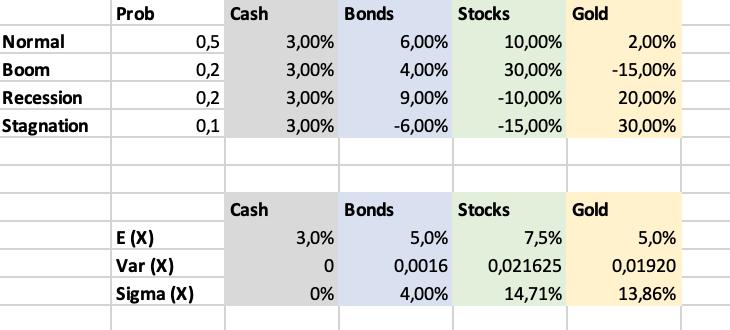

Question: - Compute the Covariance Matrix - Compute the Correlation Matrix - Build 3*11 Portfolios with Cash (and X), and compute E(RP), (RP) in excel Normal

- Compute the Covariance Matrix

- Compute the Correlation Matrix

- Build 3*11 Portfolios with Cash (and X), and compute E(RP), σ(RP) in excel

Normal Boom Recession Stagnation Prob E (X) Var (X) Sigma (X) 0,5 0,2 0,2 0,1 Cash Cash 3,00% 3,00% 3,00% 3,00% 3,0% 0 0% Bonds 6,00% 4,00% 9,00% -6,00% Bonds 5,0% 0,0016 4,00% Stocks 10,00% 30,00% -10,00% -15,00% Stocks 7,5% 0,021625 14,71% Gold Gold 2,00% -15,00% 20,00% 30,00% 5,0% 0,01920 13,86%

Step by Step Solution

There are 3 Steps involved in it

Paste File G2 SAWN 4 1 prob Ready Cut Copy Format Painter Clipboard B 6 7 EX 8 ... View full answer

Get step-by-step solutions from verified subject matter experts