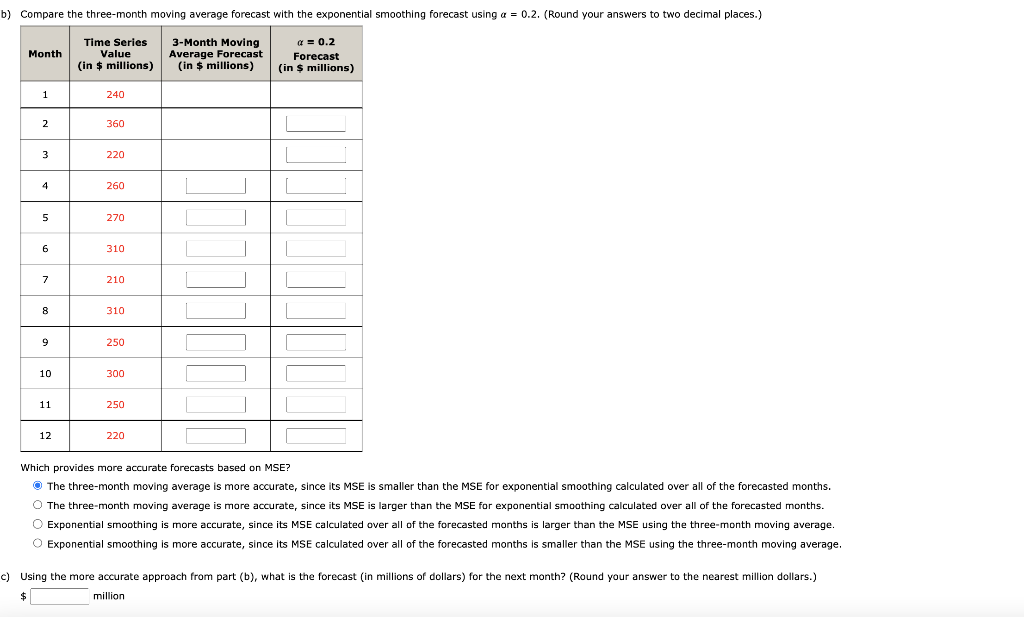

Question: Compare the three-month moving average forecast with the exponential smoothing forecast using =0.2. (Round your answers to two decimal places.) Which provides more accurate forecasts

Compare the three-month moving average forecast with the exponential smoothing forecast using =0.2. (Round your answers to two decimal places.) Which provides more accurate forecasts based on MSE? The three-month moving average is more accurate, since its MSE is smaller than the MSE for exponential smoothing calculated over all of the forecasted months. The three-month moving average is more accurate, since its MSE is larger than the MSE for exponential smoothing calculated over all of the forecasted months. Exponential smoothing is more accurate, since its MSE calculated over all of the forecasted months is larger than the MSE using the three-month moving average. Exponential smoothing is more accurate, since its MSE calculated over all of the forecasted months is smaller than the MSE using the three-month moving average

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts