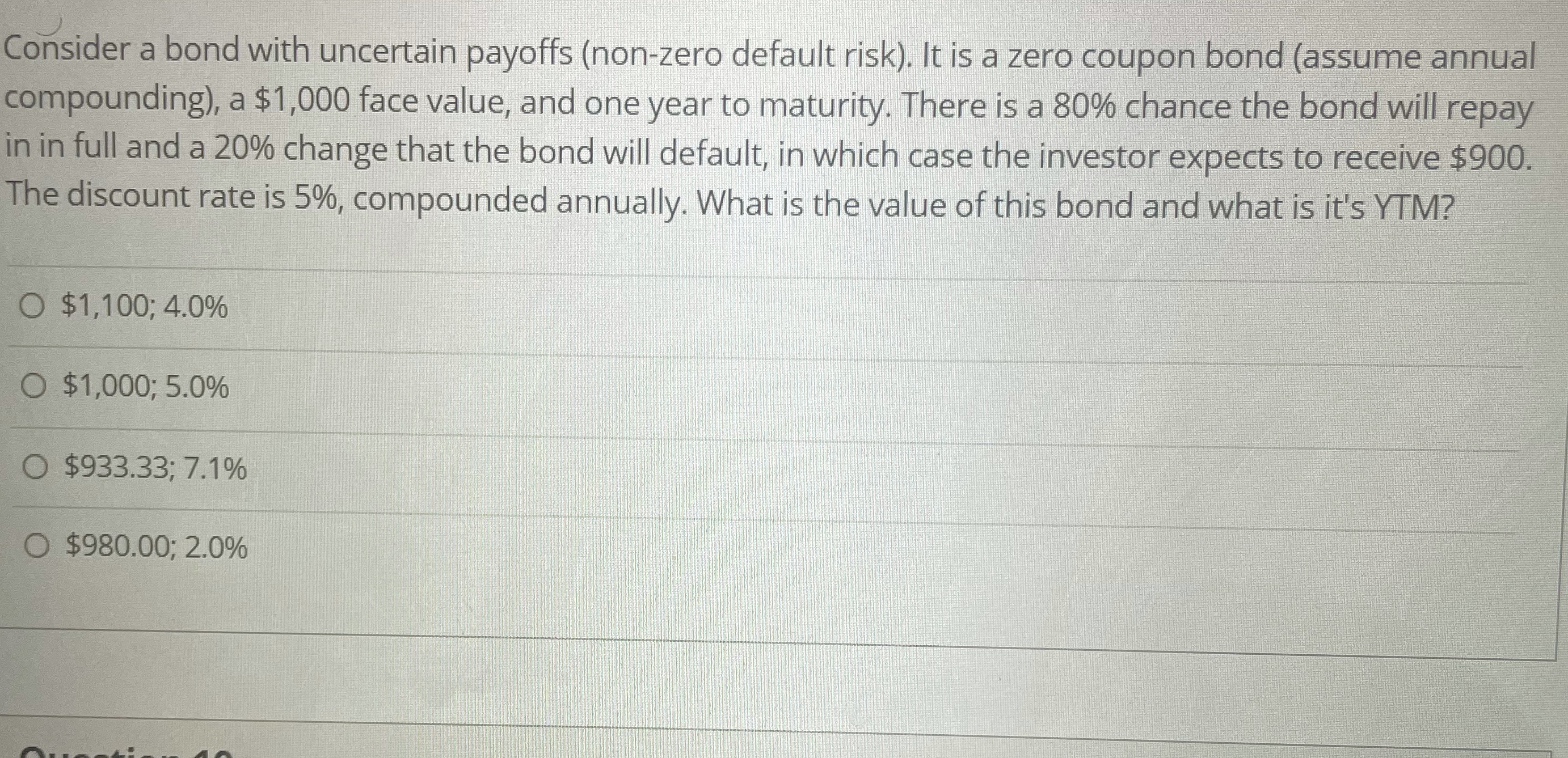

Question: Consider a bond with uncertain payoffs (non-zero default risk). It is a zero coupon bond (assume annual compounding), a $1,000 face value, and one year

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock