Companies pay their shareholders dividends. The dividends can be ordinary dividends (box 1a of the Form 1099-DIV)

Question:

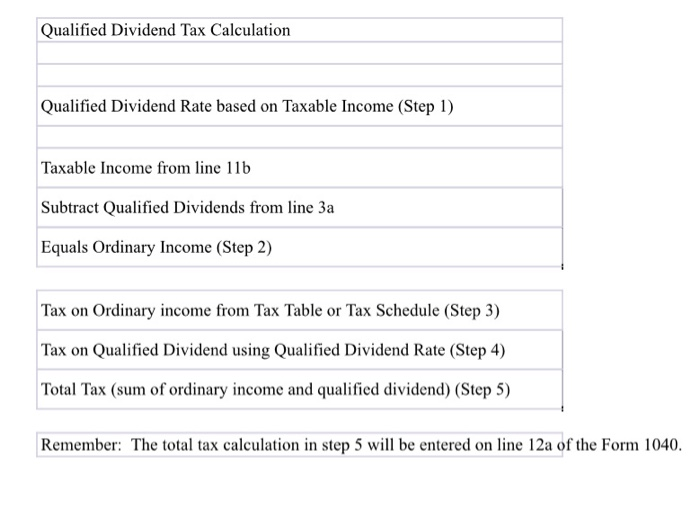

Companies pay their shareholders dividends. The dividends can be "ordinary dividends" (box 1a of the Form 1099-DIV) or they can be "ordinary dividends" AND "qualified dividends" (box 1b of the Form 1099-DIV). If they are "ordinary" they are taxed at the taxpayer's regular tax rate from the tax rate schedules.

To be a "qualified dividend", they (1) made from the earnings and profits of the corporation and (2) are from domestic corporations or qualified foreign corporations.

If they are "qualified dividend" they are taxed at lower rates. These rates are 0% for lower income tax payers to 20% for high income taxpayers. See the qualified dividend tax instructions for the exact breakdown of rates based on income.

If there are qualified dividends, you need to do two separate tax calculations. One for all the income except the dividend and one calculation for the dividend. Then, you will add them together. This total is reported as the tax on the Form 1040.

There is no tax benefit for qualified dividends for Wisconsin tax purposes.

2019 tax year

1. A single individual has taxable income of $120,000. Included in that amount, is a qualified dividend of $2,000. What is his tax liability?

2. A single individual has taxable income of $25,000. Included in that amount is a qualified dividend of $1,000. What is his tax liability?

3. A married couple filing jointly has taxable income of $200,000. Included in their income is a qualified dividend of $3,000. What is their tax liability?

.

Expert Answer:

1 For the single individual with taxable income of 120000 and a qualified dividend of 2000 the tax l... View the full answer

Essentials of Contemporary Management

ISBN: ?978-0077439477

5th edition

Authors: Gareth Jones, Jennifer George