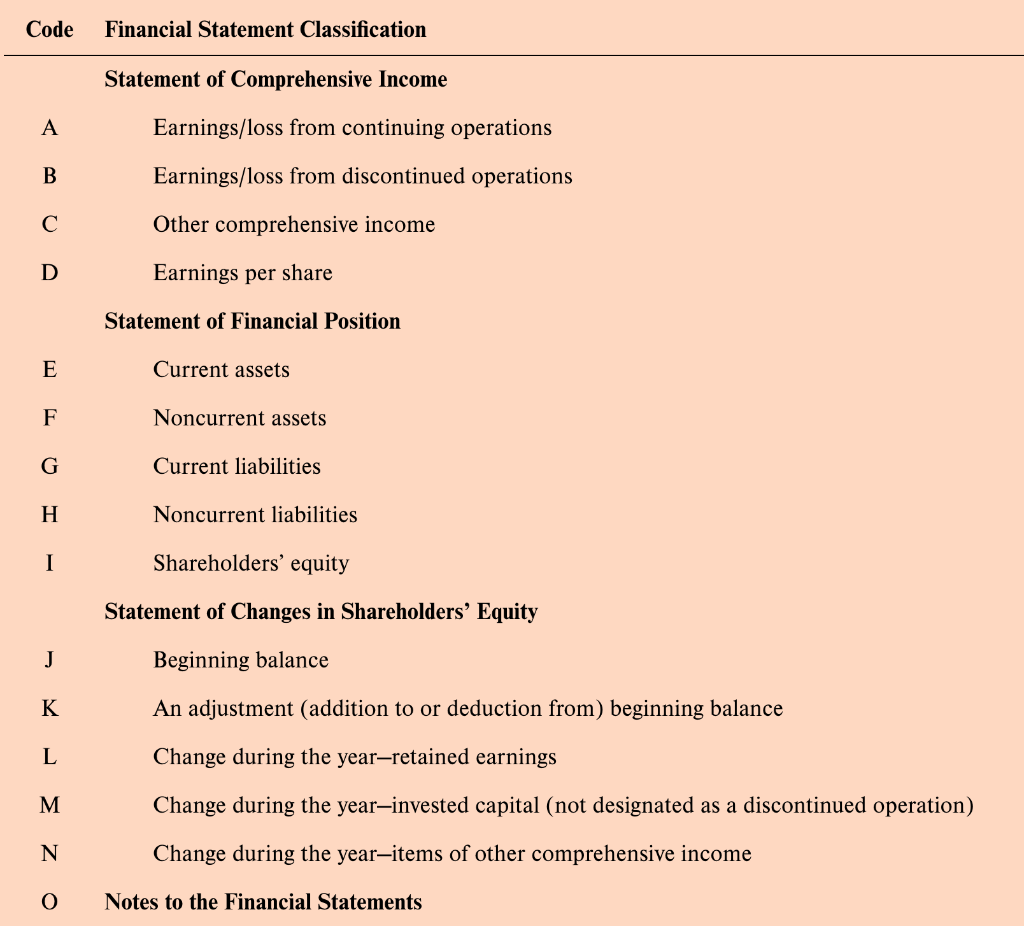

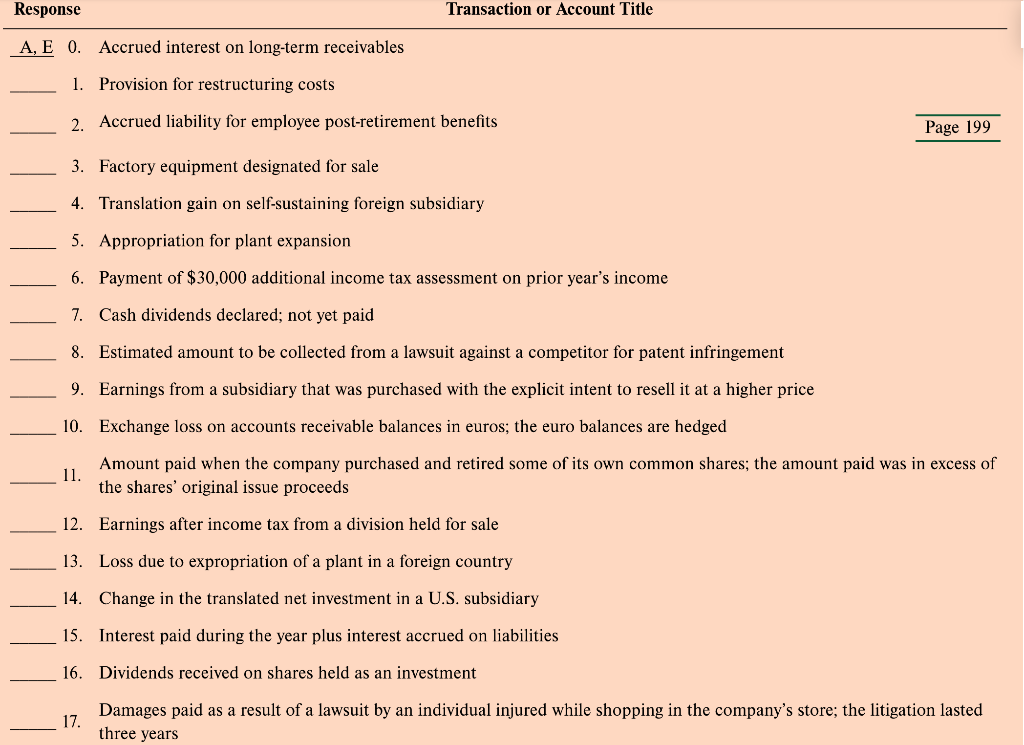

Question: Code Financial Statement Classification Statement of Comprehensive Income A Earnings/loss from continuing operations B Earnings/loss from discontinued operations C Other comprehensive income D Earnings per

Code Financial Statement Classification Statement of Comprehensive Income A Earnings/loss from continuing operations B Earnings/loss from discontinued operations C Other comprehensive income D Earnings per share Statement of Financial Position E Current assets F Noncurrent assets G Current liabilities H Noncurrent liabilities I Shareholders' equity Statement of Changes in Shareholders' Equity J Beginning balance K An adjustment (addition to or deduction from) beginning balance L Change during the year-retained earnings M Change during the year-invested capital (not designated as a discontinued operation) N Change during the year-items of other comprehensive income 0 Notes to the Financial Statements Response Transaction or Account Title A, E 0. Accrued interest on long-term receivables 1. Provision for restructuring costs 2. Accrued liability for employee post-retirement benefits Page 199 3. Factory equipment designated for sale 4. Translation gain on self-sustaining foreign subsidiary 5. Appropriation for plant expansion 6. Payment of $30,000 additional income tax assessment on prior year's income 7. Cash dividends declared; not yet paid 8. Estimated amount to be collected from a lawsuit against a competitor for patent infringement 9. Earnings from a subsidiary that was purchased with the explicit intent to resell it at a higher price 10. Exchange loss on accounts receivable balances in euros; the euro balances are hedged 11. Amount paid when the company purchased and retired some of its own common shares; the amount paid was in excess of the shares' original issue proceeds 12. Earnings after income tax from a division held for sale 13. Loss due to expropriation of a plant in a foreign country 14. Change in the translated net investment in a U.S. subsidiary 15. Interest paid during the year plus interest accrued on liabilities 16. Dividends received on shares held as an investment Damages paid as a result of a lawsuit by an individual injured while shopping in the company's store; the litigation lasted 17. three years 18. Cumulative effect of a change in accounting policy 19. A $100,000 bad debt is to be written off-the receivable had been outstanding for five years; the company estimates bad debts each year and has an allowance for bad debts 20. Adjustment due to correction of an error during current year; the error was made two years earlier

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts