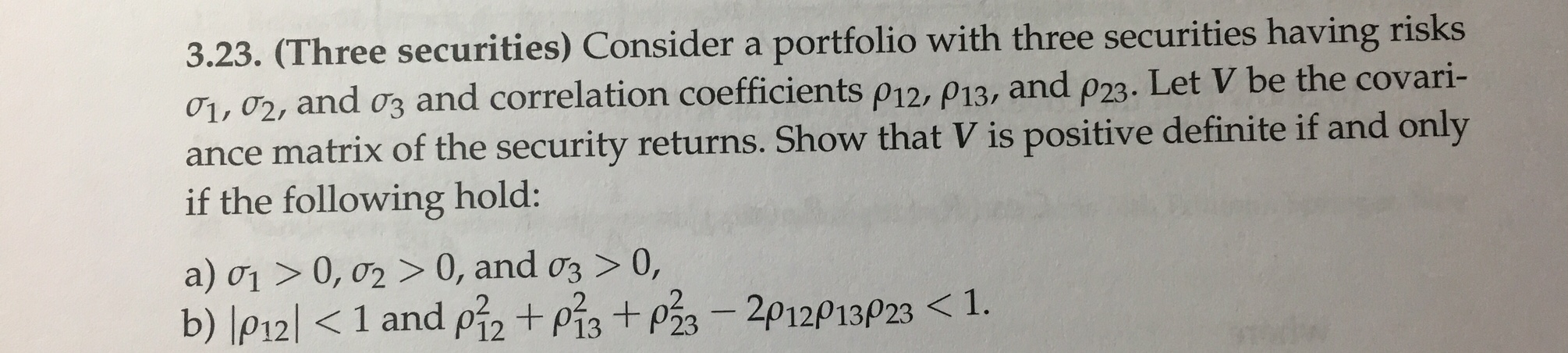

Question: Consider a portfolio with three securities having risks sigma 1, sigma 2, and sigma 3 and correlation coefficients rho 12, rho 13, and rho 23.

Consider a portfolio with three securities having risks sigma 1, sigma 2, and sigma 3 and correlation coefficients rho 12, rho 13, and rho 23. Let V be the covariance matrix of the security returns. Show that V is positive definite if and only if the following hold

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock