived activity rate and then repeat using the traditional ABC rate. What might be the cause or causes that would explain the differences in the two approaches? 4. Now suppose that time for creating BOMs is 0.50 for a standard product but that creating a BOM for a custom product adds an additional 0.3 hour. Express the time equation for this added complexity and then calculate the activity rate for the activity of creating a BOM for custom products. Chapter + Activity-Based Costing Exercise 4.21 TDABC Bob Randall, cost accounting manager for Hemple Products, was asked to determine the costs of the activities performed within the company's Manufacturing Engineering Department. The department has the following activities: creating bills of materials (BOMs), studying manufac- turing capabilities, improving manufacturing processes, training employees, and designing tools. The resource costs (from the general ledger) and the times to perform one unit of each activity are provided below. Resource Costs Activities Unit Time Driver Salaries $500,000 Creating BOMs Creatin No. of BOMs Equipment 100,000 Designing tools 5.4 hrs. No. of tool designs Supplies 30,000 Improving processes 1.0 hr. Process improvement hrs. Total $630,000 Training employees 2.0 hrs. No. of training sessions Studying capabilities 1.0 hrs. Study hrs. Total machine and labor hours (at practical capacity): Machine hours 2,000 Engineering hours 18.000 Total hours 20,000 The activity, designing tools, uses the number of tools designed as the activity driver. Using a traditional approach, the cost of the designing tools activity was determined to be $179,000 (see Exercise 4.19) with an expected activity output of 1,000 for the coming year. During the first week of the year, two jobs (Job 150 and Job 151) had a demand for 10 and 20 new tools, respectively. Required: 1. Calculate the capacity cost rate for the Manufacturing Engineering Department. 2. Using the capacity cost rate, determine the activity rates for each activity. 3. Calculate the cost of designing tools that would be assigned to each job using the TDABC. derived activity rate and then repeat using the traditional ABC rate. What might be the cause or causes that would explain the differences in the two approaches? 4. Now suppose that time for creating BOMs is 0.50 for a standard product but that creating a BOM for a custom product adds an additional 0.3 hour. Express the time equation for this added complexity and then calculate the activity rate for the activity of creating a BOM for custom products

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts