Question: Consider a 2 period Binomial Tree Model for stock in which the original stock price is 100 and U =1.25 and p=0.5. a. Find the

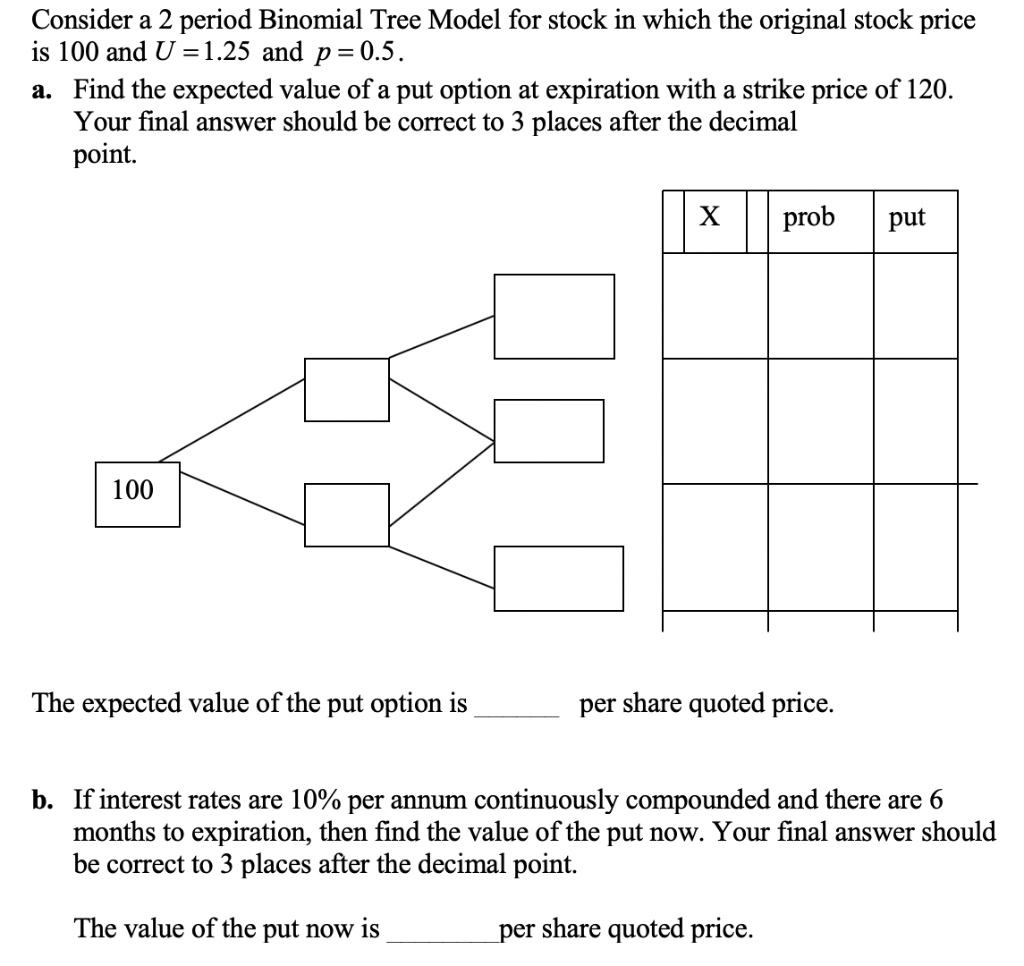

Consider a 2 period Binomial Tree Model for stock in which the original stock price is 100 and U =1.25 and p=0.5. a. Find the expected value of a put option at expiration with a strike price of 120. Your final answer should be correct to 3 places after the decimal point. prob put 100 The expected value of the put option is per share quoted price. b. If interest rates are 10% per annum continuously compounded and there are 6 months to expiration, then find the value of the put now. Your final answer should be correct to 3 places after the decimal point. The value of the put now is per share quoted price

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock