Question: Company JK s common shares are held by the Kay family. JK has significant bank loans, which require the company to submit audited financial statements.

Company JKs common shares are held by the Kay family. JK has significant bank loans, which require the company to submit audited financial statements. JK manufactures hightechnology consumer electronics and has a December yearend. JK generally closes its yearend books by the middle of February in preparation for the yearend audit.

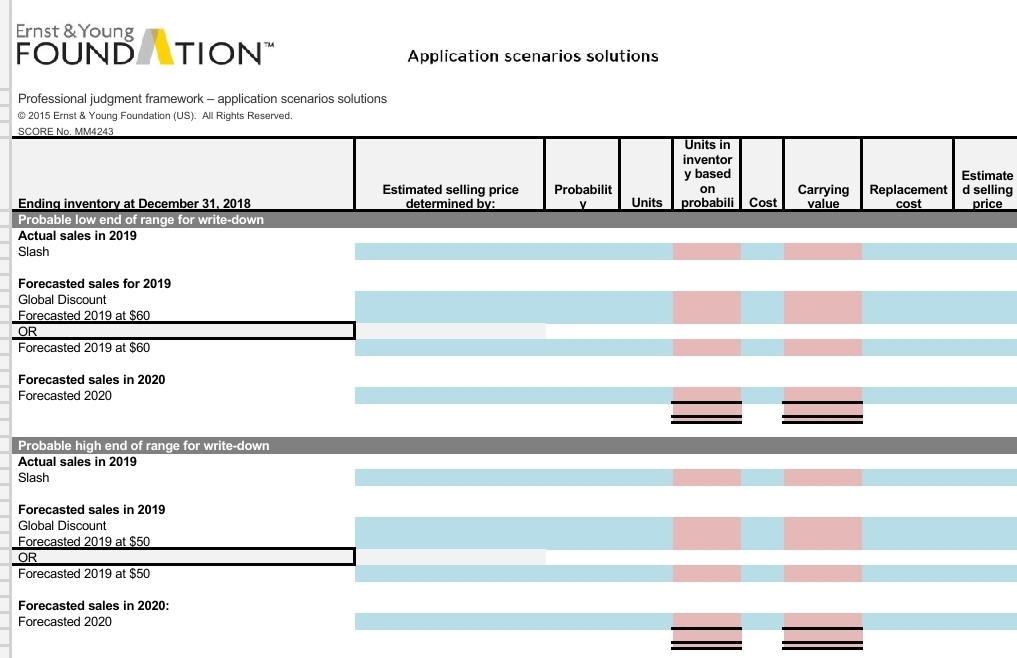

JK began manufacturing BOX A its first version of a computer tablet, in the first quarter of Early in the third quarter of JK introduced BOX B its newest computer tablet, with several enhanced features over BOX A Production of BOX A was halted after the second quarter of and replaced by production of BOX B The sales of BOX B have been very strong since its introduction; however, this has resulted in a reduced demand for the remaining units of BOX A JK has two competitors with products similar, but not identical, to Box A in terms of functionality. JK has historically been the product leader in this industry and has been able to command a higher sales price than its competitors, generally ranging from to

The CFO believes that there is an impairment issue related to the BOX A inventory. The CFO believes bonuses may still be earned in if the writedown of the BOX A product line is minimal. In compliance with ASC C JK is required to determine if any adjustments are necessary to value its LIFO inventory at the lower of cost or market. The ASC master glossary provides the following definitions of market and net realizable value:

Market:

As used in the phrase lower of cost or market, the term market means current replacement cost by purchase or by reproduction, as the case may be provided that it meets both of the following conditions:

a Market shall not exceed the net realizable value.

b Market shall not be less than net realizable value reduced by an allowance for an approximately normal profit margin.

Net realizable value:

Estimated selling price in the ordinary course of business less reasonably predictable costs of completion and disposal.

Historically, JK has applied the lower of cost or market rule directly to each item of inventory. The normal profit margin has been of the selling price.

In early February as directed by the CFO, the controller of JK began the process to value the BOX A units in inventory at December Available information regarding this inventory follows:

Fiscal and data

Fiscal financial information was audited and a clean opinion was issued. There have been no significant changes in systems and controls.

All inventories use the LIFO costing method. The average cost for each unit of BOX A produced in was $ Due to reduction in the number of units produced, the average cost for each unit of BOX A produced in was $ At December and BOX A inventory represented and of total assets, respectively.

Sales of BOX A represented of JKs revenue in and in

The last quarter of the year has historically been the best sales quarter, largely due to holidayrelated sales. The average selling price of BOX A in was $ In the average selling price began to drop when a competitor introduced a technologyenhanced computer tablet late in the first quarter and the decline continued when BOX B was introduced in the third quarter. The average selling price per unit for BOX A was $ in the first quarter, $ in the second quarter and $ in the third quarter. In response to the falling demand for BOX A starting in the fourth quarter of JK reduced the selling price by to $

January data

Despite the reduced selling price, JKs two largest customers, Better Buyer and Pad Warehouse, which account for of JKs sales volume, have refused to purchase any more units of BOX A In their view, the technology of BOX A is outdated and unsalable. To make matters worse, these customers are pressuring JK to take back units of BOX A they both still have on hand.

Company policy is not to allow customers to return inventory unless there is a warranty issue. The CFO has taken the position that they should not allow these two large customers to return unwanted product because it may indicate a higher inventory writedown is required.

The controller met with the Senior VP of Sales to discuss the value of the BOX A units. The VP expressed concerned that, if the unwanted BOX A product is not taken back, the companys distribution channels for BOX B could be disrupted.

A longtime discount chain customer, Slash, honored their outstanding purchase contract and, in January took possession of units of BOX A at $ per unit.

Early February data

Because of the significance of the customer relationships, rather than take the units back from Better Buyer and Pad Warehouse, which had been sold at an average price of $ JK decided to issue credit memos totaling $ resulting in a deeply discounted sales price of $ per unit.

The Senior VP of Sales, an industry veteran with a long history of solid forecasting of other products made by JK does share some good news. The current forecast is to sell units of BOX A in of which units were sold in January to Slash and the remaining units in This forecast is based, in part, on discussions with and letters from a discount chain in a thirdworld country, Global Discount, which may be willing to buy units of BOX A for $ million $ per unit The VP of Sales believes this transaction has a chance of occurring based on direct conversations with the VP of Purchasing at Global Discount. If this transaction does not occur, the VP of Sales estimates the selling price of the remaining units in to be $ per unit. The selling price of the remaining units in is forecasted to be discounted $ per unit from the price.

The controller becomes aware that the sales incentive cost on BOX A doubled to $ per unit beginning in

At a senior management meeting, the CEO made it clear she would prefer to write this inventory down as far as possible to be conservative and to enhance the chance for bonuses in The CFO expressed his concern that a writeoff that is too significant could result in no bonuses in

A popular industry magazine published an article outlining the shortcomings of BOX A and recommending consumers dont purchase this product and, instead, purchase BOX B

In its history of sales of other technology products, JK has observed that there is a market of customers who shop low price points despite newer, available technology; however, the time lag of this interest, about months, continues to shorten.

The following is a brief summary of the BOX A inventory quantities since its introduction.

Quarter ended Quantity produced Quantity sold Quantity in inventory

March

June

September

December

March

June

September

December

Required

Reference the professional judgment framework handout and application template separately provided.

As the controller, use your judgment to recommend the carrying value for the BOX A inventory at December Using the professional judgment framework, complete the application template for all process steps and provide the appropriate information in the documentation column.

In performing your analysis, you should use an Excel spreadsheet to support any calculations.

Using the information you documented regarding the overarching considerations and the specific considerations for each process step in the framework, use the tool below to document your judgment about the specific amount of write down you are recommending JK record in a draft memorandum format that you will provide to the CFO not to exceed three pages Be sure to include specific references to the applicable guidance and quote the applicable guidance. Also, attach your Excel spreadsheet with your calculations. Upon completing your documentation, make sure that you are able to answer the following considerations:

Is the documentation sufficient to support your judgment?

Can another professional understand how you reached your conclusion including why reasonable outcomes and possible alternatives identified were not selected

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock