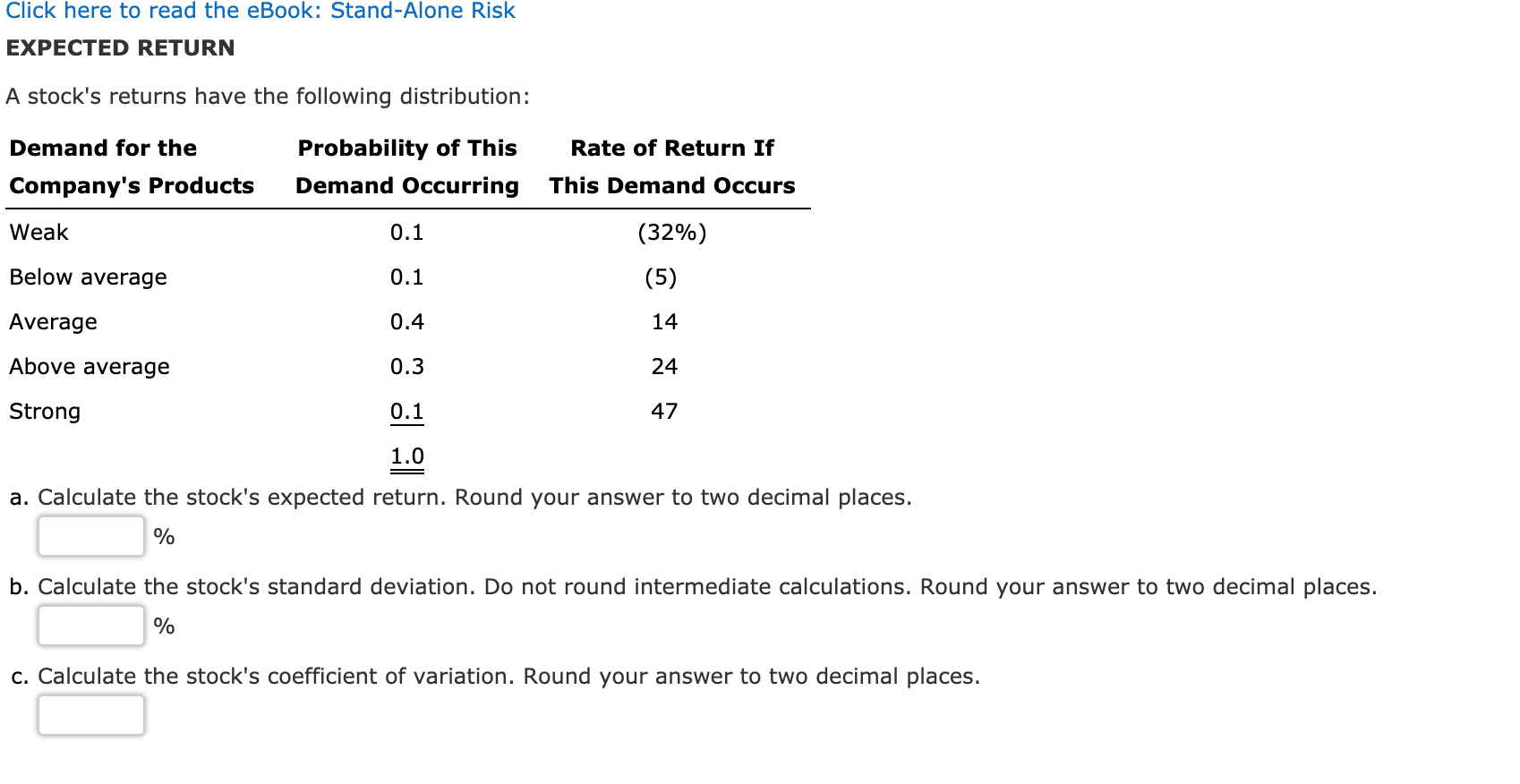

Question: Click here to read the eBook: Stand-Alone Risk EXPECTED RETURN A stock's returns have the following distribution: Demand for the Rate of Return If Probability

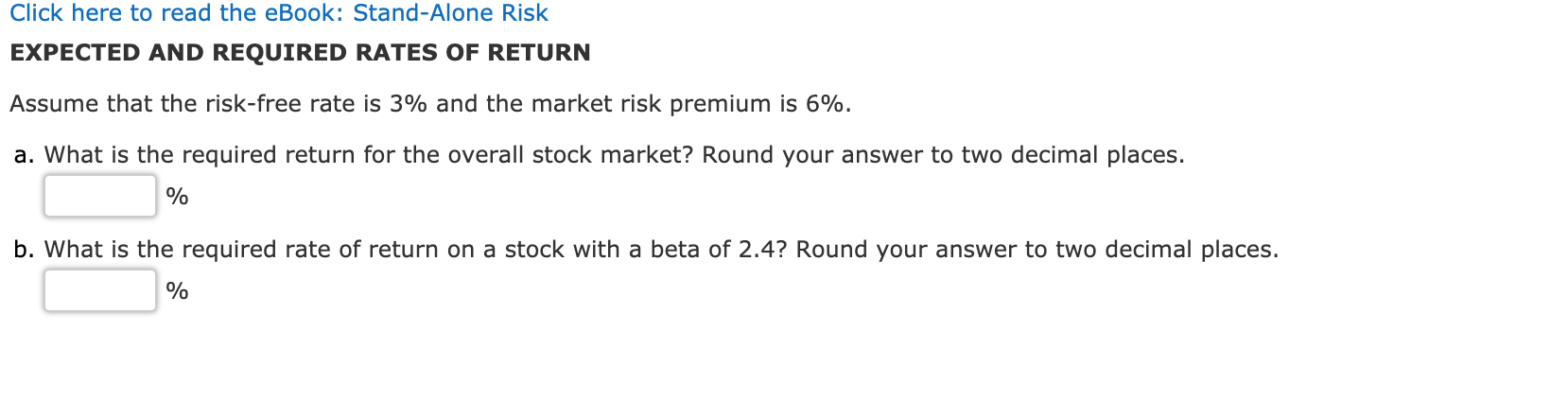

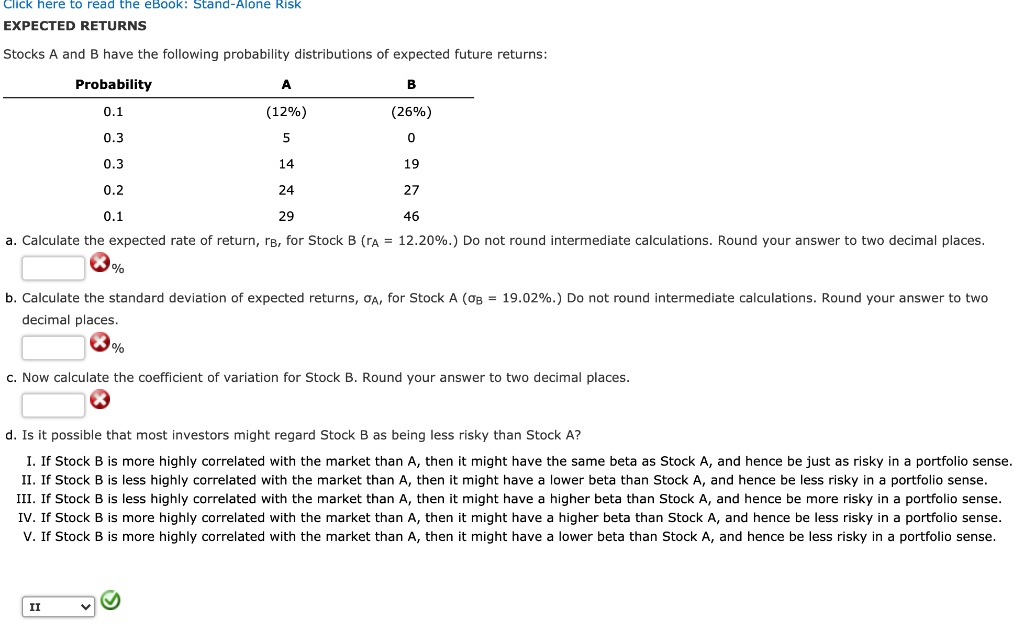

Click here to read the eBook: Stand-Alone Risk EXPECTED RETURN A stock's returns have the following distribution: Demand for the Rate of Return If Probability of this Demand Occurring Company's Products This Demand Occurs Weak 0.1 (32%) (5) Below average 0.1 Average 0.4 14 Above average 0.3 24 Strong 0.1 47 1.0 a. Calculate the stock's expected return. Round your answer to two decimal places. % b. Calculate the stock's standard deviation. Do not round intermediate calculations. Round your answer to two decimal places. % c. Calculate the stock's coefficient of variation. Round your answer to two decimal places. Click here to read the eBook: Stand-Alone Risk EXPECTED AND REQUIRED RATES OF RETURN Assume that the risk-free rate is 3% and the market risk premium is 6%. a. What is the required return for the overall stock market? Round your answer to two decimal places. % b. What is the required rate of return on a stock with a beta of 2.4? Round your answer to two decimal places. % Click here to read the eBook: Stand-Alone Risk EXPECTED RETURNS Stocks A and B have the following probability distributions of expected future returns: Probability A B 0.1 (12%) (26%) 0.3 5 0 0.3 14 19 0.2 24 27 0.1 29 46 a. Calculate the expected rate of return, rb, for Stock B (rA = 12.20%.) Do not round intermediate calculations. Round your answer to two decimal places. % b. Calculate the standard deviation of expected returns, OA, for Stock A (OB = 19.02%.) Do not round intermediate calculations. Round your answer to two decimal places. % c. Now calculate the coefficient of variation for Stock B. Round your answer to two decimal places. d. Is it possible that most investors might regard Stock B as being less risky than Stock A? I. If Stock B is more highly correlated with the market than A, then it might have the same beta as Stock A, and hence be just as risky in a portfolio sense. II. If Stock B is less highly correlated with the market than A, then it might have a lower beta than Stock A, and hence be less risky in a portfolio sense. III. If Stock B is less highly correlated with the market than A, then it might have a higher beta than Stock A, and hence be more risky in a portfolio sense. IV. If Stock B is more highly correlated with the market than A, then it might have a higher beta than Stock A, and hence be less risky in a portfolio sense. V. If Stock B is more highly correlated with the market than A, then it might have a lower beta than Stock A, and hence be less risky in a portfolio sense

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts