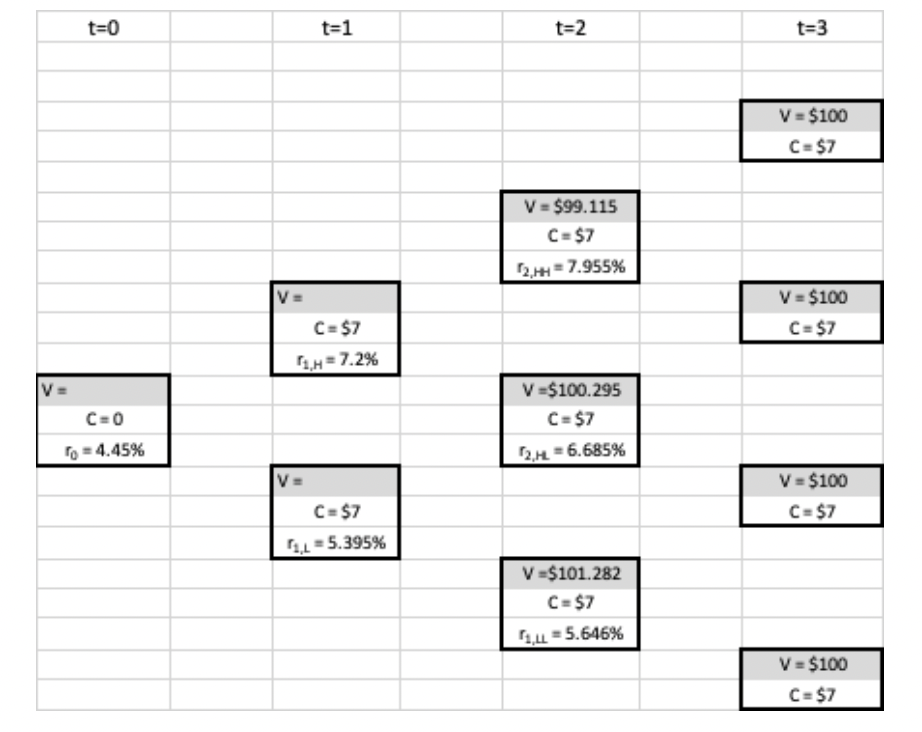

Question: Consider a 3-year putable bond with 7% coupon rate which becomes putable at $101 in one year and stays putable at $101 in the following

Consider a 3-year putable bond with 7% coupon rate which becomes putable at $101 in one year and stays putable at $101 in the following years. As in the following exhibit the prices for an option-free bond in the second year are calculated as $99.115, $100.295, and $101.282 in upper, middle and lower nodes. Assume PH=PL=0.50. Here is the binomial tree and valuation for this bond in spread sheet format What is the modified price at Price at NHH when we consider that this bond is putable?

What is the modified price at Price at NHH when we consider that this bond is putable?

What is the modified price at Price at NHL when we consider that this bond is putable?

What is the modified price at Price at NLL when we consider that this bond is putable?

Given the modified prices above, calculate the putable bond price at NH.

Given the modified prices above, calculate the putable bond price at NL.

What is the bond price at t=0?

Finally, given that the result above and assuming that a similar option free bond is traded at $100.88, what is the value of the put option?

\begin{tabular}{|c|c|c|c|} \hlinet=0 & t=1 & t=2 & t=3 \\ \hline & & & \\ \hline & & & \\ \hline & & & V=$100 \\ \hline & & & C=$7 \\ \hline & & & \\ \hline & & V=$99.115 & \\ \hline & & C=$7 & \\ \hline & & r2,tH=7.955% & \\ \hline & V= & & V=$100 \\ \hline & C=$7 & & C=$7 \\ \hline & r1,H=7.2% & & \\ \hlineV= & & V=$100.295 & \\ \hlineC=0 & & C=$7 & \\ \hliner0=4.45% & & r2,H=6.685% & \\ \hline & V= & & V=$100 \\ \hline & C=$7 & & C=$7 \\ \hline & r1,L=5.395% & & \\ \hline & & V=$101.282 & \\ \hline & & C=$7 & \\ \hline & & \( r_{1, \perp}=5.646 \% \) & \\ \hline & & & V=$100 \\ \hline & & & C=$7 \\ \hline \end{tabular}

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts