Question: Compute the expected return, standard deviation, beta, and nonsystematic standard deviation of the portfolio. 4. Assume that the total market value of an initial portfolio

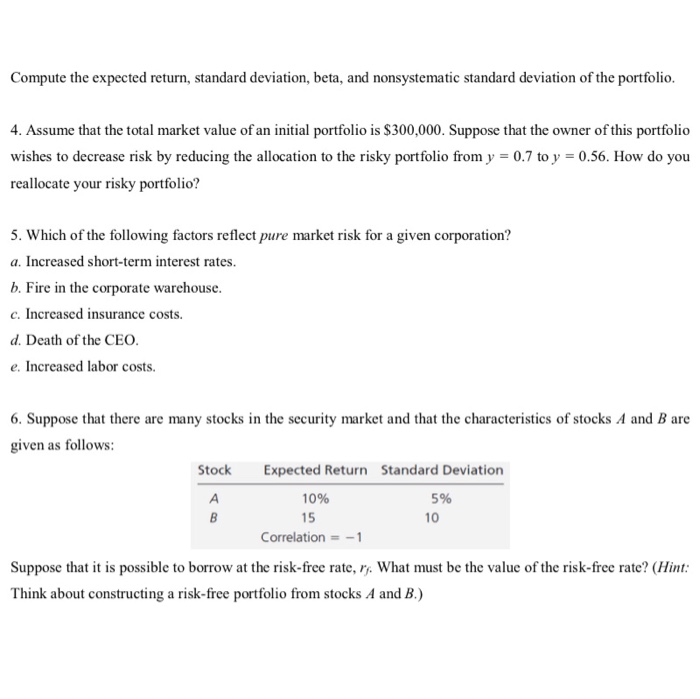

Compute the expected return, standard deviation, beta, and nonsystematic standard deviation of the portfolio. 4. Assume that the total market value of an initial portfolio is $300,000. Suppose that the owner of this portfolio wishes to decrease risk by reducing the allocation to the risky portfolio from y = 0.7 to y = 0.56. How do you reallocate your risky portfolio? 5. Which of the following factors reflect pure market risk for a given corporation? a. Increased short-term interest rates. b. Fire in the corporate warehouse. c. Increased insurance costs. d. Death of the CEO. e. Increased labor costs. 6. Suppose that there are many stocks in the security market and that the characteristics of stocks A and B are given as follows: Stock Expected Return Standard Deviation 10% 5% 15 10 Correlation = -1 Suppose that it is possible to borrow at the risk-free rate, r. What must be the value of the risk-free rate? (Hint: Think about constructing a risk-free portfolio from stocks A and B.)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts