Question: Compute and Describe for each loan as a 7/1 Arm Loan: 1. Payment over term of the loan 2. Nominal Interest Rate 3. Effective Interest

Compute and Describe for each loan as a 7/1 Arm Loan:

1. Payment over term of the loan

2. Nominal Interest Rate

3. Effective Interest Rate held to term

4. Effective Interest Rate held through holding period

5. Loan balance at end of holding period

6. Annual holding costs

7. Equity Return of Sale

8. Internal Rate of Return on Equity before taxes

9. Gross Income Needed to Qualify for Loan

Real Estate Taxes: $9,978.80 Insurance: $1,500.00

Living Area: 1,389 square feet Utilities: $1,800.00 Year Built: 1954 Maintenance: $1,800.00 Room Count: 5/3/2

Purchase Price: $890,000

Assumptions:

Holding Period: 10 years

Projected Price Appreciation over holding Period (per year):

Low High

3.0% 5.0%

Potential Costs of Sale: 7.0%

Inflation Holding Costs:

Real Estate Taxes: 2.0%

Insurance: 1.75%

Utilities: 1.75%

Maintenance: 1.75%

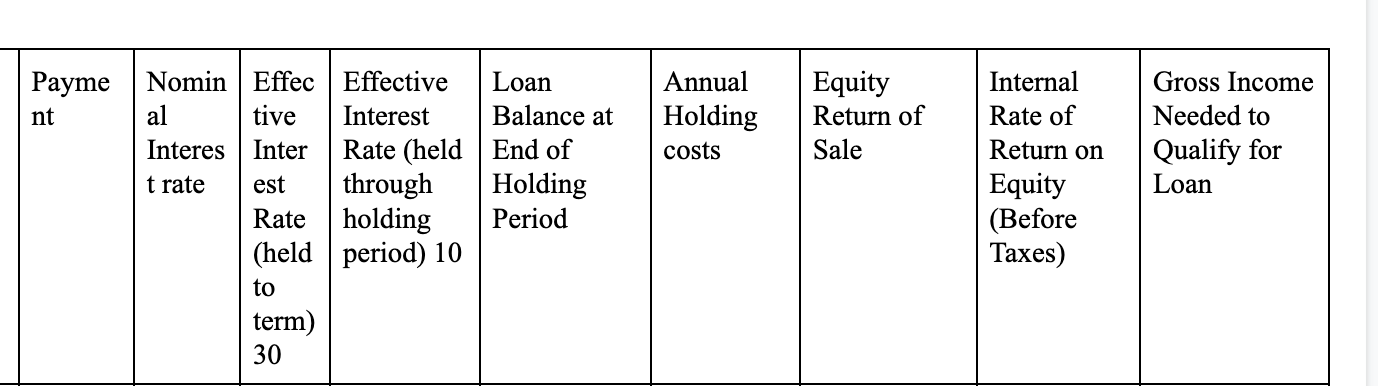

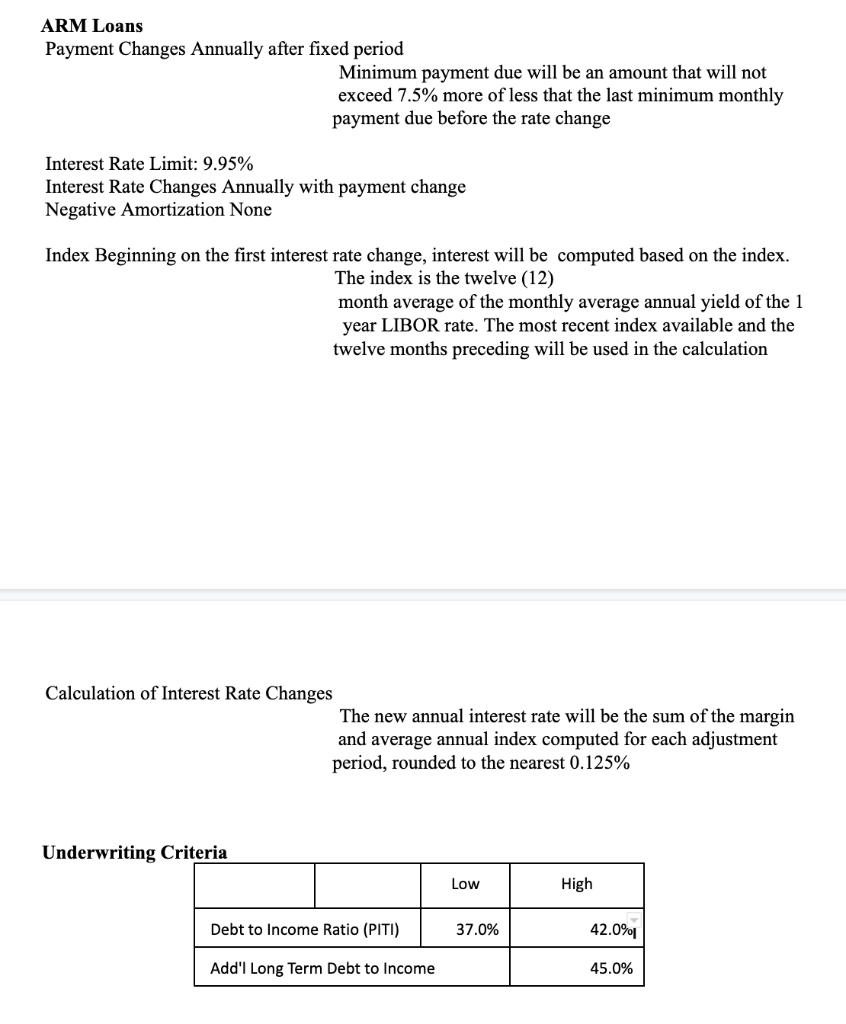

Payme nt Annual Holding costs Equity Return of Sale Nomin Effec Effective Loan al tive Interest Balance at Interes | Inter Rate (held End of t rate est through Holding Rate holding Period (held period) 10 to term) 30 Internal Rate of Return on Equity (Before Taxes) Gross Income Needed to Qualify for Loan 5 ARM Loans Payment Changes Annually after fixed period Minimum payment due will be an amount that will not exceed 7.5% more of less that the last minimum monthly payment due before the rate change Interest Rate Limit: 9.95% Interest Rate Changes Annually with payment change Negative Amortization None Index Beginning on the first interest rate change, interest will be computed based on the index. The index is the twelve (12) month average of the monthly average annual yield of the 1 year LIBOR rate. The most recent index available and the twelve months preceding will be used in the calculation Calculation of Interest Rate Changes The new annual interest rate will be the sum of the margin and average annual index computed for each adjustment period, rounded to the nearest 0.125% Underwriting Criteria Low High Debt to Income Ratio (PITI) 37.0% 42.0% Add'l Long Term Debt to Income 45.0% Payme nt Annual Holding costs Equity Return of Sale Nomin Effec Effective Loan al tive Interest Balance at Interes | Inter Rate (held End of t rate est through Holding Rate holding Period (held period) 10 to term) 30 Internal Rate of Return on Equity (Before Taxes) Gross Income Needed to Qualify for Loan 5 ARM Loans Payment Changes Annually after fixed period Minimum payment due will be an amount that will not exceed 7.5% more of less that the last minimum monthly payment due before the rate change Interest Rate Limit: 9.95% Interest Rate Changes Annually with payment change Negative Amortization None Index Beginning on the first interest rate change, interest will be computed based on the index. The index is the twelve (12) month average of the monthly average annual yield of the 1 year LIBOR rate. The most recent index available and the twelve months preceding will be used in the calculation Calculation of Interest Rate Changes The new annual interest rate will be the sum of the margin and average annual index computed for each adjustment period, rounded to the nearest 0.125% Underwriting Criteria Low High Debt to Income Ratio (PITI) 37.0% 42.0% Add'l Long Term Debt to Income 45.0%

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts