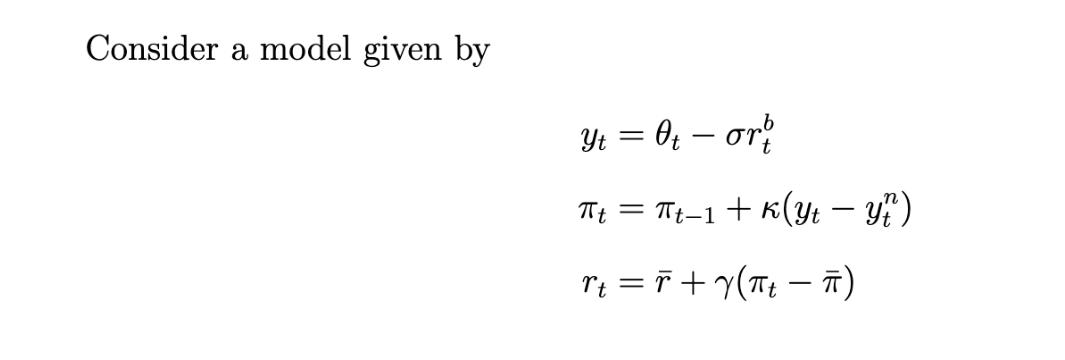

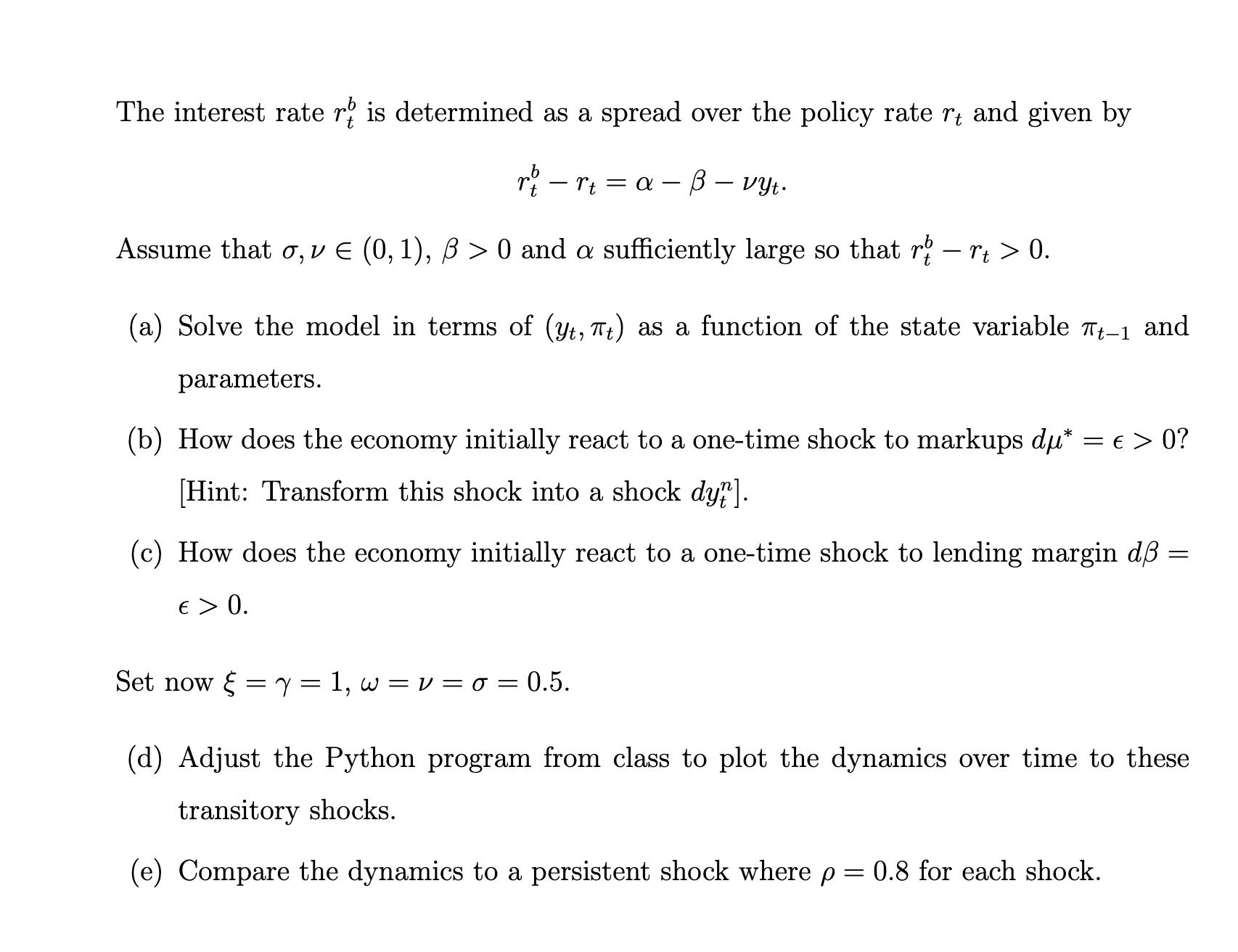

Question: Consider a model given by Yt = 0 - orb Tt = Tt-1 + K(Yt Y?) - rt = F+Y(t ) The interest rate

Consider a model given by Yt = 0 - orb Tt = Tt-1 + K(Yt Y?) - rt = F+Y(t ) The interest rate rt is determined as a spread over the policy rate r, and given by rt rt = a- - vyt. Assume that , v (0, 1), > 0 and a sufficiently large so that r rt > 0. (a) Solve the model in terms of (yt, t) as a function of the state variable Tt-1 and parameters. (b) How does the economy initially react to a one-time shock to markups du* = > 0? [Hint: Transform this shock into a shock dyn]. = (c) How does the economy initially react to a one-time shock to lending margin d : > 0. Set now = 7 = 1 w = v= 0 = 0.5. (d) Adjust the Python program from class to plot the dynamics over time to these transitory shocks. (e) Compare the dynamics to a persistent shock where p = 0.8 for each shock.

Step by Step Solution

3.45 Rating (155 Votes )

There are 3 Steps involved in it

a Solving the model stepbystep 1 Take the equation for yt yt Et t t1 2 Take the equation for t t Yt ... View full answer

Get step-by-step solutions from verified subject matter experts