Question: Consider a stock and a bond with the following risks. For simplicity the risk free rate is rf=0. This problem involves calculations of several steps.

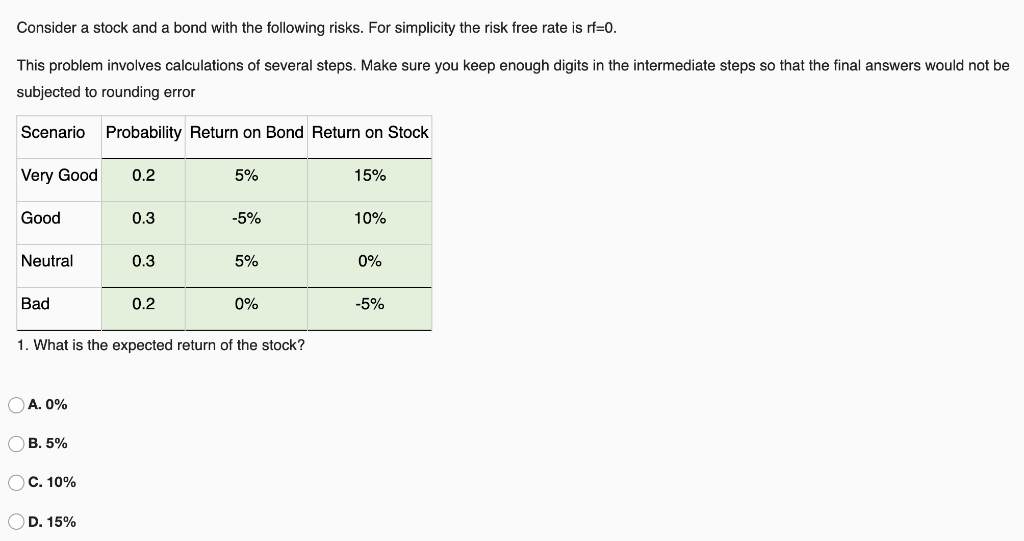

Consider a stock and a bond with the following risks. For simplicity the risk free rate is rf=0. This problem involves calculations of several steps. Make sure you keep enough digits in the intermediate steps so that the final answers would not be subjected to rounding error Scenario Probability Return on Bond Return on Stock Very Good 0.2 5% 15% Good 0.3 -5% 10% Neutral 0.3 5% 0% Bad 0.2 0% -5% 1. What is the expected return of the stock? A. 0% OB. 5% OC. 10% OD 15% 2. What is the Sharpe ratio of the stock? A. 0.23 B. 0.45 C. 0.67 D. 0.89 3. What is the correlation between the stock and the bond? OA. -0.15 OB. -0.17 C. -0.19 D. -0.21 4. You create a portfolio by mixing stocks and bonds. What Sharpe ratio do you obtain if you invest 50/50 in the bond and stock? Sharpe ratio = (round answer to two decimal places) 5. What is the weight on stocks that would give you the highest Sharpe ratio? Answer = (round answer to nearest two decimal places) 6. What is the highest Sharpe ratio that you achieve? Answer: (round answer to nearest two decimal places)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts