Question: Consider a single factor APT. We have the following information about the portfolio A, portfolio B, and risk-free rate of return. Please answer the

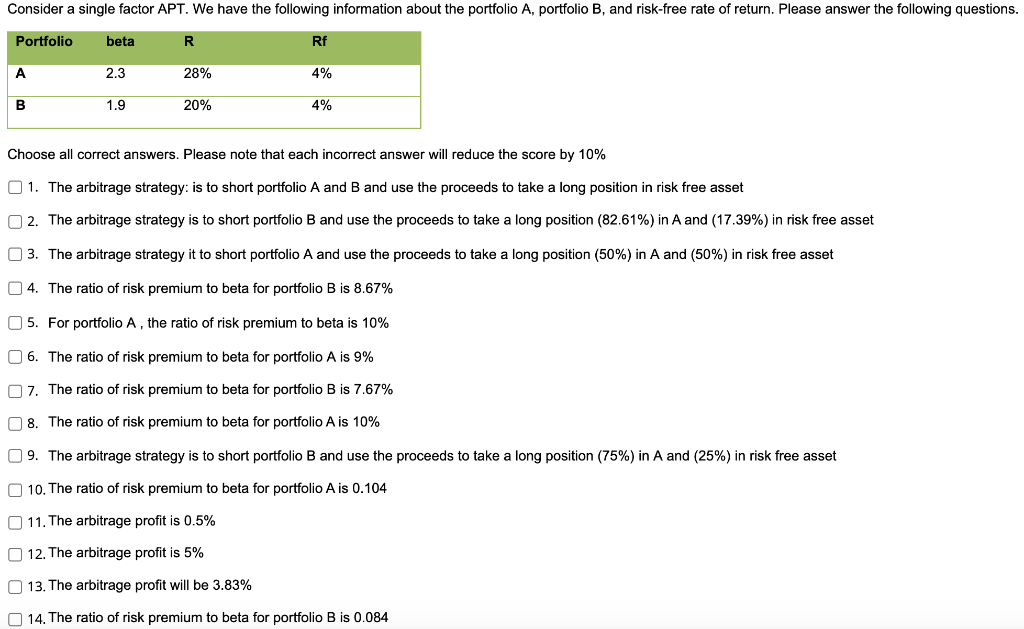

Consider a single factor APT. We have the following information about the portfolio A, portfolio B, and risk-free rate of return. Please answer the following questions. Portfolio Rf beta R 2.3 28% 4% B 1.9 20% 4% A Choose all correct answers. Please note that each incorrect answer will reduce the score by 10% 1. The arbitrage strategy: is to short portfolio A and B and use the proceeds to take a long position in risk free asset 2. The arbitrage strategy is to short portfolio B and use the proceeds to take a long position (82.61%) in A and (17.39%) in risk free asset 13. The arbitrage strategy it to short portfolio A and use the proceeds to take a long position (50%) in A and (50%) in risk free asset 4. The ratio of risk premium to beta for portfolio B is 8.67% 5. For portfolio A, the ratio of risk premium to beta is 10% 6. The ratio of risk premium to beta for portfolio A is 9% 7. The ratio of risk premium to beta for portfolio B is 7.67% 18. The ratio of risk premium to beta for portfolio A is 10% 9. The arbitrage strategy is to short portfolio B and use the proceeds to take a long position (75%) in A and (25%) in risk free asset 10. The ratio of risk premium to beta for portfolio A is 0.104 11. The arbitrage profit is 0.5% 12. The arbitrage profit is 5% 13. The arbitrage profit will be 3.83% 14. The ratio of risk premium to beta for portfolio B is 0.084

Step by Step Solution

There are 3 Steps involved in it

To solve these questions we need to calculate the risk premiums and the ratio of risk premiums to beta for each portfolio The risk premium is calculat... View full answer

Get step-by-step solutions from verified subject matter experts