Question: Consider a multifactor (APT) model of security returns for a particular stock Factor Factor Expected Factor risk premium rate of change Oil prices 5% 7%

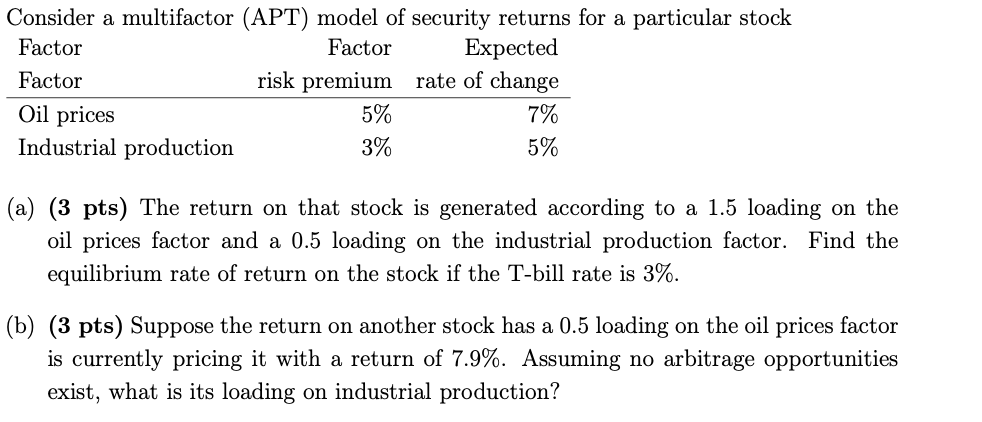

Consider a multifactor (APT) model of security returns for a particular stock Factor Factor Expected Factor risk premium rate of change Oil prices 5% 7% Industrial production 3% 5% (a) (3 pts) The return on that stock is generated according to a 1.5 loading on the oil prices factor and a 0.5 loading on the industrial production factor. Find the equilibrium rate of return on the stock if the T-bill rate is 3%. (b) (3 pts) Suppose the return on another stock has a 0.5 loading on the oil prices factor is currently pricing it with a return of 7.9%. Assuming no arbitrage opportunities exist, what is its loading on industrial production

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts