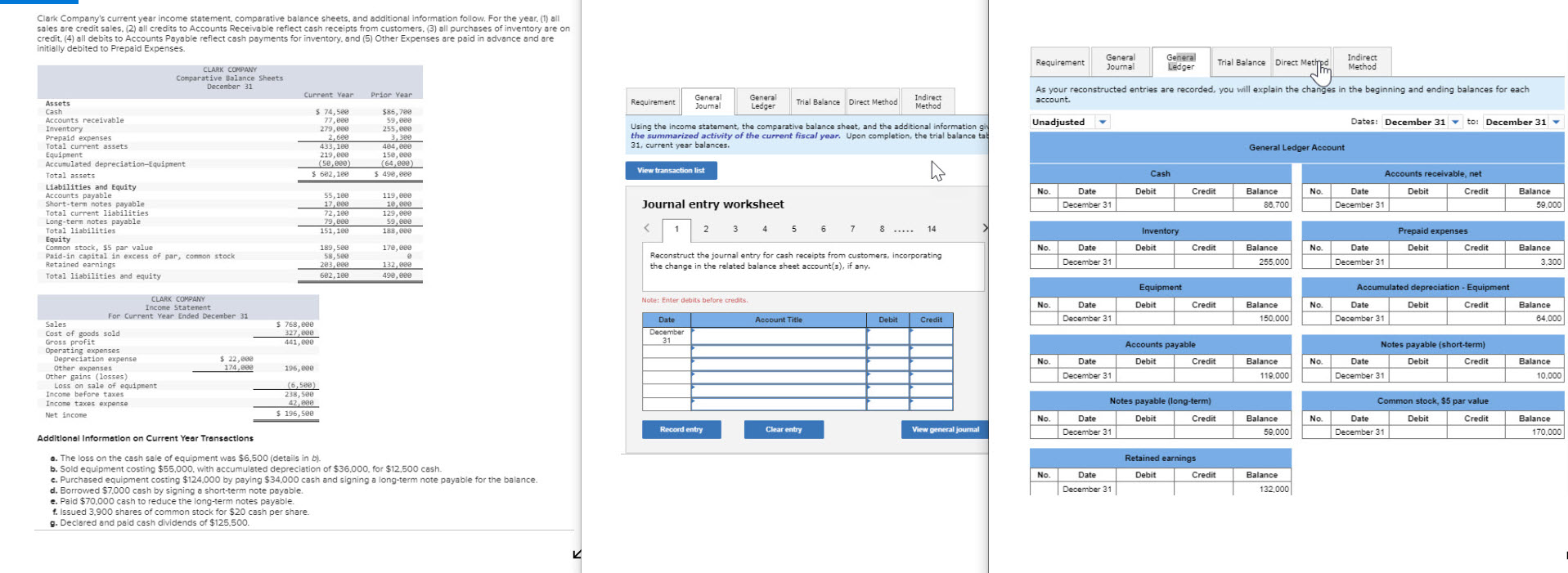

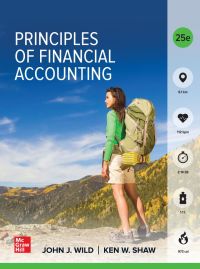

Clark Company's current year income statement, comparative balance sheets, and additional information follow. For the year....

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

Based on the information provided we can prepare the journal entries for the transactions of ... View the full answer

Related Book For

Principles Of Financial Accounting (Chapters 1-17)

ISBN: 9781260780147

25th Edition

Authors: John Wild

Posted Date: