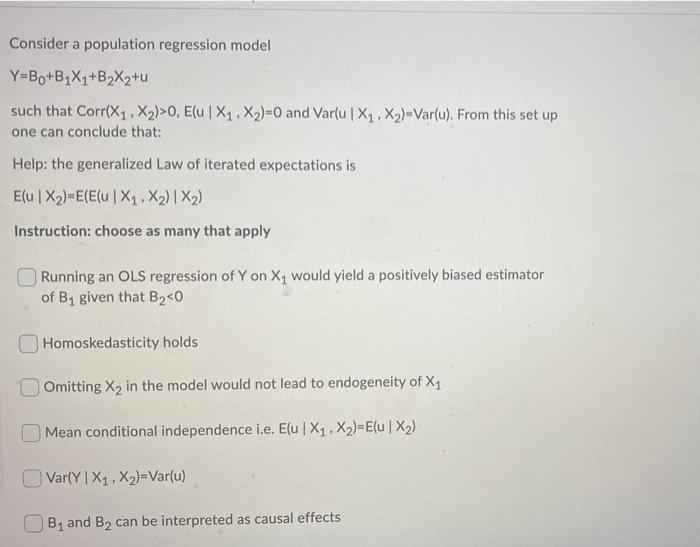

Question: Consider a population regression model Y= Bo+B1X1+B2X2+u such that Corr(X1 , X2)>0, E(u | X1 . X2)=0 and Var(u | X1 , X2)=Var(u). From this

Consider a population regression model Y= Bo+B1X1+B2X2+u such that Corr(X1 , X2)>0, E(u | X1 . X2)=0 and Var(u | X1 , X2)=Var(u). From this set up one can conclude that: Help: the generalized Law of iterated expectations is E(u | X2)=E(E(u | X1 , X2) 1 X2) Instruction: choose as many that apply Running an OLS regression of Y on X, would yield a positively biased estimator of B, given that B2

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock