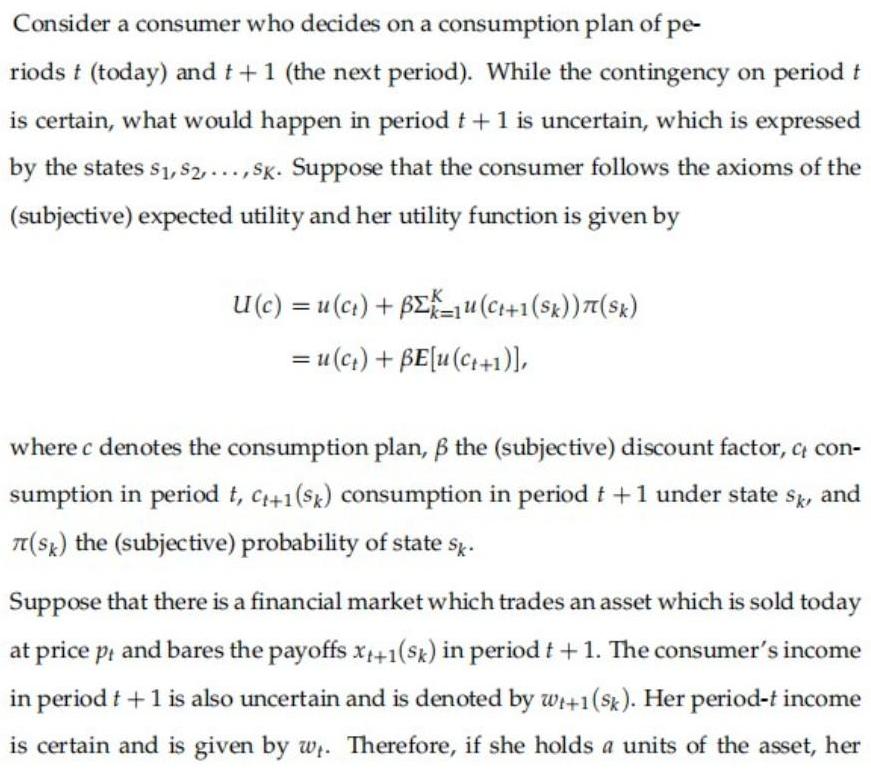

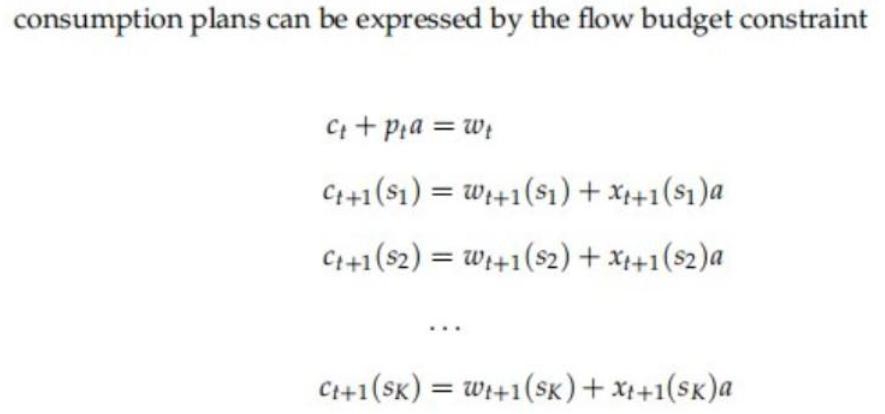

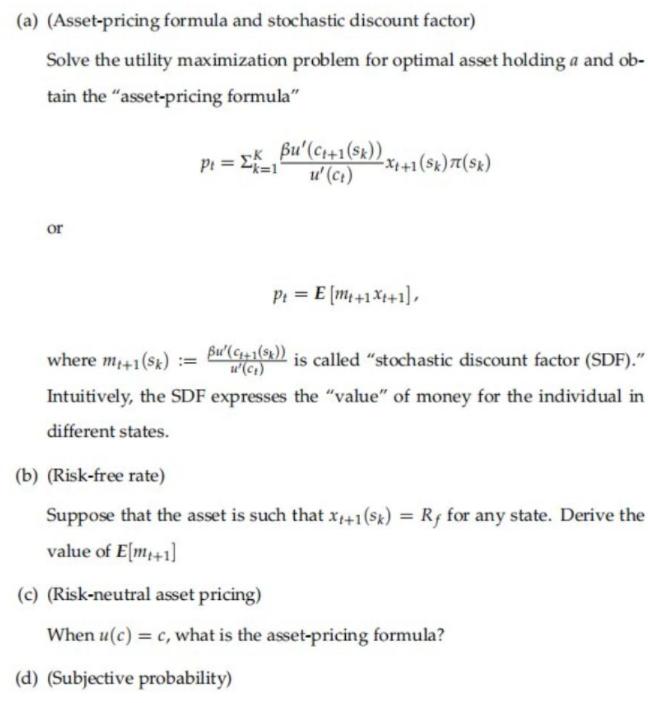

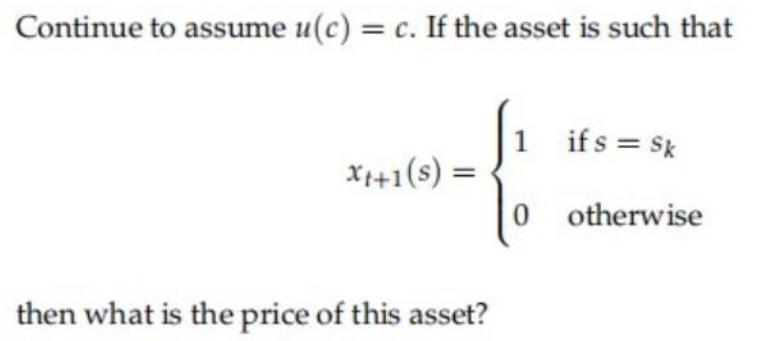

Consider a consumer who decides on a consumption plan of pe- riods t (today) and t...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

Consider a consumer who decides on a consumption plan of pe- riods t (today) and t +1 (the next period). While the contingency on period t is certain, what would happen in period t + 1 is uncertain, which is expressed by the states $₁, $2,..., SK. Suppose that the consumer follows the axioms of the (subjective) expected utility and her utility function is given by -K U (c) = u(c₁) + BEKU (Ct+1(SK)) TT (SK) = u(c₂) + BE[u (C++1)], where c denotes the consumption plan, ß the (subjective) discount factor, c con- sumption in period t, C++1 (SK) consumption in period t + 1 under state sk, and TT(SK) the (subjective) probability of state Sk. Suppose that there is a financial market which trades an asset which is sold today at price pt and bares the payoffs x++1(SK) in period t + 1. The consumer's income in period t + 1 is also uncertain and is denoted by wr+1(sk). Her period-t income is certain and is given by w. Therefore, if she holds a units of the asset, her consumption plans can be expressed by the flow budget constraint C₁ + p₁a = w₁ C++1(S1) = Wt+1(S1) + X₁+1(S₁) a C++1 (52) = Wt+1(S2) + X₁+1($2)a Ct+1(SK) = Wt+1(SK)+x+1(SK)a (a) (Asset-pricing formula and stochastic discount factor) Solve the utility maximization problem for optimal asset holding a and ob- tain the "asset-pricing formula" Pt=P(C₁+1(SK)) x₁+1(SK) TT (SK) or P₁ = E[m₁+1 Xt+1], Bu' (C₁+1(SK)) where mi+1(SK) := is called "stochastic discount factor (SDF)." Intuitively, the SDF expresses the "value" of money for the individual in different states. (b) (Risk-free rate) Suppose that the asset is such that x++1 (Sk) = Rf for any state. Derive the value of E[m+1] (c) (Risk-neutral asset pricing) When u(c) = c, what is the asset-pricing formula? (d) (Subjective probability) Continue to assume u(c) = c. If the asset is such that x+1(s) = then what is the price of this asset? 1 ifs = Sk 0 otherwise (e) (Risk correction for asset pricing) For notational simplicity, drop the subscript for the formula: p = E[mx]. Recall that the covariance Cov (m, x) satisfies Cov(m, x) = E[mx] - E[m]E[x]. Show that, from the asset-pricing formula, we obtain E[x] P = + Cov(m, x). Rf This expression implies that the price of an asset depends on how the asset payoff and SDF covaries across states. Consider a consumer who decides on a consumption plan of pe- riods t (today) and t +1 (the next period). While the contingency on period t is certain, what would happen in period t + 1 is uncertain, which is expressed by the states $₁, $2,..., SK. Suppose that the consumer follows the axioms of the (subjective) expected utility and her utility function is given by -K U (c) = u(c₁) + BEKU (Ct+1(SK)) TT (SK) = u(c₂) + BE[u (C++1)], where c denotes the consumption plan, ß the (subjective) discount factor, c con- sumption in period t, C++1 (SK) consumption in period t + 1 under state sk, and TT(SK) the (subjective) probability of state Sk. Suppose that there is a financial market which trades an asset which is sold today at price pt and bares the payoffs x++1(SK) in period t + 1. The consumer's income in period t + 1 is also uncertain and is denoted by wr+1(sk). Her period-t income is certain and is given by w. Therefore, if she holds a units of the asset, her consumption plans can be expressed by the flow budget constraint C₁ + p₁a = w₁ C++1(S1) = Wt+1(S1) + X₁+1(S₁) a C++1 (52) = Wt+1(S2) + X₁+1($2)a Ct+1(SK) = Wt+1(SK)+x+1(SK)a (a) (Asset-pricing formula and stochastic discount factor) Solve the utility maximization problem for optimal asset holding a and ob- tain the "asset-pricing formula" Pt=P(C₁+1(SK)) x₁+1(SK) TT (SK) or P₁ = E[m₁+1 Xt+1], Bu' (C₁+1(SK)) where mi+1(SK) := is called "stochastic discount factor (SDF)." Intuitively, the SDF expresses the "value" of money for the individual in different states. (b) (Risk-free rate) Suppose that the asset is such that x++1 (Sk) = Rf for any state. Derive the value of E[m+1] (c) (Risk-neutral asset pricing) When u(c) = c, what is the asset-pricing formula? (d) (Subjective probability) Continue to assume u(c) = c. If the asset is such that x+1(s) = then what is the price of this asset? 1 ifs = Sk 0 otherwise (e) (Risk correction for asset pricing) For notational simplicity, drop the subscript for the formula: p = E[mx]. Recall that the covariance Cov (m, x) satisfies Cov(m, x) = E[mx] - E[m]E[x]. Show that, from the asset-pricing formula, we obtain E[x] P = + Cov(m, x). Rf This expression implies that the price of an asset depends on how the asset payoff and SDF covaries across states.

Expert Answer:

Answer rating: 100% (QA)

Part a Assetpricing formula and stochastic discount factor To solve the utility maximization problem for optimal asset holding a we set up the Lagrangean La uct Euct1 wt pt a where is the Lagrange mul... View the full answer

Posted Date:

Students also viewed these general management questions

-

What would happen in Example 1 if we replaced r(t) with its derivative (the rectangular wave)? What is the ratio of the new Cn to the old ones?

-

What would happen in Problem if the immediate predecessor activity changed? For example, activity F may have an immediate predecessor of activity A instead of activity B.

-

What would happen in the apple market if the government set a minimum price of $5.00 per apple? What might motivate such a policy? What would happen in the apple market if the government set a...

-

Discuss the salient features of the international monetary system.

-

Dorel Industries Inc. manufactures and markets juvenile products, bicycles, and a wide assortment of both domestically produced and imported furniture products, principally within North America. The...

-

Prospector Company makes three types of long-burning scented candles. The models vary in terms of size and type of materials (fragrance, decorations, etc.). Unit information for Prospector follows:...

-

Each message in a digital communication system is classified as to whether it is received within the time specified by the system design. If three messages are classified, use a tree diagram to...

-

1. Do you think a country the size of Iceland a Lilliputian is more or less sensitive to the potential impacts of global capital movements? 2. Many countries have used interest rate increases to...

-

It may not have always worked out very well in practice, but theoretically it is possible to issue AAA rated bonds backed by a pool of sub-prime mortgages .Briefly describe how you would do this.Be...

-

Database includes 2 years worth of actual data and one year of budget data for a retail business with 2 locations. In 2017, there was just one location, North. In January 2018, a new location, South,...

-

Choose a company and then choose a process within that company. Then will research that company and the industry in which it exists, and also on the trends that are affecting that company. Explain...

-

The management of Southern Express Corporation is considering investing 20% of all future earnings in growth. The company has a single growth opportunity that it can take either now or in one period....

-

Betas and risk rankings Thomas Hill is considering three stocksA, B, and Cfor possible inclusions in his existing portfolio. Stock A has a beta of 0.75, stock B has a beta of 1.60, and stock C has a...

-

Have you seen job simplification, job rotation, or job expansion being used in your workplace? (If you arent currently working, use a workplace that you are familiar with.) Did it work to motivate...

-

Label each of the following statements true, false, or uncertain. Explain briefly. a. Since 1950, the participation rate in the United States has remained roughly constant at \(60 \%\). b. Each...

-

Are there any groups of people in the United States that you think should be covered by federal laws as a protected group but are not currently covered? Why or why not?

-

Describe factors for finances in college including student expenses, financial aid, and financial decision-making . Describe employment opportunities for students and factors in deciding whether to...

-

D Which of the following is considered part of the Controlling activity of managerial accounting? O Choosing to purchase raw materials from one supplier versus another O Choosing the allocation base...

-

What are the values of the feathering parameters for the airfoils given by Examples 8.5 and 8.6? Examples 8.5 Assume an airfoil pitching about its leading edge and plunging with \(k=0.35\) as follows...

-

Obtain the lift and propulsive force coefficients of an airfoil given in Example 8.6, and compare the results with Problem 8.30. Assume the profile pitches about midchord. Example 8.6 The NACA 0012...

-

Find the heat transfer rate \(\mathrm{q}_{\mathrm{w}}\) at \(\mathrm{x}=10 \mathrm{~cm}\) and \(100 \mathrm{~cm}\) for the flat plate given in Problem 7.31. Problem 7.31 A flat plate of \(4...

Study smarter with the SolutionInn App