Question: Code the question asked using MATLAB. Read the whole question and use the sub plus command as stated in the directions 1. (50pt) Write a

Code the question asked using MATLAB. Read the whole question and use the sub plus command as stated in the directions

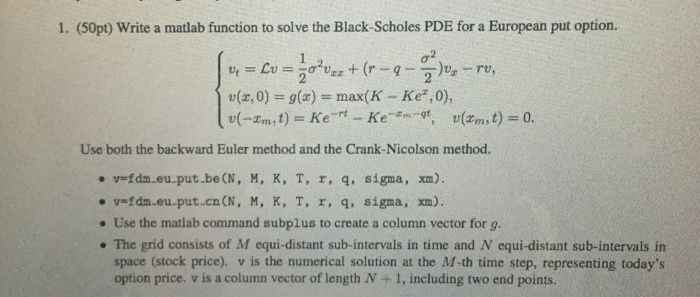

1. (50pt) Write a matlab function to solve the Black-Scholes PDE for a European put option. 2 Use both the backward Euler method and the Crank-Nicolson method vefdm.euput.be (N, M, K, T, r, q, sigma, xm). v-fdm.eu-put.cn(N, M, K, T, r, q, sigma, xm). . Use the matlab command subplus to create a column vector for g. . The grid consists of M equi-distant sub-intervals in time and N equi-distant sub-intervals in space (stock price). v is the numerical solution at the M-th time step, representing today's option price. v is a column vector of length N + 1, including two end points

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock