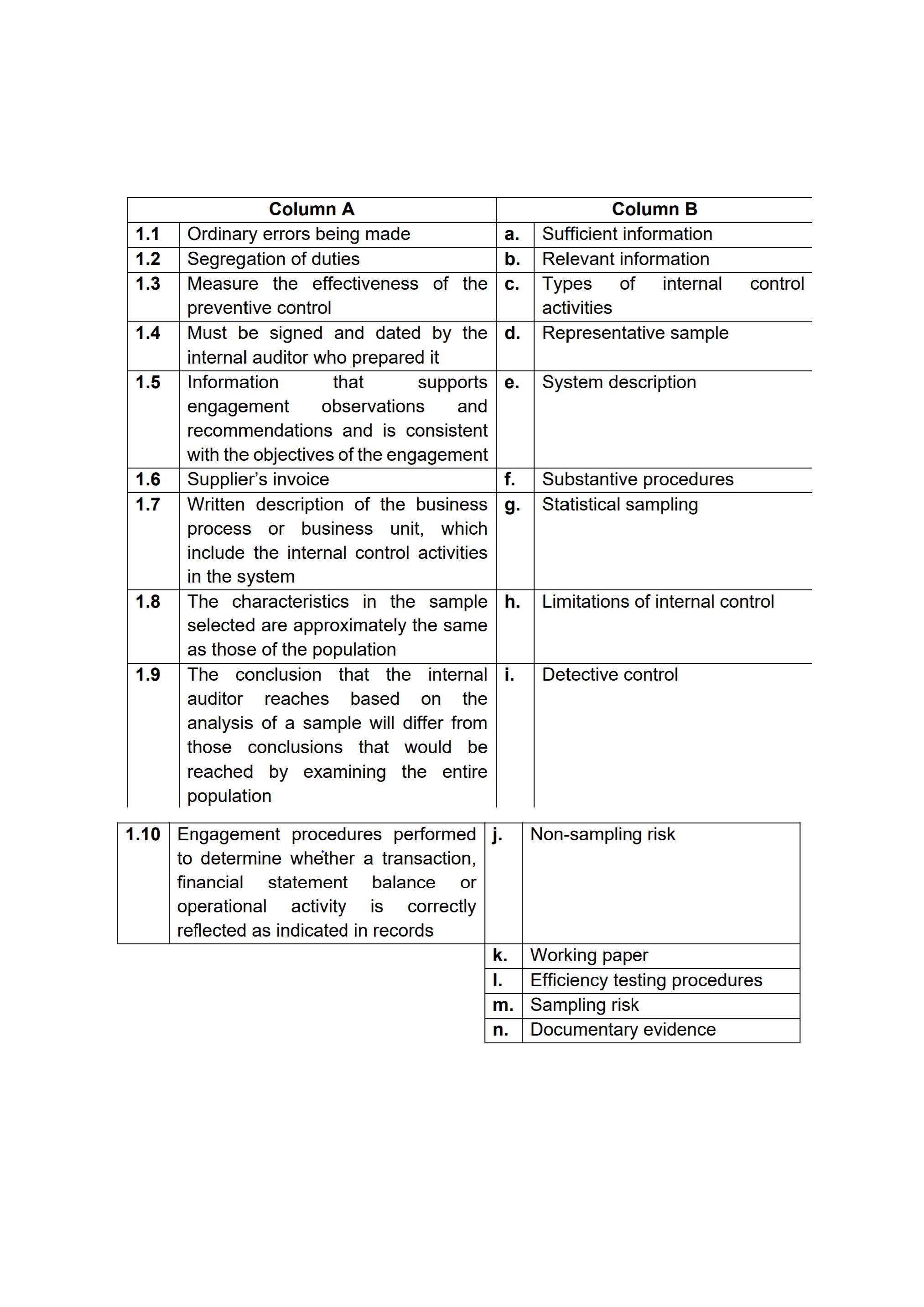

Question: Column A Column B 1.1 1.2 Ordinary errors being made Segregation of duties Sufcient information Relevant information 1.3 Measure the effectiveness of the preventive control

Column A Column B 1.1 1.2 Ordinary errors being made Segregation of duties Sufcient information Relevant information 1.3 Measure the effectiveness of the preventive control Types of internal control activities 1.4 Must be signed and dated by the internal auditor who prepared it Representative sample 1.5 Information that supports engagement observations and recommendations and is consistent with the objectives of the engagement System description 1.6 Supplier's invoice Substantive procedures 1.7 Written description of the business process or business unit, which include the internal control activities in the system Statistical sampling 1.8 The characteristics in the sample selected are approximately the same as those of the population Limitations of internal control 1.9 The conclusion that the internal auditor reaches based on the analysis of a sample will differ from those conclusions that would be reached by examining the entire population Detective control 1.10 Engagement procedures performed j. to determine whether a transaction, financial statement balance or operational activity is correctly reected as indicated in records Non-sampling risk Working paper Efciency testing procedures Sampling risk Documentary evidence

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts