Question: Check my workCheck My Work button is now enabled Item 8 Item 8 6.25 points Following are separate financial statements of Michael Company and Aaron

Check my workCheck My Work button is now enabled

Item 8

Item 8 6.25 points

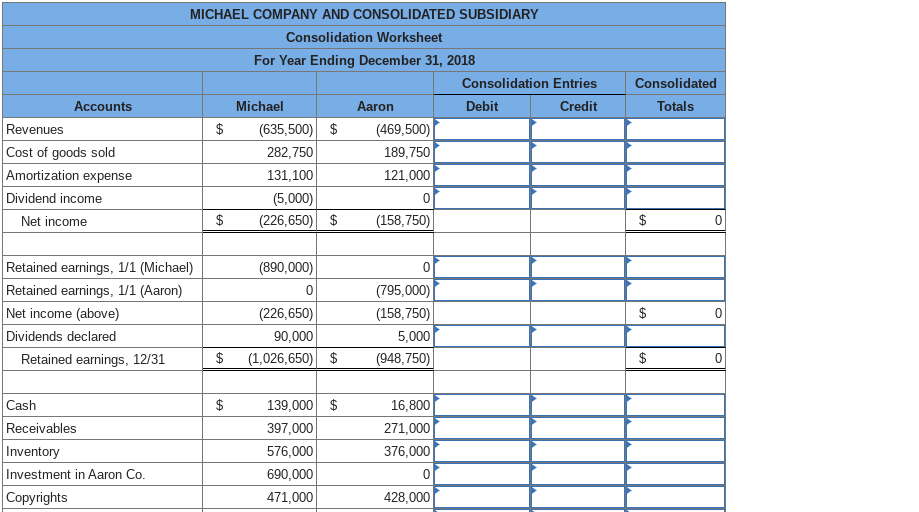

Following are separate financial statements of Michael Company and Aaron Company as of December 31, 2018 (credit balances indicated by parentheses). Michael acquired all of Aarons outstanding voting stock on January 1, 2014, by issuing 20,000 shares of its own $1 par common stock. On the acquisition date, Michael Companys stock actively traded at $34.50 per share.

| Michael Company 12/31/18 | Aaron Company 12/31/18 | ||||||

| Revenues | $ | (635,500 | ) | $ | (469,500 | ) | |

| Cost of goods sold | 282,750 | 189,750 | |||||

| Amortization expense | 131,100 | 121,000 | |||||

| Dividend income | (5,000 | ) | 0 | ||||

| Net income | $ | (226,650 | ) | $ | (158,750 | ) | |

| Retained earnings, 1/1/18 | $ | (890,000 | ) | $ | (795,000 | ) | |

| Net income (above) | (226,650 | ) | (158,750 | ) | |||

| Dividends declared | 90,000 | 5,000 | |||||

| Retained earnings, 12/31/18 | $ | (1,026,650 | ) | $ | (948,750 | ) | |

| Cash | $ | 139,000 | $ | 16,800 | |||

| Receivables | 397,000 | 271,000 | |||||

| Inventory | 576,000 | 376,000 | |||||

| Investment in Aaron Company | 690,000 | 0 | |||||

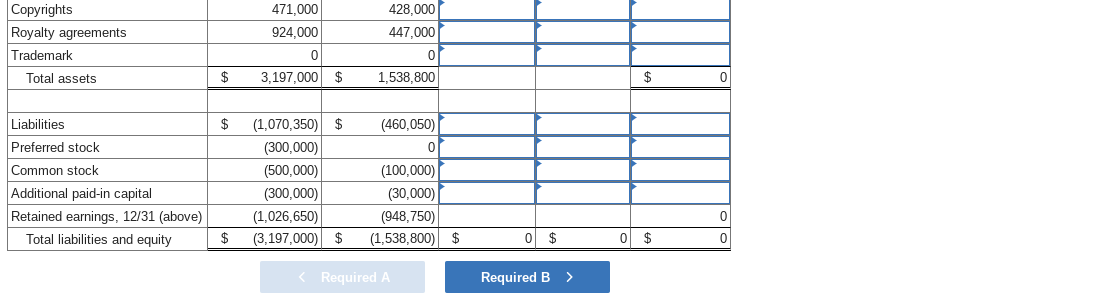

| Copyrights | 471,000 | 428,000 | |||||

| Royalty agreements | 924,000 | 447,000 | |||||

| Total assets | $ | 3,197,000 | $ | 1,538,800 | |||

| Liabilities | $ | (1,070,350 | ) | $ | (460,050 | ) | |

| Preferred stock | (300,000 | ) | 0 | ||||

| Common stock | (500,000 | ) | (100,000 | ) | |||

| Additional paid-in capital | (300,000 | ) | (30,000 | ) | |||

| Retained earnings, 12/31/18 | (1,026,650 | ) | (948,750 | ) | |||

| Total liabilities and equity | $ | (3,197,000 | ) | $ | (1,538,800 | ) | |

On the date of acquisition, Aaron reported retained earnings of $450,000 and a total book value of $580,000. At that time, its royalty agreements were undervalued by $60,000. This intangible was assumed to have a six-year remaining life with no residual value. Additionally, Aaron owned a trademark with a fair value of $50,000 and a 10-year remaining life that was not reflected on its books. Aaron declared and paid dividends in the same period.

-

a. Using the preceding information, prepare a consolidation worksheet for these two companies as of December 31, 2018.

-

b. Assuming that Michael applied the equity method to this investment, what account balances would differ on the parent's individual financial statements?

Consolidated Totals Accounts Revenues Cost of goods sold Amortization expense Dividend income Net income MICHAEL COMPANY AND CONSOLIDATED SUBSIDIARY Consolidation Worksheet For Year Ending December 31, 2018 Consolidation Entries Michael Aaron Debit Credit $ (635,500) $ (469,500) 282,750 189,750 131, 100 121,000 (5,000) 0 $ (226,650) $ (158,750) $ 0 (890,000) 0 Retained earnings, 1/1 (Michael) Retained earnings, 11 (Aaron) Net income (above) Dividends declared Retained earnings, 12/31 $ 0 (226,650) 90,000 (1,026,650) $ (795,000) (158,750) 5,000 (948,750) $ $ $ Cash Receivables Inventory Investment in Aaron Co. Copyrights 139,000 $ 397,000 576,000 690,000 471,000 16,800 271,000 376,000 0 428,000 Copyrights Royalty agreements Trademark Total assets 471,000 924,000 0 428,000 447,000 0 3,197,000 $ 1,538,800 $ 0 $ (460,050) 0 Liabilities Preferred stock Common stock Additional paid-in capital Retained earnings, 12/31 (above) Total liabilities and equity (1,070,350) $ (300,000) (500,000) (300,000) (1,026,650) (3,197,000) $ (100,000) (30,000) (948,750) (1,538,800) $ 0 0 $ 0 $ 0 $ Required A Required B >

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts