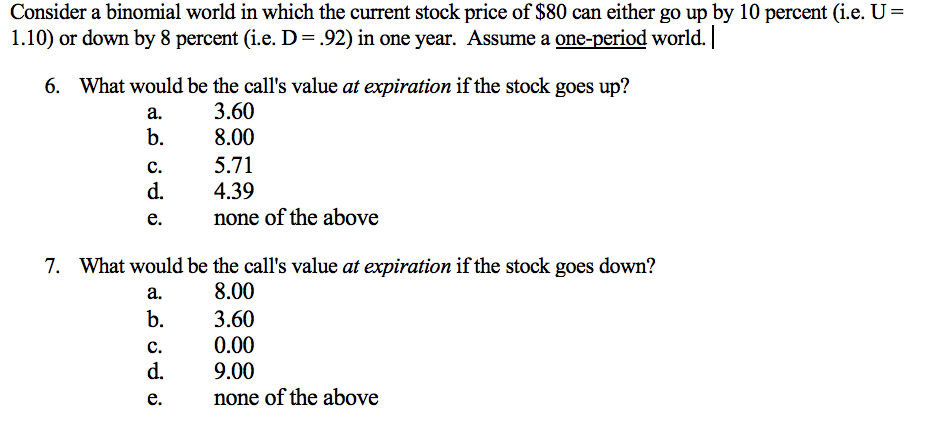

Question: Consider a binomial world in which the current stock price of $80 can either go up by 10 percent (i.e. U= 1.10) or down by

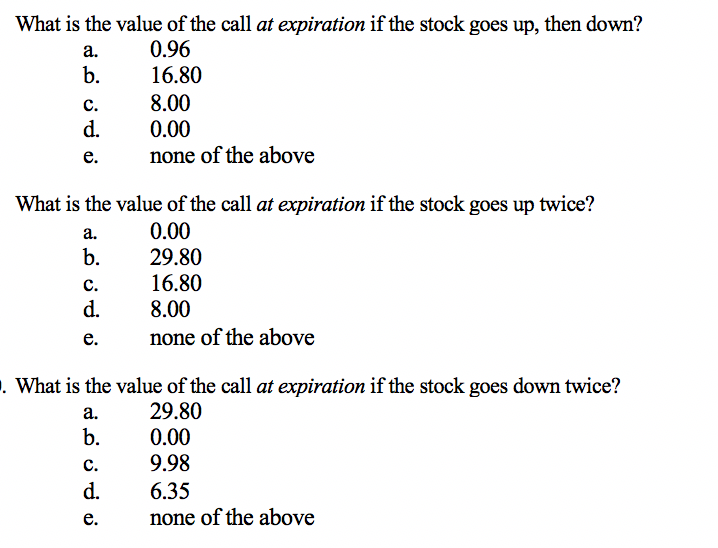

Consider a binomial world in which the current stock price of $80 can either go up by 10 percent (i.e. U= 1.10) or down by 8 percent (i.e. D= .92) in one year. Assume a one-period world. | 6. What would be the call's value at expiration if the stock goes up? 3.60 b. 8.00 5.71 d. 4.39 e. none of the above 7. What would be the call's value at expiration if the stock goes down? a. 8.00 b. 3.60 c. 0.00 d. 9.00 e. none of the above Now extend the one-year binomial model to a two-year model, i.e. step size remains at one-year, but the option expires in two years. What is the value of the call at expiration if the stock goes up, then down? a. 0.96 b. 16.80 c. 8.00 d. 0.00 e. none of the above What is the value of the call at expiration if the stock goes up twice? a. 0.00 b. 29.80 16.80 d. 8.00 e. none of the above . What is the value of the call at expiration if the stock goes down twice? a. 29.80 b. 0.00 C. 9.98 d. 6.35 e. none of the above

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts