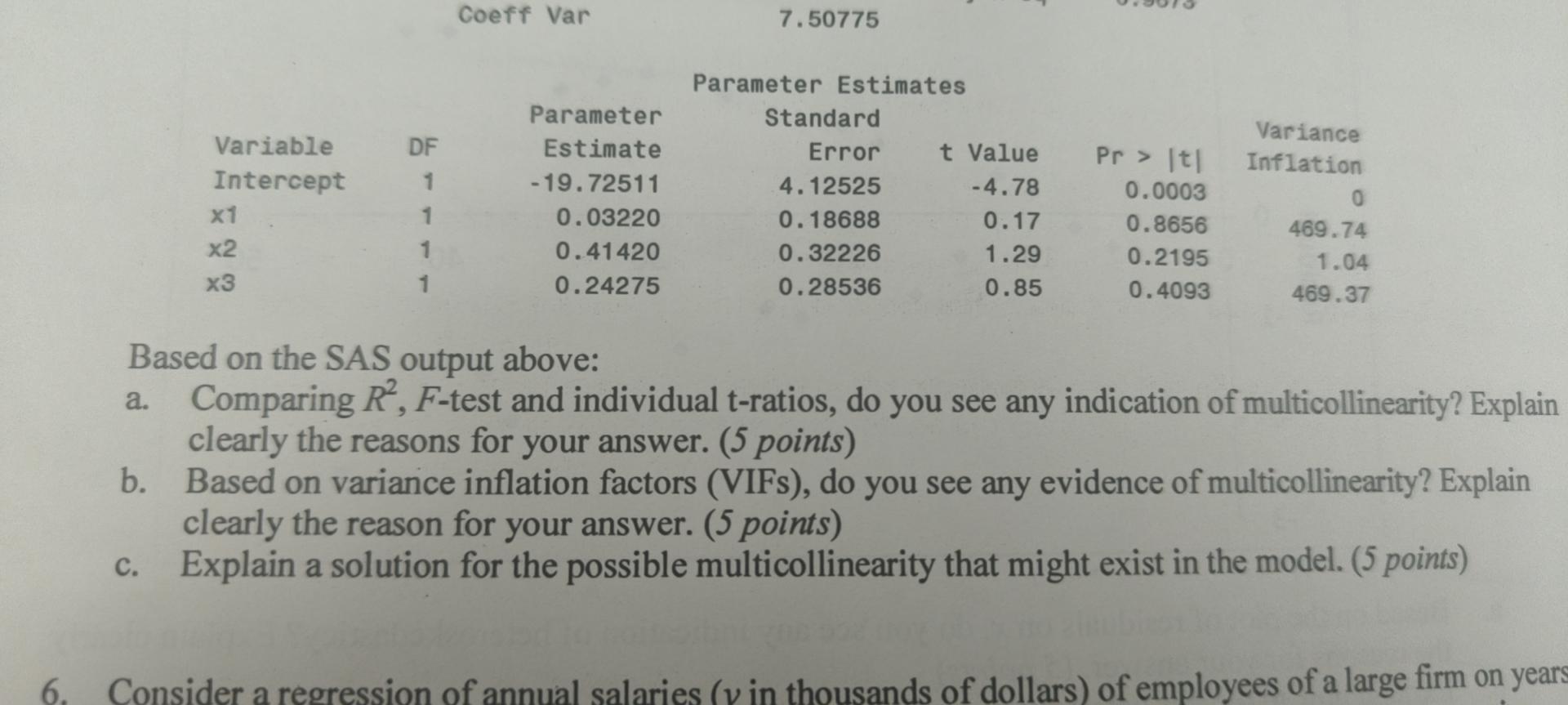

Question: Coeff Var 7.50775 Parameter Estimates Parameter Standard Variance Variable DF Estimate Error t Value Pr > t Inflation Intercept 1 -19.72511 4.12525 -4.78 0.0003

Coeff Var 7.50775 Parameter Estimates Parameter Standard Variance Variable DF Estimate Error t Value Pr > \t\ Inflation Intercept 1 -19.72511 4.12525 -4.78 0.0003 x1 1 0.03220 0.18688 0.17 0.8656 469.74 x2 1 0.41420 0.32226 1.29 0.2195 1.04 x3 1 0.24275 0.28536 0.85 0.4093 469.37 6. Based on the SAS output above: a. Comparing R, F-test and individual t-ratios, do you see any indication of multicollinearity? Explain clearly the reasons for your answer. (5 points) b. Based on variance inflation factors (VIFs), do you see any evidence of multicollinearity? Explain clearly the reason for your answer. (5 points) c. Explain a solution for the possible multicollinearity that might exist in the model. (5 points) Consider a regression of annual salaries (y in thousands of dollars) of employees of a large firm on years

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts