Question: (Computing the standard deviation for a portfolio of two risky investments) Mary Guilott recently graduated from college and is evaluating an investment in two companies'

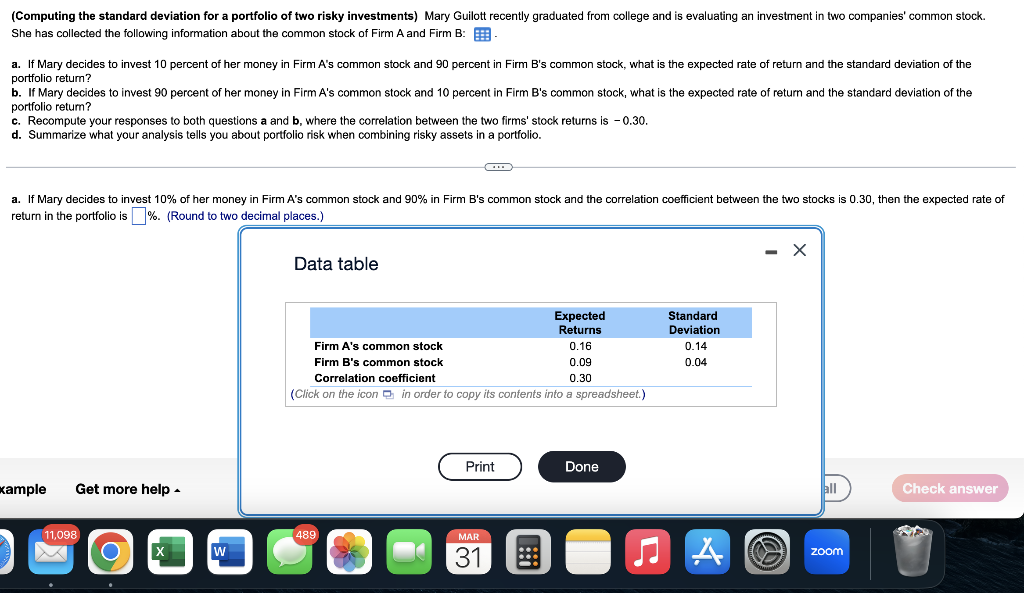

(Computing the standard deviation for a portfolio of two risky investments) Mary Guilott recently graduated from college and is evaluating an investment in two companies' common stock. She has collected the following information about the common stock of Firm A and Firm B: a. If Mary decides to invest 10 percent of her money in Firm A's common stock and 90 percent in Firm B's common stock, what is the expected rate of return and the standard deviation of the portfolio retum? b. If Mary decides to invest 90 percent of her money in Firm A's common stock and 10 percent in Firm B's common stock, what is the expected rate of return and the standard deviation of the portfolio retum? c. Recompute your responses to both questions a and b, where the correlation between the two firms' stock returns is -0.30 . d. Summarize what your analysis tells you about portfolio risk when combining risky assets in a portfolio. a. If Mary decides to invest 10% of her money in Firm A's common stock and 90% in Firm B's common stock and the correlation coefficient between the two stocks is 0.30 , then the expected rate of return in the portfolio is \%. (Round to two decimal places.) Data table

Step by Step Solution

There are 3 Steps involved in it

To solve this problem lets follow a stepbystep approach for each part Given Data Expected Return of Firm A ERA 016 Standard Deviation of Firm A sigmaA ... View full answer

Get step-by-step solutions from verified subject matter experts