Question: Consider a set of time series data defined as random walk as follows: x t = + x t - 1 + w t for

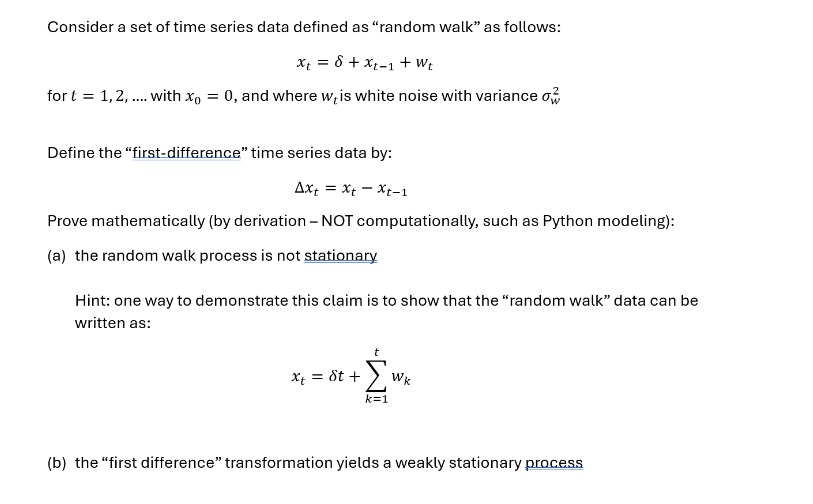

Consider a set of time series data defined as "random walk" as follows:

for dots with and where is white noise with variance

Define the "firstdifference" time series data by:

Prove mathematically by derivation NOT computationally, such as Python modeling:

a the random walk process is not stationary

Hint: one way to demonstrate this claim is to show that the "random walk" data can be

written as:

b the "first difference" transformation yields a weakly stationary process

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock